Fiscal Deficit, Budget & Government Finances (Economic Survey 2025–26 Explained)

CENTRAL GOVERNMENT FINANCES

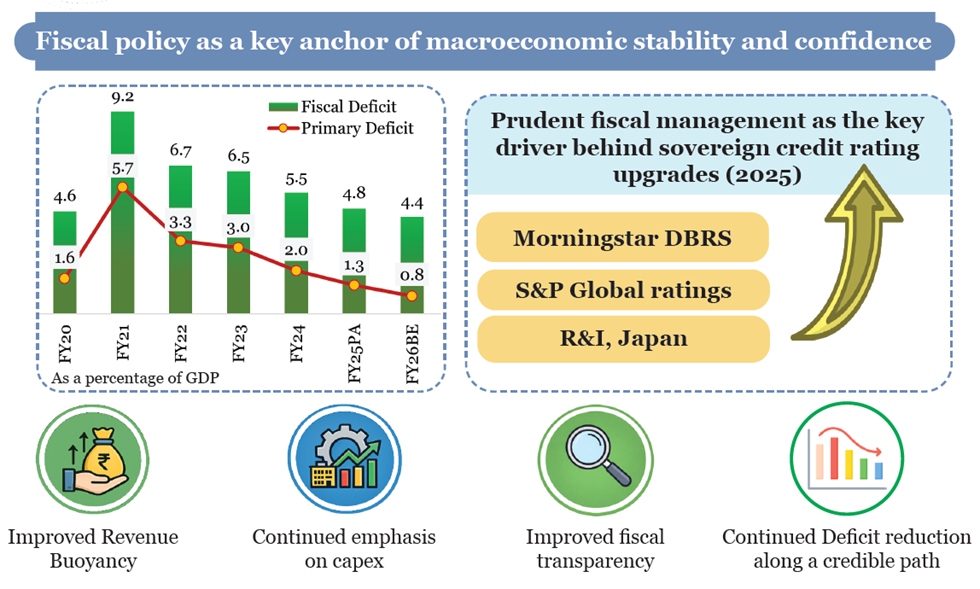

India’s fiscal trajectory in recent years reflects a carefully calibrated balance between growth and fiscal prudence, leading to enhanced macroeconomic stability and global confidence. The recognition of India’s fiscal resilience through sovereign credit rating upgrades underscores the success of sustained policy efforts, including deficit reduction, improved revenue buoyancy, and a structural shift towards capital expenditure.

The government adopted a flexible medium-term consolidation path rather than rigid annual targets, ensuring that growth-enhancing spending was not compromised. Fiscal deficits have declined significantly from pandemic highs, accompanied by improvements in the quality of expenditure, as reflected in reduced revenue deficits and rising capital outlays. Strong revenue performance, driven by tax reforms, improved compliance, and formalisation, has strengthened fiscal capacity.

At the same time, rationalisation of subsidies and efficiency gains through digital governance have created fiscal space for productive investments. Capital expenditure has been scaled up substantially, particularly in infrastructure sectors, reinforcing long-term growth potential. Overall, India’s fiscal policy has emerged as a key anchor of macroeconomic stability, combining credibility, flexibility, and growth orientation in a challenging global environment.

Key Points

1. Fiscal Policy as Anchor of Stability

- Fiscal policy has ensured macroeconomic stability by balancing growth needs with fiscal discipline.

- A medium-term glide path was adopted, targeting fiscal deficit below 4.5% of GDP by FY26.

- Flexibility in fiscal targets allowed continued focus on capital expenditure during uncertain periods.

- Credible fiscal consolidation enhanced investor confidence and sovereign ratings.

2. Trends in Deficit Indicators

- Fiscal deficit declined sharply from 9.2% of GDP (FY21) to 4.8% (FY25) and is budgeted at 4.4% (FY26).

- Revenue deficit reached its lowest level since FY09, improving expenditure quality.

- Decline in primary deficit indicates reduced reliance on fresh borrowing for current expenditure.

- Borrowing is increasingly used for servicing past debt rather than financing consumption.

