Industrial Growth, Manufacturing & Production Trends (Economic Survey 2025–26)

GLOBAL TRENDS & DOMESTIC DEVELOPMENTS

The global manufacturing landscape in 2025 reflects an uneven recovery marked by geopolitical tensions, inflationary pressures, and supply chain realignments. While overall growth remains subdued, a structural shift toward high-technology and innovation-driven manufacturing is evident, with medium- and high-tech industries outperforming low-tech segments.

Countries are increasingly focusing on strategic integration into Global Value Chains (GVCs) to enhance resilience and competitiveness. In this context, India’s industrial sector has demonstrated strong resilience and structural transformation.

Industrial GVA growth has accelerated, supported by manufacturing recovery, infrastructure expansion, and policy interventions such as the Production Linked Incentive (PLI) schemes. A significant transition towards high-value manufacturing is underway, with medium- and high-tech sectors accounting for a rising share of output.

Business sentiment remains positive, as reflected in strong PMI and investment indicators. Additionally, the financial landscape is evolving, with industries increasingly diversifying away from bank credit towards market-based financing. Overall, India’s industrial sector is emerging as a key growth engine, driven by technological upgrading, policy support, and improving global integration.

Key Points

1. Global Manufacturing Trends

- Global manufacturing growth remains uneven due to geopolitical tensions and supply chain disruptions.

- Manufacturing output grew modestly, with regional disparities across continents.

- Medium- and high-technology industries are expanding faster than low-tech sectors.

- Investment is increasingly directed towards digital and innovation-driven sectors.

- Countries are focusing on strategic positioning in global value chains (GVCs).

2. Shift Towards High-Tech Manufacturing

- Global manufacturing is transitioning from cost-based production to innovation-driven value chains.

- High-tech sectors are emerging as the primary drivers of industrial growth.

- Strategic indispensability is becoming more important than cost competitiveness.

- Countries aim to secure critical positions in supply chains to reduce vulnerabilities.

3. India’s Industrial Performance

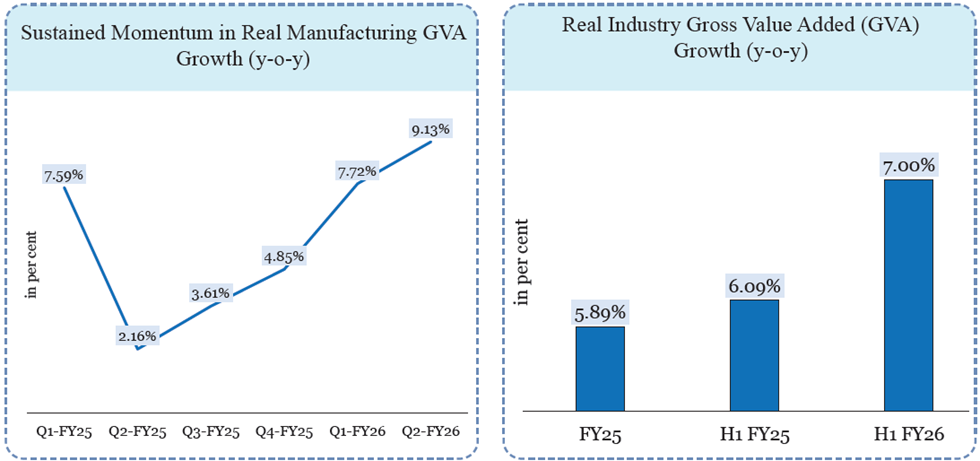

- Industry GVA grew by 7.0% in H1 FY26, indicating strong recovery.

- Manufacturing growth accelerated significantly in FY26 compared to FY25.

- Growth slowdown in FY25 was largely due to global demand conditions, not domestic weakness.

- Structural improvements have strengthened India’s industrial capability.

4. Structural Transformation in Manufacturing

- India is shifting towards higher-value manufacturing segments.

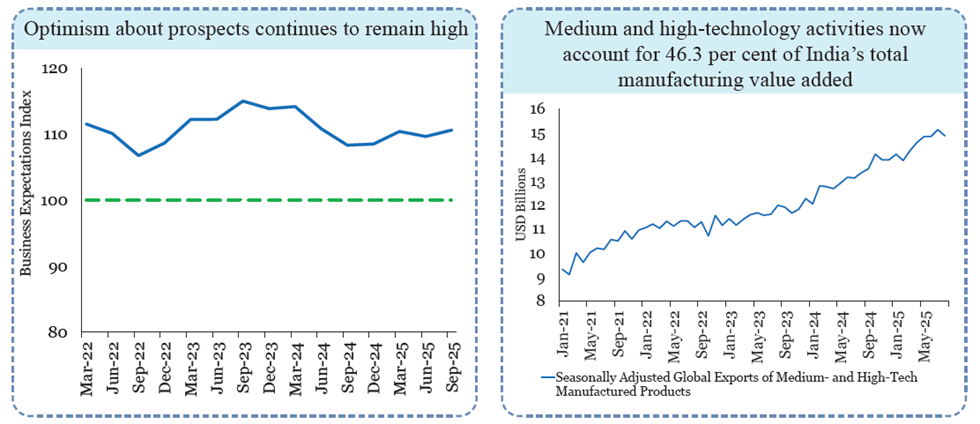

- Medium and high-tech sectors account for 46.3% of manufacturing value added.

