India’s External Sector: Trade, Forex & Balance of Payments (Economic Survey 2025–26)

GLOBAL TRADE DYNAMICS AND INDIA’S TRADE PERFORMANCE

The global economic order is undergoing a structural transformation marked by rising protectionism, geopolitical fragmentation, and a shift from multilateralism to strategic bilateralism. Supply chains are being reconfigured to prioritise resilience, national security, and technological sovereignty over cost efficiency. Trade policy uncertainty has surged, driven by tariff wars, industrial policies, and competition over critical resources, leading to increased volatility in global trade.

In this evolving landscape, India’s external sector has demonstrated resilience through diversification, strong services exports, and expanding trade partnerships. While merchandise exports remain stable, the growth of non-petroleum exports and services trade highlights structural strengths. India’s integration into global trade has deepened, with rising shares in both merchandise and services exports.

However, challenges persist, including widening trade deficits, dependence on imported intermediates, and limited export complexity. Policy initiatives such as Production-Linked Incentive (PLI) schemes, FTAs, and export promotion measures aim to enhance competitiveness and diversification. Overall, India’s external sector reflects a balance between global vulnerabilities and domestic strengths, with significant potential for structural upgrading and export-led growth.

GLOBAL TRADE DYNAMICS

1. Structural Shift in Global Trade

- Globalisation is giving way to a fragmented and protectionist trade environment.

- Supply chains are being restructured to prioritise resilience and national security.

- Bilateral and strategic trade relationships are replacing multilateral frameworks.

- Economies are increasingly focusing on domestic capacity building.

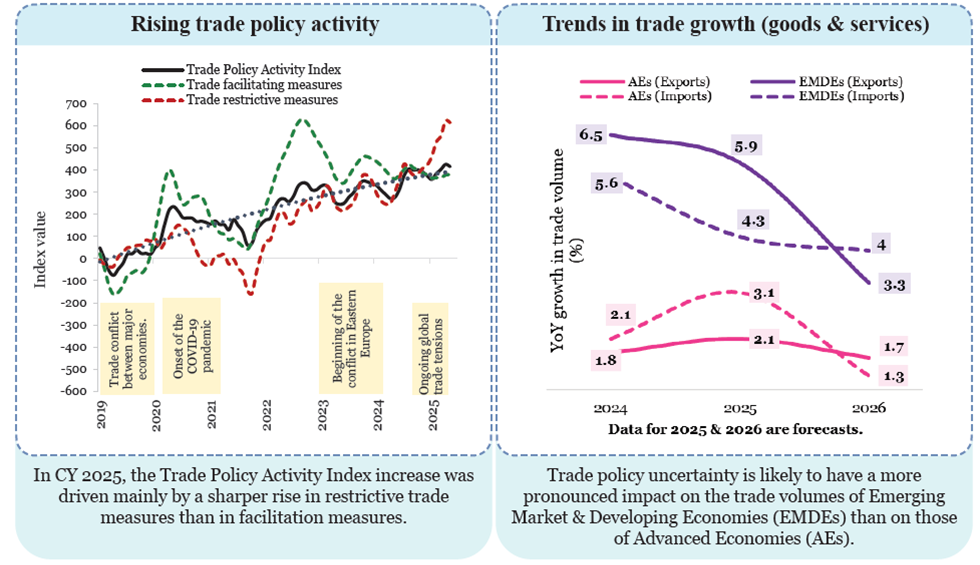

2. Rising Trade Policy Uncertainty

- Trade Policy Uncertainty (TPU) and Global Economic Policy Uncertainty (GEPU) indices surged sharply in 2025.

- Drivers include tariff wars, weakening multilateral agreements, and competition for critical minerals.

- Uncertainty is reinforced by unilateral trade measures and retaliatory policies.

- Elevated uncertainty affects global trade volumes and investment decisions.

3. Emerging Global Trade Trends

- “Geostrategic globalisation” is replacing pure economic globalisation.

- Friend-shoring and nearshoring trends are reshaping trade flows.

- Trade concentration is increasing among major economies.

- Economic, political, and technological factors are increasingly interlinked in trade decisions.

4. Global Trade Performance

- Global trade growth is projected to slow from 3.6% (2025) to 2.3% (2026).

- Emerging economies are expected to grow faster but are more vulnerable to uncertainty.

- Trade growth in 2025 was partly driven by frontloading due to anticipated tariffs.

- Fragmentation continues to constrain long-term trade expansion.