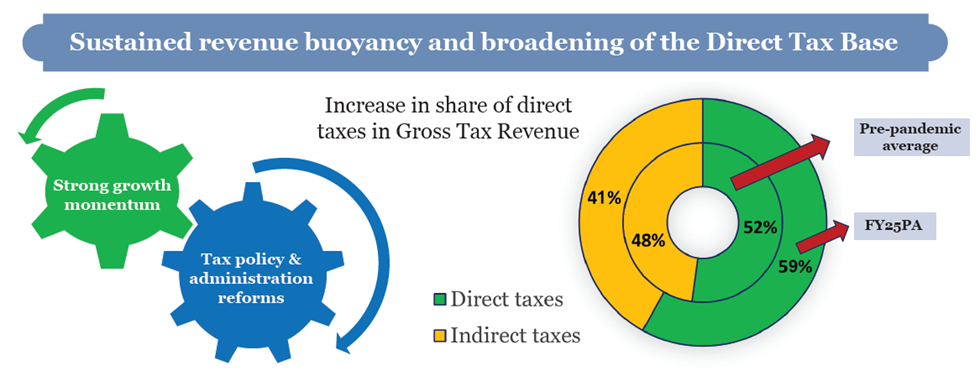

3. Revenue Buoyancy and Fiscal Capacity

- Revenue receipts increased from 8.5% (pre-pandemic) to 9.1% of GDP (post-pandemic).

- Gross tax revenue rose to about 11.5% of GDP due to strong economic growth and reforms.

- Improved tax administration and compliance contributed significantly to revenue gains.

- Revenue buoyancy enabled consolidation without compromising expenditure needs.

4. Expansion of Direct Tax Base

- Share of direct taxes increased to 58.8% of total taxes in FY25.

- Non-corporate taxes (mainly personal income tax) showed strong growth and high buoyancy.

- Number of income tax returns increased from 6.9 crore to 9.2 crore, indicating formalisation.

- Data-driven nudging improved voluntary compliance and reduced litigation.

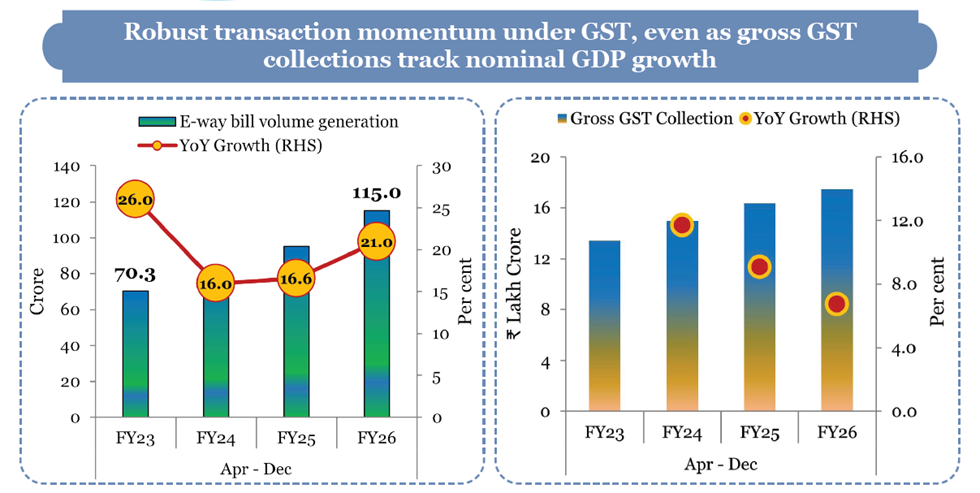

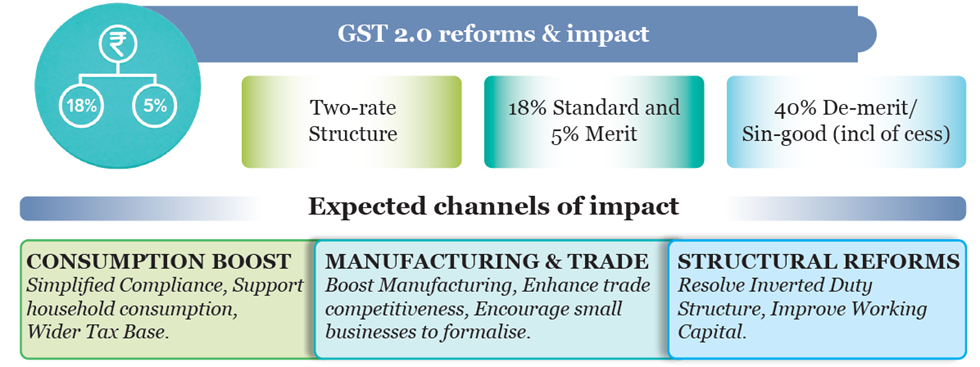

5. Indirect Taxes and GST Performance

- Excise duty collections declined due to tax cuts on petroleum products.