- Government initiatives like PLI and semiconductor policies are driving transformation.

- India’s global industrial ranking improved in Competitive Industrial Performance (CIP).

5. Business Sentiment and Forward Indicators

- Manufacturing PMI remains consistently above the expansion threshold of 50.

- Business Expectations Index indicates optimism in output, employment, and investment.

- Firms show confidence in demand conditions and future growth prospects.

- These indicators reflect a stable and positive industrial environment.

6. Structural Pillars of Industrial Competitiveness

- Improving ease of doing business is essential for industrial growth.

- Innovation and R&D investment are critical for long-term competitiveness.

- Skill development is necessary to meet future workforce requirements.

- Infrastructure and logistics improvements help reduce production costs.

- Strengthening MSMEs is crucial for integration into global markets.

7. Industrial Credit Trends

- Bank credit growth to industry moderated but remains positive.

- Industries are increasingly shifting towards market-based financing sources.

- Non-bank financial flows have grown significantly in recent years.

- Diversification of funding sources improves financial stability.

- Corporate bond markets are playing a larger role in industrial financing.

Data & Facts

- Global manufacturing growth: ~0.7% (Q3 2025)

- Industry GVA growth (India): 7.0% (H1 FY26)

- Medium & high-tech share: 46.3% of manufacturing value added

- India’s CIP rank: 37th (2023)

- PMI: Consistently above 50 (expansion zone)

- Bank credit growth to industry: 8.24% (FY25)

- Non-bank financial flows CAGR: ~17.3% (FY20–FY25)

Concepts

- Global Value Chains (GVCs): International production networks where different stages of production occur across countries.

- Manufacturing PMI: An index measuring manufacturing sector activity; above 50 indicates expansion.

- Industrial GVA: Contribution of industry to total economic output.

- High-Tech Manufacturing: Production involving advanced technology and innovation (e.g., electronics, semiconductors).

- Corporate Bonds: Debt instruments issued by companies to raise funds from the market.

Analysis

The global industrial landscape is transitioning from efficiency-driven globalisation to resilience-driven production systems. India’s ability to sustain high industrial growth despite global slowdown reflects strong domestic fundamentals and effective policy support. The shift towards high-tech manufacturing enhances competitiveness but also raises challenges related to skills, innovation capacity, and technological adoption.

The diversification of financing sources indicates a maturing financial ecosystem, reducing systemic risks. However, sustaining this trajectory requires continuous reforms in infrastructure, regulatory frameworks, and human capital development.

POLICY INITIATIVES, MSMEs & GLOBAL INTEGRATION

India’s industrial strategy is undergoing a decisive shift from protection-driven growth to competitiveness, innovation, and global integration. Flagship initiatives like the Production Linked Incentive (PLI) scheme and the National Manufacturing Mission (NMM) aim to expand manufacturing capacity, deepen value chains, and enhance technological capabilities.

Alongside, the innovation ecosystem has strengthened significantly, with improvements in research output, startup activity, and intellectual property generation, although low R&D expenditure remains a key constraint. Infrastructure and logistics reforms—especially through PM Gati Shakti and the National Logistics Policy—are reducing costs and improving efficiency.

MSMEs, forming the backbone of industrial growth, are witnessing improved credit access and digital integration, though financing gaps persist. A crucial strategic shift is toward deeper integration into Global Value Chains (GVCs), particularly through backward linkages that can enhance scale, employment, and domestic value addition.

The roadmap ahead emphasises advanced manufacturing, cluster-based development, innovation-driven growth, and a mission-oriented industrial policy framework. Overall, India’s industrial sector is transitioning toward a resilient, globally competitive, and technology-driven growth model.

Key Points

1. Production Linked Incentive (PLI) Scheme

- The PLI scheme spans 14 sectors with an outlay of ₹1.97 lakh crore to boost manufacturing competitiveness.

- It has attracted investments exceeding ₹2 lakh crore and generated significant employment.