INDIA’S TRADE PERFORMANCE

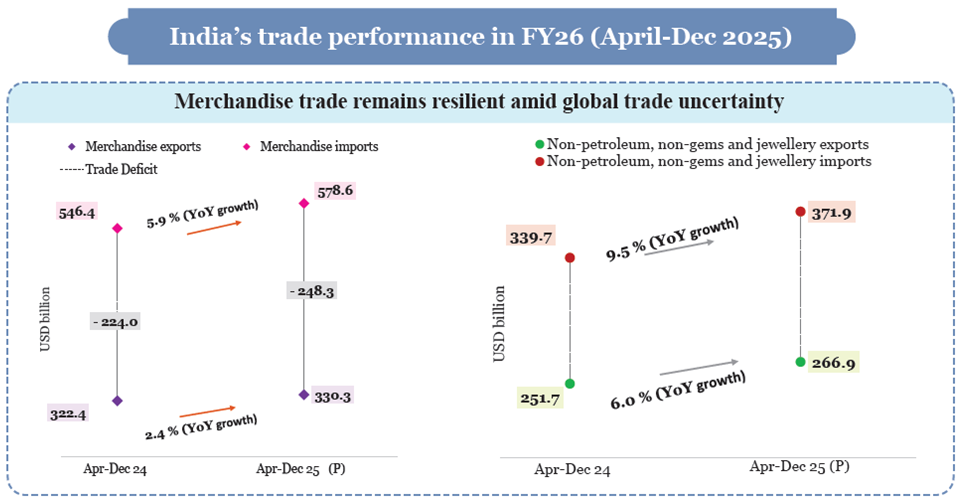

5. Overall Trade Trends

- India’s total exports reached a record USD 825.3 billion in FY25, driven by services.

- Imports increased to USD 919.9 billion, leading to a trade deficit of USD 94.7 billion.

- Strong domestic demand contributed to rising imports.

- Trade performance reflects resilience despite global uncertainty.

6. Merchandise Trade Performance

- Merchandise exports remained stable at USD 437.7 billion in FY25.

- Non-petroleum, non-gems exports grew strongly, indicating core sector strength.

- Petroleum and gems exports masked underlying positive trends.

- Merchandise imports increased due to demand for capital goods and intermediates.

7. Composition of Trade

- Key export sectors include petroleum products, telecom equipment, and pharmaceuticals.

- Electronics and telecom exports are growing rapidly, indicating manufacturing strength.

- Imports are dominated by crude oil, gold, and electronic goods.

- Rising imports of intermediates indicate integration into global value chains.

8. Trade Deficit Dynamics

- Merchandise trade deficit widened significantly due to rising imports.

- Services trade surplus partially offsets the merchandise deficit.

- Increasing imports reflect growth rather than weakness.

- Managing trade balance requires export diversification and value addition.

9. Agricultural Trade

- Agricultural exports grew to USD 51.1 billion (FY25) but remain below potential.

- India’s global share in agricultural exports is only 2.2%, despite high production.

- Policy interventions (export bans, price controls) disrupt export stability.

- Agricultural exports have strong potential as a future growth driver.

10. PLI Scheme and Trade

- PLI sectors recorded strong export growth (~10.6% annually).

- High-growth sectors include electronics, IT hardware, and batteries.

- Import growth alongside exports reflects integration into value chains.

- Some sectors show early success in import substitution (e.g., telecom).

11. Diversification of Trade

- India is diversifying export destinations beyond traditional markets like the US.

- Alternative markets include UAE, EU, Africa, and Southeast Asia.

- Crude oil import sources are also becoming more diversified.

- Diversification enhances resilience against global shocks.

12. Export Complexity Challenge

- India ranks 44th in Economic Complexity Index (ECI).

- Export basket is dominated by low- and mid-complexity products.

- High-complexity sectors like advanced manufacturing remain underdeveloped.

- However, strong potential exists as per Complexity Outlook Index (COI).

13. Policy Measures for Export Growth

- FTAs (e.g., India-UK, India-Oman) enhance market access.

- Export Promotion Mission provides integrated support to exporters.

- RBI measures improve liquidity and ease credit constraints.

- Focus is shifting toward competitiveness, innovation, and diversification.