- Customs duty growth remained moderate due to tariff rationalisation and lower global prices.

- GST collections remained robust, reaching ₹17.4 lakh crore (Apr–Dec FY26).

- GST base expanded significantly, with taxpayers rising from 60 lakh to over 1.5 crore.

- GST reforms (GST 2.0) aim to simplify rates, boost consumption, and enhance compliance.

6. Non-Tax Revenue Trends

- Non-tax revenues remained stable at around 1.4% of GDP.

- Dividends and profits surged due to higher RBI surplus and improved PSU performance.

- RBI transferred ₹2.68 lakh crore surplus in FY26, boosting government finances.

- CPSE profitability and dividends increased significantly, reflecting operational efficiency.

7. Non-Debt Capital Receipts and Disinvestment

- Disinvestment focused on market-based transactions such as Offer for Sale (OFS).

- Equity monetisation and InvITs contributed to resource mobilisation.

- Strategic disinvestment progressed gradually, with several CPSE transactions underway.

- Proposal to reduce government ownership threshold could unlock greater monetisation potential.

8. Expenditure Rationalisation

- Revenue expenditure declined from 13.6% (FY22) to 10.9% of GDP (FY25).

- Subsidy expenditure reduced significantly while maintaining welfare commitments.

- Direct Benefit Transfer (DBT) reduced leakages and improved targeting efficiency.

- Committed expenditures like interest, pensions, and salaries limit fiscal flexibility.

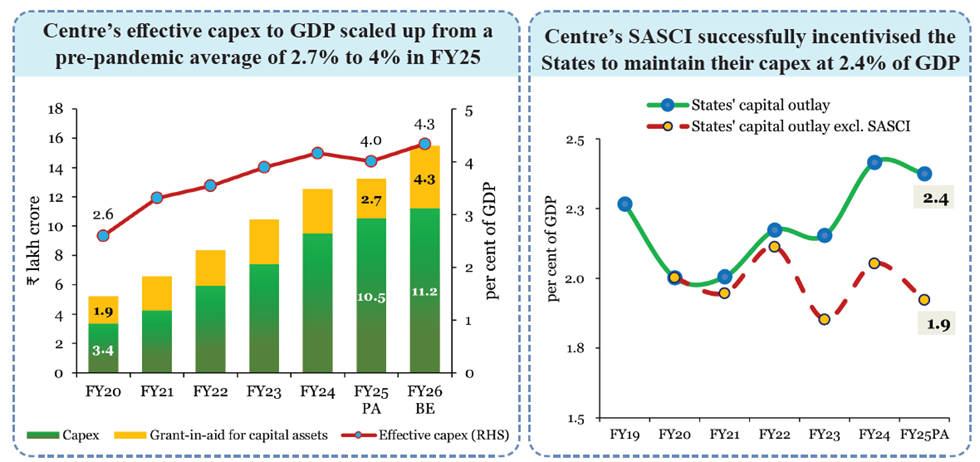

9. Capital Expenditure Push

- Capital expenditure increased from 1.7% to around 2.9% of GDP post-pandemic.

- Effective capex rose to about 4% of GDP, reflecting strong infrastructure investment.

- Major sectors include roads, railways, defence, and urban development.

- Shift from revenue to capital expenditure indicates improved quality of spending.

10. Fiscal Management Reforms

- Just-in-Time (JIT) fund release system reduced idle funds and improved efficiency.

- Digital tools like PFMS and SNA-SPARSH enhanced transparency and accountability.

- Route optimisation in PDS reduced logistics costs and environmental impact.

- Technology-driven governance improved expenditure efficiency and reduced leakages.

