CHAPTER 1: STATE OF THE ECONOMY (Economic Survey 2025-26)

GLOBAL ECONOMIC GROWTH – FRAGILE AND DIVERGING

The global economy during 2025–26 has remained resilient in the short term despite multiple disruptions, particularly the imposition of tariffs by the United States. Initial concerns regarding slower growth and higher inflation proved temporary due to mitigating factors such as trade adjustments, delayed tariff implementation, and pre-emptive spending by firms and households.

While global growth projections stabilised, underlying vulnerabilities persist across regions. The United States has driven growth through strong investment in artificial intelligence, but inflation remains above target and unemployment is rising.

Europe exhibits mixed growth trends, while China faces deflationary pressures due to weak domestic demand despite strong exports. Monetary policy across countries is diverging due to varying growth-inflation dynamics, influencing global capital flows.

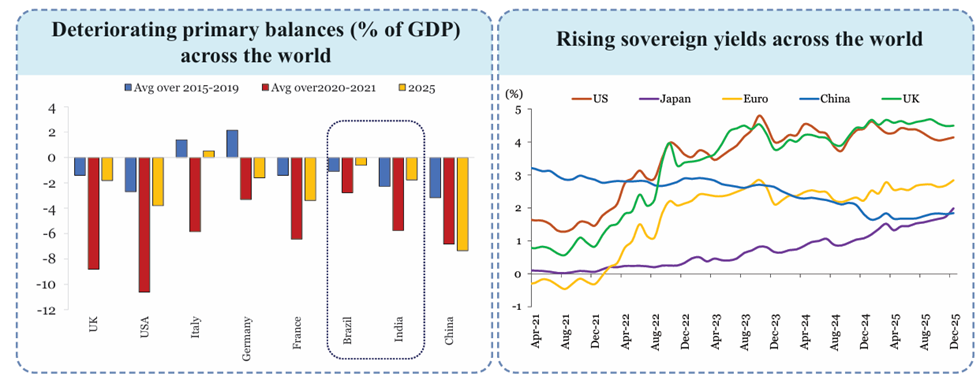

Fiscal policies remain expansionary, with high deficits and elevated sovereign bond yields indicating fiscal stress. Additionally, global uncertainty, geopolitical fragmentation, and declining foreign direct investment flows reflect structural weaknesses. The resurgence of economic statecraft highlights a shift where economic tools are increasingly used for strategic and geopolitical objectives.

In this evolving global order, countries, including India, must focus on building resilience and achieving strategic indispensability to safeguard long-term economic interests.

Key Points

1. Short-term Stability vs Structural Fragility

- Global growth remained stable in the short term despite tariff shocks due to adaptive trade and investment behaviour.

- Advanced economies experienced slightly better-than-expected growth, primarily driven by the United States.

- Emerging market and developing economies showed improved growth projections compared to earlier estimates.

- Inflation in advanced economies remained persistently high, while it declined in emerging economies.

- Aggregate global indicators conceal significant regional disparities and structural weaknesses.

2. Regional Growth Divergence

- The United States experienced strong growth driven by artificial intelligence-related investments.

- European economies showed mixed growth, with Spain outperforming while major economies remained moderate.

- China faced deflationary pressures due to weak domestic demand despite strong export performance.

- Japan recorded moderate growth but continued to experience inflation above its target.

- Regional divergence reflects uneven recovery and structural challenges across economies.

3. Monetary and Financial Trends

- Central banks are gradually shifting from tight monetary policy to neutral or accommodative stances.

- Divergence in inflation and growth has led to varied policy rate trajectories across countries.

- Differences in interest rates are influencing global capital flows in search of higher returns.

- Financial conditions remain uncertain due to inconsistent macroeconomic signals.

4. Fiscal Stress and Debt Concerns

- Fiscal policies remain expansionary, with deficits higher than pre-pandemic levels in most economies.

- Rising public debt has led to elevated long-term borrowing costs globally.

- Sovereign bond yields, especially long-term yields, have increased significantly.

- Investor concerns regarding fiscal sustainability have reduced demand for long-duration bonds.