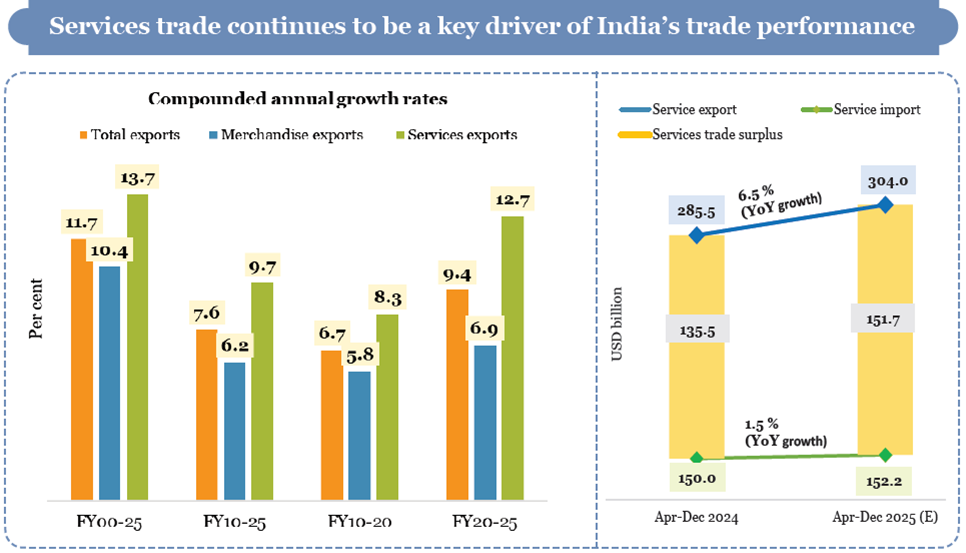

14. Services Trade Performance

- Services exports reached USD 387.5 billion in FY25, growing 13.6%.

- Services surplus covered nearly two-thirds of merchandise deficit.

- Key sectors include IT, business services, and fintech.

- Growth driven by Global Capability Centres (GCCs) and skilled workforce.

Data & Facts

- Total exports: USD 825.3 billion (FY25)

- Total imports: USD 919.9 billion (FY25)

- Trade deficit: USD 94.7 billion

- Merchandise exports: USD 437.7 billion

- Services exports: USD 387.5 billion

- Services surplus: USD 188.8 billion

- Agricultural exports: USD 51.1 billion

- India’s share in global merchandise exports: 1.8%

- India’s share in global services exports: 4.3%

Concepts

- Balance of Payments (BoP): Record of all economic transactions with the rest of the world.

- Trade Deficit: When imports exceed exports.

- Friend-shoring: Trading with politically aligned countries.

- Nearshoring: Shifting production closer geographically.

- Economic Complexity Index (ECI): Measures sophistication of a country’s exports.

- PLI Scheme: Incentive scheme to boost manufacturing and exports.

Analysis

The external sector reflects a dual reality—global fragmentation and domestic resilience. While rising protectionism and uncertainty are reshaping global trade, India has adapted through diversification, services strength, and policy support.

However, structural challenges remain, particularly low export complexity and dependence on imports for intermediates. The key strategic shift required is moving from volume-driven exports to value-driven exports.

Strengthening manufacturing, improving product sophistication, and ensuring policy stability—especially in agriculture—will be crucial. India’s ability to leverage global shifts while building domestic capabilities will determine its long-term position in global trade.