Data & Facts

- Fiscal deficit: 9.2% (FY21) → 4.8% (FY25) → 4.4% (FY26 BE)

- Revenue receipts: ~9.1% of GDP (post-pandemic)

- Direct tax share: 58.8% (FY25)

- GST collection (Apr–Dec FY26): ₹17.4 lakh crore

- Income tax returns: 6.9 crore → 9.2 crore

- Non-tax revenue: ~1.4% of GDP

- RBI dividend: ₹2.68 lakh crore (FY26)

- Effective capex: ~4% of GDP

- Subsidy expenditure: 1.9% (FY22) → 1.2% (FY25)

Concepts

- Fiscal Deficit: Total expenditure minus total non-debt receipts of the government.

- Revenue Deficit: Excess of revenue expenditure over revenue receipts.

- Primary Deficit: Fiscal deficit excluding interest payments.

- Tax Buoyancy: Responsiveness of tax revenue to changes in GDP.

- Disinvestment: Sale of government stake in public sector enterprises.

- DBT (Direct Benefit Transfer): Transfer of subsidies directly to beneficiaries’ bank accounts.

Analysis

India’s fiscal strategy reflects a shift from crisis-driven expansion to rule-based consolidation with flexibility. The emphasis on capital expenditure alongside deficit reduction marks a qualitative improvement in fiscal policy. Strong revenue performance and digital governance reforms have enhanced fiscal capacity without increasing tax burden excessively.

However, challenges remain in managing committed expenditures and ensuring sustainable debt levels. The focus on disinvestment, subsidy rationalisation, and efficiency gains indicates a forward-looking approach. Overall, fiscal policy has evolved into a key instrument for sustaining growth while maintaining macroeconomic stability.

OVERVIEW OF STATE GOVERNMENT FINANCES

State finances in India reflect a complex balance between fiscal autonomy, central support, and emerging expenditure pressures. Transfers from the Centre to States have increased significantly, both in absolute terms and as a share of GDP, strengthening fiscal capacity and supporting development.

However, the effectiveness of these transfers depends on their utilisation, with capital expenditure emerging as the most critical driver of long-term growth. While States’ fiscal deficits have remained broadly stable, revenue deficits have increased in recent years due to rising expenditure pressures and relatively slower revenue growth.

Despite these constraints, capital expenditure has been protected, largely due to central support schemes such as interest-free loans for capital investment (SASCI). The revenue composition has improved with higher own tax revenues, reflecting economic recovery and better compliance. However, increasing reliance on unconditional cash transfers and committed expenditures is creating fiscal trade-offs, potentially crowding out productive investment.

Overall, State finances remain stable but face structural challenges, requiring a careful balance between welfare spending, fiscal discipline, and growth-oriented investments.

Key Points

1. Expansion of Centre-State Fiscal Transfers

- Total transfers from the Centre to States more than doubled between FY20 and FY26.

- Transfers increased from 5.7% to 6.9% of GDP, reflecting enhanced fiscal support.

- Components include tax devolution, Finance Commission grants, CSS, and other transfers.

- Increased transfers have expanded fiscal space for States.

2. Role of Finance Commission Grants

- Fifteenth Finance Commission recommended ₹1.48 lakh crore grants for FY26.

- Grants include revenue deficit grants, local body grants, health grants, and disaster relief.

- Effective utilisation of grants is critical for growth outcomes.

- Grants support decentralisation and local governance capacity.

3. Fiscal Devolution and Growth Outcomes

- Capital expenditure is the most significant driver of State-level economic growth.

- Higher transfers alone do not guarantee growth without productive utilisation.

- Fiscal discipline and efficient spending determine long-term outcomes.

- Investment-led spending yields more durable income and welfare gains.

4. Borrowing Flexibility for States

- Net borrowing ceiling set at 3% of GSDP, with additional 0.5% for power sector reforms.

- Additional borrowing allowed for contributions under the National Pension System.

- Borrowing flexibility incentivises reforms and sectoral efficiency improvements.

5. Trends in State Fiscal Performance

- Fiscal deficit remained stable around 2.8% of GDP but increased to 3.2% recently.

- Revenue deficit increased from 0.1% (FY19) to 0.7% (FY25), indicating fiscal stress.

- Rising expenditure pressures and slower revenue growth contributed to deficits.

- Number of revenue-surplus States declined significantly.

6. Revenue Composition of States

- States’ own tax revenue is the largest source, accounting for about 50% of total revenue.