5. Global Uncertainty and FDI Trends

- Geopolitical fragmentation and policy uncertainty continue to remain elevated.

- Global FDI flows declined significantly, reflecting weakened investor confidence.

- Investment is increasingly concentrated in sectors such as semiconductors and AI.

- Developed economies saw declining FDI inflows, except for the United States.

6. Rise of Economic Statecraft

- Economic tools are increasingly used for strategic and geopolitical objectives rather than purely economic goals.

- Countries are prioritising national security, supply chain resilience, and technological dominance.

- Trade restrictions, export controls, and sanctions have become common instruments of policy.

- Strategic sectors such as semiconductors, critical minerals, and renewable energy are receiving state support.

- Nations are shifting towards friend-shoring and near-shoring to reduce geopolitical risks.

Data & Facts

- Global growth for 2025 stabilised around 3.3%, with EMDEs outperforming advanced economies.

- EMDEs means Emerging Market and Developing Economies

- Inflation in advanced economies remained about 40 basis points higher than initial projections.

- FDI flows declined by 11% in 2024 (YoY) excluding conduit economies.

- Conduit economies are financial hubs (like Luxembourg, Singapore, Netherlands) where FDI often just “passes through” without creating real productive assets. Excluding them gives a clearer picture of genuine investment flows.

- US 30-year bond yields reached around 5.15% in 2025, the highest since 2007.

- AI-related investments accounted for nearly half of US GDP growth in recent quarters.

Concepts

- Economic Statecraft: The use of economic tools such as trade, finance, and investment to achieve geopolitical or strategic objectives.

- FDI (Foreign Direct Investment): Investment made by a firm or individual in one country into business interests in another country.

- Primary Deficit: Fiscal deficit excluding interest payments on past debt.

- Bond Yield: The return earned by investors on government or corporate bonds.

- Friend-shoring: Shifting supply chains to politically allied countries to reduce geopolitical risk.

Analysis

The current global economic phase reflects a transition from globalisation driven by efficiency to one shaped by security and resilience. While short-term stability has been achieved through adaptive responses, deeper structural issues such as fiscal stress, geopolitical fragmentation, and uneven growth persist.

The divergence in monetary policy and capital flows indicates increasing financial volatility. Moreover, the resurgence of economic statecraft signals a paradigm shift where economic interdependence is no longer seen purely as beneficial but also as a source of vulnerability. This transformation is likely to reshape global trade, investment patterns, and institutional frameworks in the coming years.

TRENDS IN THE DOMESTIC ECONOMY

India’s domestic economy in FY26 demonstrates strong and broad-based growth momentum despite global uncertainties.

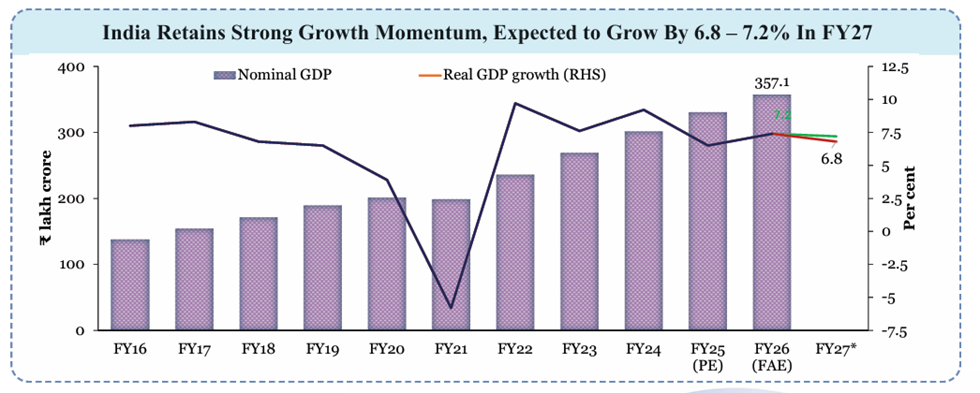

According to the First Advance Estimates (FAE), real GDP growth is projected at 7.4%, reaffirming India’s position as the fastest-growing major economy.