INDIA’S BALANCE OF PAYMENT

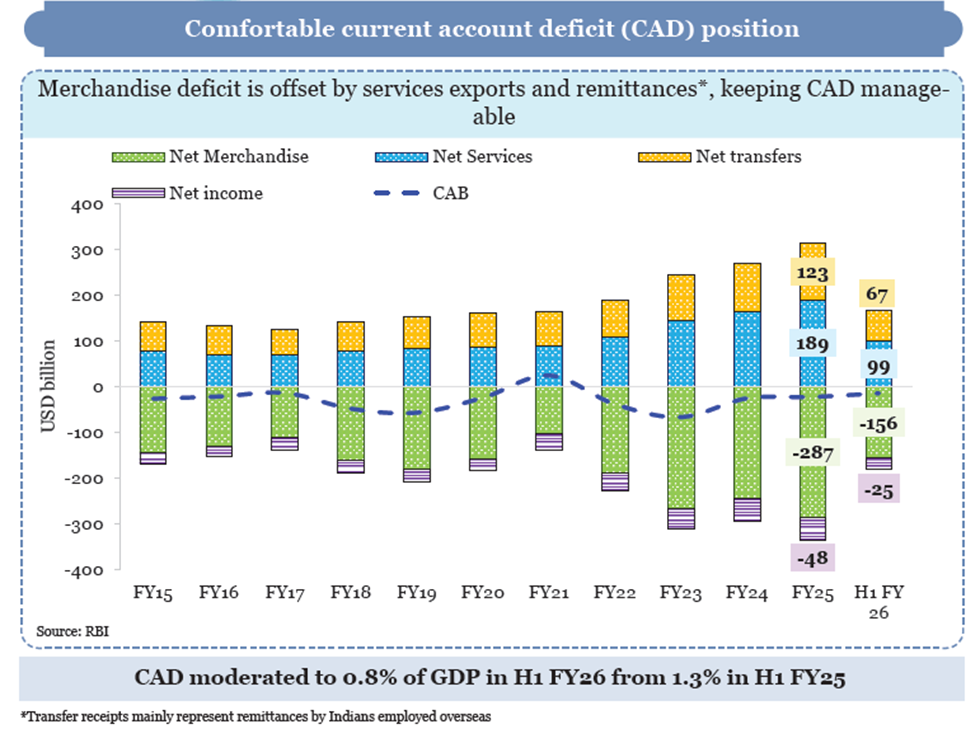

India’s external sector demonstrates resilience through a balanced combination of current account management and stable capital inflows. While the economy continues to run a merchandise trade deficit, it is effectively offset by strong services exports and robust remittance inflows, keeping the current account deficit (CAD) at manageable levels.

On the capital account side, India continues to attract significant foreign investments, particularly FDI, which remains stable despite global uncertainty. Portfolio flows, however, remain volatile and sensitive to global financial conditions.

Foreign exchange reserves are at comfortable levels, providing a buffer against external shocks. Exchange rate movements reflect both structural factors such as persistent trade deficits and cyclical factors like capital flow volatility. Empirical evidence suggests that a weaker currency improves India’s trade balance, particularly merchandise exports, while the financial channel may offset some gains.

Over the long term, sustainable external stability depends on strengthening manufacturing exports, improving export complexity, and enhancing domestic savings. The outlook emphasises export-led growth, stable capital inflows, and structural reforms as key drivers of external sector resilience.

Key Points

1. Current Account Dynamics

- India runs a structural merchandise trade deficit, offset by services surplus and remittances.

- CAD moderated to 0.8% of GDP in H1 FY26 from 1.3% a year earlier.

- Services exports and remittances act as stable buffers.

- India’s CAD remains modest compared to other deficit economies.

2. Role of Remittances

- Remittances reached USD 73 billion in H1 FY26.

- India remains the world’s largest recipient of remittances.

- Remittances account for around 3.5% of GDP and exceed FDI inflows in many years.

- Shift observed towards advanced economies (US, UK) as major sources.

3. Capital Account Trends

- Capital account reflects foreign investments, borrowings, and external financing.

- FDI remains stable and reflects investor confidence in India’s growth.

- Portfolio flows are volatile and influenced by global interest rates.

- External borrowing trends depend on global liquidity conditions.

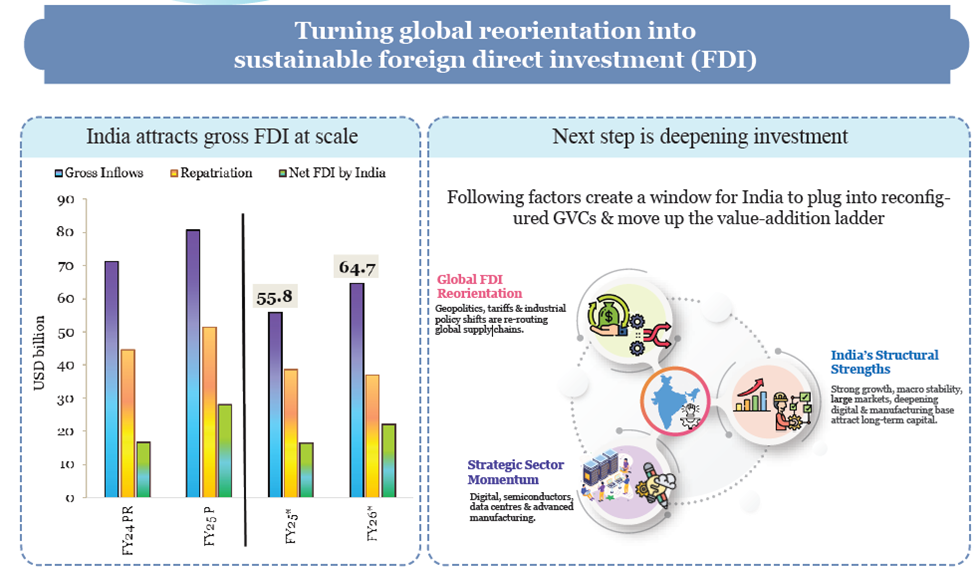

4. Global FDI Trends

- Global FDI declined by 11% in 2024, reflecting weak investment climate.