- Share in central taxes contributes around 32%, followed by grants and non-tax revenue.

- Own tax revenues grew strongly, indicating improved fiscal capacity.

- Total revenue receipts as a share of GDP declined, constraining fiscal space.

7. Role of SASCI in Supporting Capex

- Special Assistance to States for Capital Investment provides interest-free loans.

- Allocation increased from ₹12,000 crore (FY21) to ₹1.5 lakh crore (FY26).

- SASCI helped maintain capital expenditure despite revenue pressures.

- Scheme plays a key role in preventing pro-cyclical reduction in investment.

8. Expenditure Trends and Quality

- Total State expenditure remained stable around 15–16% of GDP.

- Revenue expenditure dominates, accounting for around 84% of total expenditure.

- Increasing share of unconditional cash transfers is altering expenditure composition.

- Higher revenue spending reduces fiscal space for capital investment.

9. Fiscal Trade-offs of Cash Transfers

- Unconditional cash transfers are expanding rapidly across States.

- These transfers provide short-term welfare benefits but raise fiscal sustainability concerns.

- Evidence suggests limited long-term impact on productivity and human capital.

- Rising revenue expenditure may crowd out capital expenditure and affect growth.

10. Trends in FY26 (Current Year)

- Revenue growth moderated to around 6.6% in FY26 (Apr–Nov).

- Revenue deficit overshot budget estimates due to slower revenue growth.

- Capital expenditure rebounded but lagged behind budgeted targets.

- States face pressure to balance fiscal discipline with expenditure needs.

Data & Facts

- Transfers to States: ₹11.5 lakh crore (FY20) → ₹25.6 lakh crore (FY26 BE)

- Transfers as % of GDP: 5.7% → 6.9%

- State fiscal deficit: ~2.8% → 3.2% of GDP

- Revenue deficit: 0.1% (FY19) → 0.7% (FY25)

- SASCI allocation: ₹12,000 crore → ₹1.5 lakh crore

- States’ own tax revenue share: ~50% of total revenue

- Total State expenditure: ~15.4% of GDP

Concepts

- Fiscal Devolution: Transfer of financial resources from the Centre to States.

- GSDP (Gross State Domestic Product): Total economic output of a State.

- Revenue Deficit (States): Excess of revenue expenditure over revenue receipts.

- SASCI: Scheme providing interest-free loans to States for capital expenditure.

- Unconditional Cash Transfers (UCTs): Direct cash payments without conditions.

Analysis

State finances reflect a growing tension between welfare expansion and fiscal sustainability. While increased transfers and schemes like SASCI have strengthened fiscal capacity and protected capital expenditure, rising revenue deficits and expanding cash transfer programmes pose long-term risks. The evidence clearly indicates that growth outcomes depend more on capital expenditure than on the volume of transfers.

Therefore, maintaining fiscal discipline and prioritising investment-led spending is essential. The challenge ahead lies in balancing short-term welfare needs with long-term growth objectives, ensuring that fiscal policy at the State level remains both sustainable and growth-oriented.

DEBT PROFILE OF THE GOVERNMENT & GENERAL GOVERNMENT FINANCES

India’s debt management strategy reflects a prudent and growth-oriented approach, balancing cost minimisation, risk mitigation, and market development. The Central Government aims to reduce its debt-to-GDP ratio to around 50% by FY31, signalling a shift toward a more credible and flexible fiscal framework.

Debt composition is dominated by domestic, long-term, fixed-rate instruments, which reduces rollover, interest rate, and currency risks. At the State level, rising debt and fiscal pressures highlight inter-state disparities, though market pricing does not adequately reflect fiscal performance differences.

At the aggregate level, general government finances show a clear post-pandemic consolidation trend, with declining debt ratios and improving fiscal discipline. India stands out among emerging economies for achieving debt reduction while sustaining growth, supported by a strong public investment push. Evidence suggests that India’s fiscal policy is sustainable, as governments respond to rising debt with corrective measures over time.

However, maintaining sustainability requires continued fiscal discipline, efficient public investment, and coordinated Centre-State action. Overall, India’s fiscal framework demonstrates that growth-friendly consolidation is achievable even in a volatile global environment.

Key Points

1. Central Government Debt Strategy

- Debt management is guided by minimising borrowing costs, mitigating risks, and supporting G-sec markets.