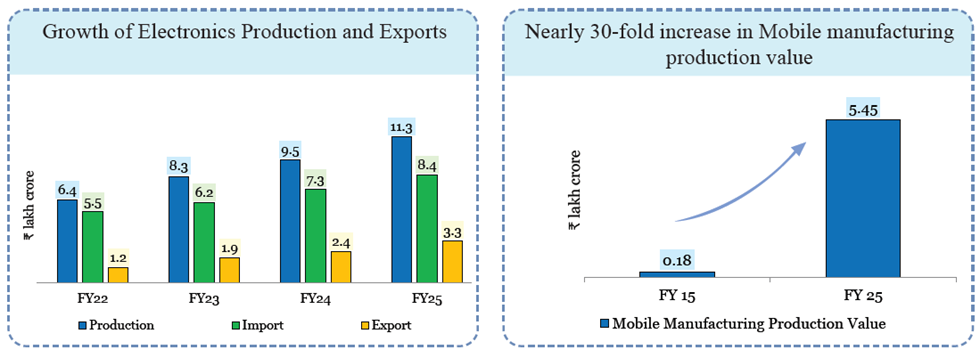

- Incremental production and exports have increased substantially, especially in electronics and pharmaceuticals.

- The scheme promotes economies of scale, efficiency, and technological upgrading.

- It has positioned India as a global hub for sectors like mobile manufacturing.

2. National Manufacturing Mission (NMM)

- NMM aims to raise manufacturing share in GDP to 25% and generate 143 million jobs by 2035.

- It adopts a cluster-based and sector-specific strategy across priority industries.

- The mission categorises sectors into Scale, Fix & Transform, and Seed segments.

- It focuses on MSME integration, innovation, and infrastructure development.

- It acts as a coordinating framework aligning Centre, States, and industry.

3. Innovation and R&D Ecosystem

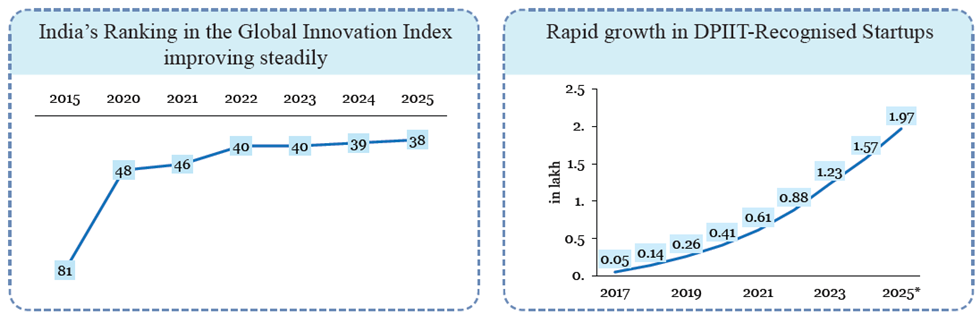

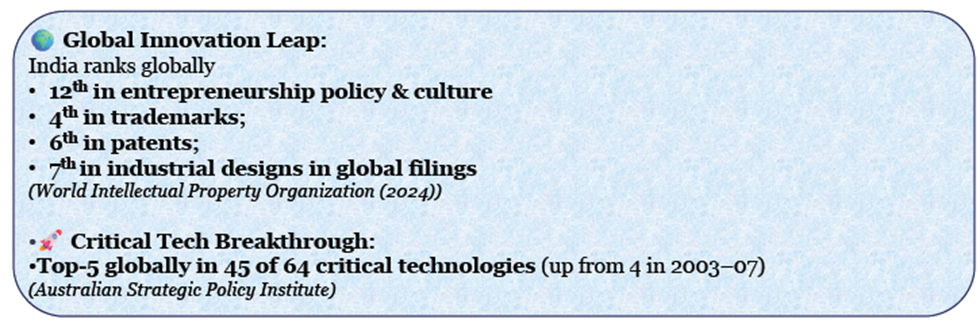

- India ranks 3rd globally in scientific publications and 38th in the Global Innovation Index.

- Startup ecosystem has expanded rapidly with over 2 lakh recognised startups.

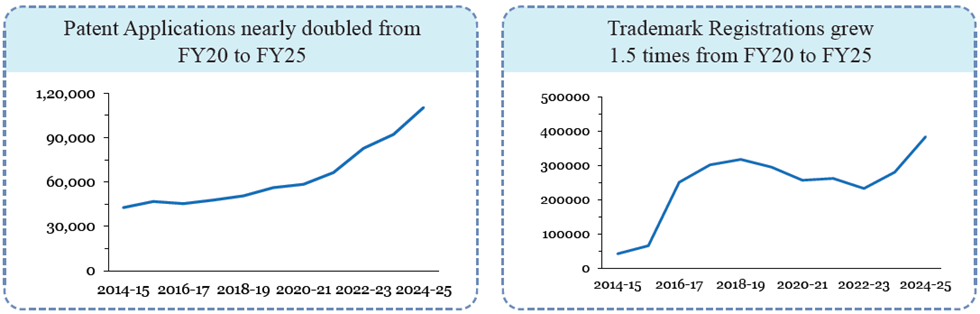

- India has emerged as a global player in patents, trademarks, and design registrations.