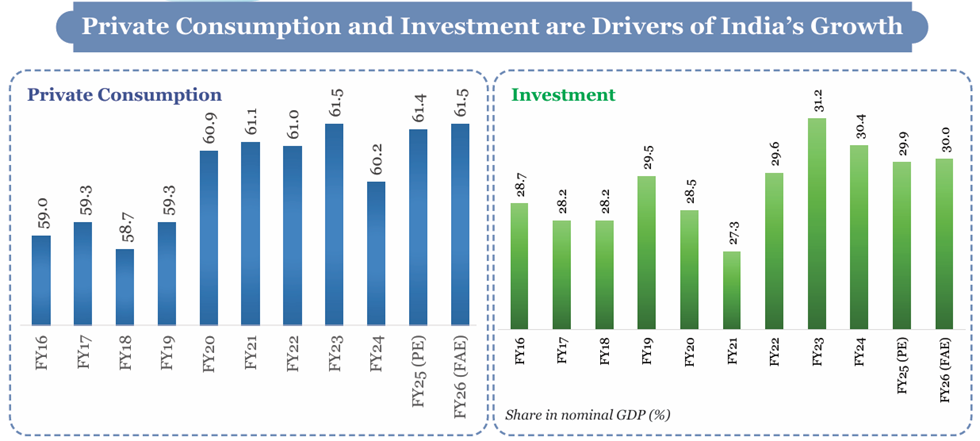

Growth is primarily driven by robust domestic demand, particularly private consumption and investment. Consumption demand has strengthened due to low inflation, rising real incomes, and supportive tax policies, while investment activity is buoyed by public capital expenditure and revival in private sector investment.

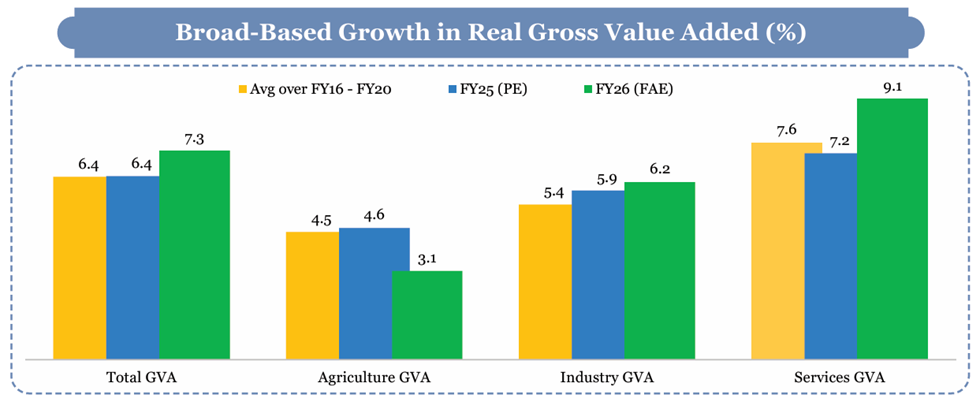

On the supply side, services and industry are the key growth drivers, with manufacturing showing strong expansion and services maintaining its role as the stabilising pillar. Agriculture provides steady support, though growth remains structurally constrained by volatility in crop output.

External demand has also contributed modestly, supported by resilient services exports. High-frequency indicators across sectors confirm sustained economic momentum.

Overall, the Indian economy reflects a healthy balance between consumption, investment, and sectoral growth, indicating resilience and strengthening macroeconomic fundamentals.

Key Points

1. Overall Growth Performance

- Real GDP growth for FY26 is estimated at 7.4%, while GVA growth stands at 7.3%.

- India remains the fastest-growing major economy for the fourth consecutive year.

- Growth is supported by both demand-side and supply-side factors.

- Domestic demand continues to be the primary driver of economic expansion.

2. Demand-Side Drivers

Private Consumption (PFCE)

- Private consumption remains the largest contributor, accounting for about 61.5% of GDP.

- Consumption growth is supported by low inflation, rising incomes, and stable employment.

- Rural consumption is strengthened by agricultural performance, while urban demand is improving due to tax rationalisation.

- High-frequency indicators such as vehicle sales and UPI transactions confirm strong consumption demand.