- Medium-term target is to reduce debt-to-GDP ratio to 50 ± 1% by FY31.

- Debt consolidation has strengthened fiscal credibility post-pandemic.

- Flexible fiscal framework is preferred over rigid deficit targets in uncertain conditions.

2. Composition and Cost of Debt

- Marketable securities (G-secs and T-bills) constitute about 65% of total liabilities.

- Weighted average maturity (WAM) is around 19 years, reducing rollover risk.

- Weighted average coupon (WAC) declined to ~6.65% in FY26, lowering borrowing costs.

- Strategic issuance across maturities helps stabilise yields and borrowing conditions.

3. Risk Management in Public Debt

- Rollover risk is low, with only ~27% of debt maturing in the next five years.

- Interest rate risk is limited due to dominance of fixed-rate debt (~96%).

- External debt exposure is minimal (~2.6% of GDP), reducing currency risk.

- Debt profile ensures stability against global financial volatility.

4. State-Level Debt Dynamics

- Combined State debt stands at ~28.1% of GDP (FY25).

- Interest payments to revenue receipts ratio is around 12.6%.

- Significant variation exists across States in fiscal health.

- Borrowing costs do not adequately reflect fiscal discipline differences.

- Improved transparency and market development are needed for better risk pricing.

5. General Government Finances

- Combined (Centre + States) debt and deficits are on a consolidation path post-pandemic.

- General government debt declined by ~7.1 percentage points since 2020.

- India’s performance compares favourably with global peers, especially EMEs.

- Fiscal consolidation is being achieved alongside sustained economic growth.

6. Debt Sustainability Framework

- Fiscal Response Function (FRF) shows that fiscal policy responds positively to rising debt.

- Higher debt leads to corrective measures such as improved primary balance.

- Fiscal policy in India is counter-cyclical and institutionally driven.

- Debt sustainability is supported by strong growth and fiscal discipline.

7. Public Investment and Growth

- General government investment is about 4% of GDP, relatively high globally.

- India allocates a larger share of revenue to capital expenditure compared to peers.

- Public investment enhances productivity, crowds in private investment, and boosts growth.

- Growth-led debt sustainability is a key feature of India’s fiscal model.

8. Fiscal Challenges at State Level

- Rising revenue deficits and unconditional cash transfers pose fiscal risks.

- High committed expenditure limits fiscal flexibility.

- Fiscal indiscipline at State level can increase sovereign borrowing costs.

- Need for better coordination between Centre and States.

9. Future Fiscal Reforms

- GST 2.0 and personal income tax reforms aim to improve efficiency and compliance.

- Digitalisation of public finance will enhance transparency and reduce leakages.

- Strengthening local bodies can improve grassroots fiscal efficiency.

- Sixteenth Finance Commission will shape future fiscal federalism.

Data & Facts

- Central debt target: ~50% of GDP by FY31

- Marketable securities: ~65% of total liabilities

- WAM: ~19 years

- WAC: ~6.65% (FY26)

- Debt maturing in 5 years: ~27%

- Sovereign External debt: ~2.6% of GDP

- State debt: ~28.1% of GDP

- General government debt reduction: ~7.1 percentage points since 2020

- Public investment: ~4% of GDP

Concepts

- Debt-to-GDP Ratio: Indicator of a country’s debt burden relative to its economic output.

- G-Sec (Government Security): Debt instrument issued by the government to borrow funds.

- Weighted Average Maturity (WAM): Average time to maturity of debt instruments.

- Fiscal Response Function (FRF): Relationship between debt levels and fiscal policy response.

- General Government: Combined fiscal position of Centre and State governments.

Analysis

India’s debt framework reflects a mature and adaptive fiscal strategy that prioritises sustainability without compromising growth. The shift toward a debt anchor instead of rigid fiscal deficit targets indicates pragmatic policymaking in a volatile global environment. Strong reliance on domestic, long-term borrowing has insulated the economy from external shocks.

At the same time, the emphasis on public investment has strengthened growth prospects, making debt more sustainable. However, rising fiscal pressures at the State level and increasing revenue expenditure pose risks to long-term stability. Ensuring coordinated fiscal discipline and maintaining the quality of expenditure will be critical for sustaining this trajectory.

One Comment