- Technology sectors (AI, semiconductors) attract majority investments.

- Infrastructure investments declined due to high interest rates.

- Shift towards short-term, technology-driven investments.

5. FDI in India

- Gross FDI inflows: USD 81 billion (FY25) with continued growth in FY26.

- Net FDI improved due to reduced repatriation and steady inflows.

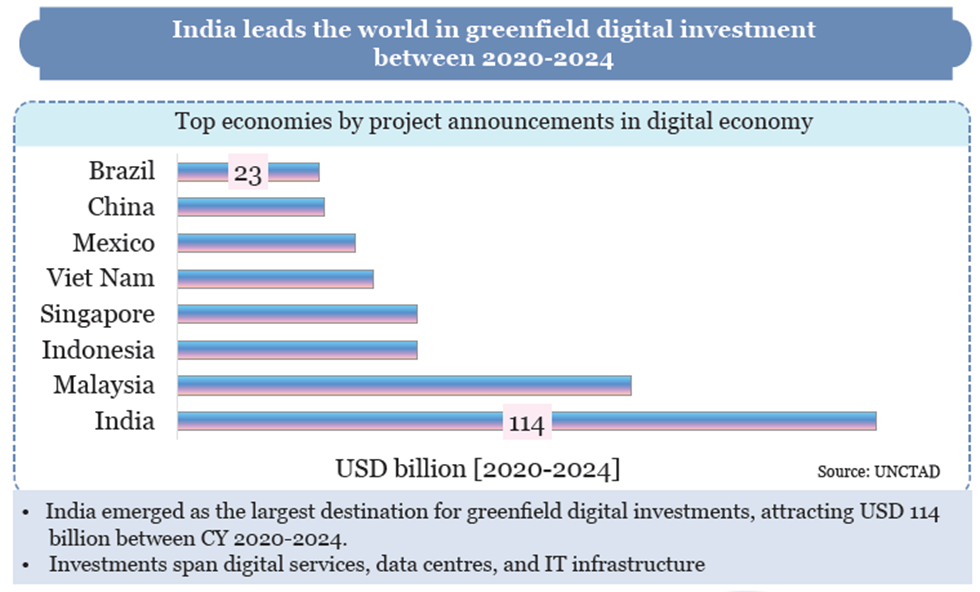

- India ranks among top global destinations for greenfield investments.

- Key sectors: services, IT, infrastructure, and manufacturing.

6. Outward Direct Investment (ODI)

- ODI increased, reflecting global expansion of Indian firms.

- Helps acquire technology, markets, and resources.

- Complements domestic investment in the long run.

- India is transitioning toward greater global economic integration.

7. Foreign Portfolio Investment (FPI)

- FPI flows are cyclical and sensitive to global financial conditions.

- FY26 witnessed alternating inflows and outflows.

- Equity flows dominate during favourable market conditions.

- Debt flows stabilised through VRR and FAR mechanisms.