- Critical technology capabilities have improved across AI, defence, and advanced materials.

- However, R&D expenditure remains low at around 0.64% of GDP.

4. Government Initiatives for Innovation

- The Anusandhan National Research Foundation (ANRF) provides strategic direction for R&D.

- The ₹1 lakh crore Research, Development and Innovation (RDI) Fund aims to boost private investment.

- National missions such as Semiconductor Mission, AI Mission, and Green Hydrogen Mission are underway.

- These initiatives aim to bridge the gap between research and commercialisation.

5. Quality Control and Standards (QCOs)

- QCOs ensure compliance with quality standards to improve global competitiveness.

- Over 700 products are now covered under mandatory quality standards.

- They help curb substandard imports and protect consumers.

- However, improper implementation can burden MSMEs and disrupt supply chains.

- A balanced and pragmatic approach is required for effective outcomes.

6. Infrastructure and Logistics Reforms

- PM GatiShakti integrates infrastructure planning through a unified digital platform.

- National Logistics Policy and ULIP improve coordination and efficiency.

- Logistics cost has reduced to around 7.97% of GDP, indicating improved efficiency.

- Industrial corridors and smart cities enhance manufacturing ecosystems.

- These reforms reduce transaction costs and improve competitiveness.

7. MSMEs: Backbone of Industrial Growth

- MSMEs contribute ~31% to GDP, ~35% to manufacturing, and ~48% to exports.

- They employ over 32 crore people, making them a key employment generator.

- Credit growth to MSMEs has outpaced large industries.

- Government schemes like CGTMSE, SRI Fund, and PMEGP support financing and growth.

- Digital platforms like ONDC and TReDS enhance market access and liquidity.

8. MSME Challenges and Reforms

- Access to formal credit remains limited, especially for micro enterprises.

- Delayed payments continue to affect liquidity and working capital.

- Informal financing remains prevalent for small-ticket loans.

- Online Dispute Resolution (ODR) and digital lending aim to address these issues.

- Expanding cash-flow-based lending is critical for inclusion.

9. Integration with Global Value Chains (GVCs)

- India’s share in global manufacturing and exports remains relatively low.

- Backward GVC participation can enhance scale, employment, and domestic value addition.

- Tariff rationalisation is necessary to avoid inverted duty structures.

- Global supply chain shifts present opportunities for India.

- Export-oriented manufacturing is key for long-term growth.

10. Role of Advanced Manufacturing

- Advanced manufacturing enforces efficiency, quality, and global competitiveness.

- It drives technological capability and institutional improvement.

- It complements other growth drivers like infrastructure and services.

- It is essential for achieving strategic autonomy and resilience.

11. Industrial Cluster Strategy

- Clusters enhance productivity through agglomeration benefits.

- India needs larger, globally competitive clusters with better connectivity.

- Private sector participation and regulatory flexibility are critical.

- Tier-2 and Tier-3 cities are emerging as new manufacturing hubs.

Data & Facts

- PLI outlay: ₹1.97 lakh crore

- Investment under PLI: ₹2+ lakh crore

- Incremental production: ₹18.7 lakh crore

- R&D expenditure: ~0.64% of GDP

- MSME share: 31% GDP, 35% manufacturing, 48% exports

- Logistics cost: ~7.97% of GDP (FY24)

- India’s global manufacturing share: ~2.9%

- Startup ecosystem: 2 lakh+ startups

Concepts

- PLI Scheme: Incentive scheme rewarding firms based on incremental production.

- GVC (Global Value Chain): International production network with cross-border value addition.

- Backward GVC Participation: Importing inputs to produce exports.

- Quality Control Orders (QCOs): Mandatory standards ensuring product quality.

- Advanced Manufacturing: High-tech, innovation-driven production systems.

Analysis

India’s industrial strategy reflects a transition toward a globally integrated and innovation-driven model. Policies like PLI and NMM are shifting the focus from import substitution to competitiveness and scale. Strengthening MSMEs and improving infrastructure are critical for inclusive industrialisation.

However, challenges such as low R&D investment, credit constraints, and regulatory complexities persist. Integration into GVCs emerges as a key strategy for accelerating growth and employment. The emphasis on advanced manufacturing and clusters indicates a long-term vision of building a resilient and self-reliant industrial ecosystem.

One Comment