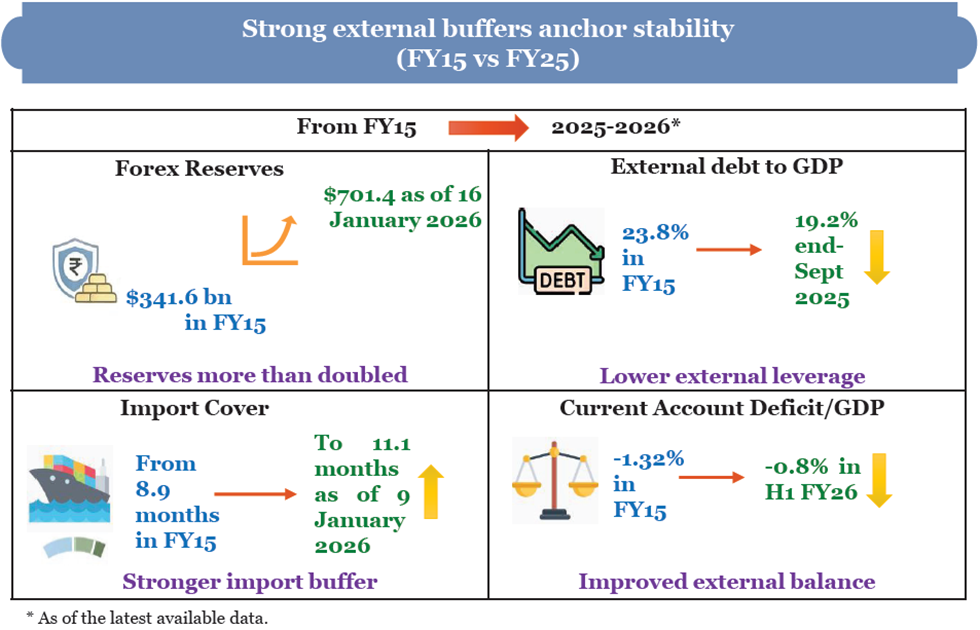

8. Foreign Exchange Reserves

- Forex reserves reached USD 701.4 billion (Jan 2026).

- Cover around 11 months of imports, indicating strong adequacy.

- Increasing share of gold reflects diversification strategy.

- Reserves provide a buffer against external shocks.

9. Exchange Rate Dynamics

- INR depreciated by ~5.4% in FY26 against USD.

- Depreciation driven by capital outflows and trade dynamics.

- Exchange rate influenced by both CAD and capital inflows.

- Persistent import demand creates structural depreciation pressure.

10. Exchange Rate Channels

Trade Channel

- Currency depreciation improves export competitiveness.

- Merchandise trade responds strongly to exchange rate changes.

- Services exports are relatively less sensitive to exchange rates.

Financial Channel

- Currency appreciation attracts capital inflows in short term.

- However, long-term effects may reverse due to policy responses.

- Overall, trade gains outweigh financial losses for India.

11. External Debt & NIIP

- External debt: USD 746 billion (Sept 2025) (~20% of GDP).

- India’s debt levels are moderate compared to global standards.

- NIIP remains negative but is improving gradually.

- Asset-liability ratio rising indicates strengthening external balance sheet.

12. Structural Drivers of External Balance

- High growth leads to increased imports (capital goods, energy).

- Export sectors depend on imported intermediates.

- Gold imports contribute to trade deficit.

- External balance depends on both trade and capital flows.

13. Lessons from Global Experience

- Strong manufacturing exports are key to sustained external stability.

- East Asian economies achieved currency strength through export-led growth.

- Services exports alone are insufficient for long-term external balance.

- Industrial policy must focus on productivity and global competitiveness.

14. Policy Priorities

- Enhance manufacturing export competitiveness.

- Improve logistics and reduce cost of production.

- Promote stable and long-term FDI inflows.

- Strengthen innovation, R&D, and export complexity.

- Ensure policy stability and ease of doing business.

Data & Facts

- CAD: 0.8% of GDP (H1 FY26)

- Remittances: USD 135.4 billion (FY25)

- Forex reserves: USD 701.4 billion

- External debt: ~20% of GDP

- FDI inflows: USD 81 billion (FY25)

- ODI: USD 23.6 billion (FY25)

- INR depreciation: ~5.4% (FY26)

Concepts

- Current Account Deficit (CAD): When imports of goods/services exceed exports.

- FDI (Foreign Direct Investment): Long-term investment in productive assets.

- FPI (Foreign Portfolio Investment): Short-term investment in financial assets.

- Foreign Exchange Reserves: Assets held by central bank to manage currency stability.

- NIIP (Net International Investment Position): Difference between external assets and liabilities.

- Exchange Rate Channels: Trade and financial pathways through which currency affects the economy.

Analysis

India’s external sector reflects a structurally stable yet evolving framework. While trade deficits persist due to growth-driven imports, strong services exports and remittances provide a cushion.

The increasing importance of FDI highlights a shift toward stable capital financing, while volatile portfolio flows underscore external vulnerabilities. Exchange rate dynamics reveal a deeper structural issue—India’s reliance on imports and limited export sophistication.

The long-term solution lies in strengthening manufacturing exports, enhancing productivity, and improving integration into global value chains. The emphasis on export-led growth and stable capital inflows signals a strategic shift toward building durable external resilience in a fragmented global economy.

One Comment