Investment (GFCF)

- Investment share remains robust at around 30% of GDP.

- Gross fixed capital formation grew by 7.6% in H1 FY26, above pre-pandemic trends.

- Public capital expenditure and rising private investment announcements are key drivers.

- Indicators such as capital goods imports and credit growth signal a strengthening investment cycle.

External Demand

- Exports of goods and services grew by 5.9% in H1 FY26.

- Services exports provide stability, offsetting volatility in merchandise exports.

- Export share in GDP remains stable despite global uncertainties.

3. Supply-Side Performance

Agriculture

- Agriculture is expected to grow by 3.1% in FY26.

- Growth is supported by favourable monsoon and strong allied activities like livestock and fisheries.

- Crop output remains volatile, reflecting structural productivity constraints.

- Rabi sowing and reservoir levels indicate positive outlook for H2 FY26.

Industry

- Industrial growth is estimated at 6.2% in FY26.

- Manufacturing grew strongly at 8.4% in H1 FY26, driven by demand and capacity utilisation.

- Construction activity remains robust due to infrastructure investment.

- Mining sector contracted due to weather-related disruptions.

- Manufacturing share remains stable in real terms, despite decline in nominal share.

Services

- Services sector growth is estimated at 9.1% in FY26.

- It remains the largest contributor to GDP, with a share above 50%.

- Key segments such as financial services and public administration show strong growth.

- High-frequency indicators like PMI services and freight traffic confirm continued momentum.

4. High-Frequency Indicators (HFIs)

- Indicators such as automobile sales, UPI transactions, and air traffic show strong consumption trends.

- Investment indicators like credit growth and capital goods imports signal expansion.

- Industrial indicators such as IIP and PMI reflect strengthening manufacturing activity.

- Services indicators like port traffic and railway freight confirm sustained sectoral performance.

5. Nowcasting and Data Systems

- Nowcasting models use high-frequency indicators to estimate real-time GDP growth.

- The model estimates Q3 FY26 growth at around 7%.

- India is strengthening its statistical system through new surveys, rebasing, and digital platforms.

- Enhanced data availability improves policymaking and economic monitoring.

Data & Facts

- GDP growth (FY26): 7.4%

- GVA growth (FY26): 7.3%

- PFCE share: ~61.5% of GDP (highest since FY12)

- GFCF share: ~30% of GDP

- Services share: ~51% of GDP

- Agriculture growth: 3.1%

- Industry growth: 6.2%

- Services growth: 9.1%

- Nowcast GDP growth (Q3 FY26): ~7%

Concepts

- GDP (Gross Domestic Product): Total value of goods and services produced in an economy.

- GVA (Gross Value Added): Value of output minus intermediate consumption; sector-wise contribution to GDP.

- PFCE: Private Final Consumption Expenditure → Household consumption expenditure on goods and services.

- GFCF: Gross Fixed Capital Formation → Investment in fixed assets such as infrastructure and machinery.

- Nowcasting: Estimating current economic conditions using high-frequency data before official data is released.

Analysis

The domestic economy in FY26 reflects a balanced and resilient growth structure driven by strong internal demand and improving investment cycles. The dominance of consumption ensures stability, while rising investment signals future growth potential. The services sector continues to anchor growth, but the strengthening of manufacturing is a positive structural shift.

However, agriculture’s modest growth highlights persistent structural issues. The increasing use of high-frequency data and nowcasting indicates a shift toward more dynamic and responsive policymaking. Overall, the economy is transitioning towards a more investment-driven and structurally robust growth model.

ASSESSMENT OF DOMESTIC MACROECONOMIC FUNDAMENTALS

India’s macroeconomic fundamentals in FY26 remain strong and well-balanced, supported by easing inflation, prudent fiscal management, effective monetary transmission, and a stable external sector. Inflation has moderated significantly, primarily due to a sharp decline in food prices, improving real incomes and boosting consumption demand.

Fiscal policy has combined consolidation with growth, marked by strong revenue mobilisation and a shift towards capital expenditure, enhancing the quality of spending. Monetary policy has complemented this through rate cuts and liquidity support, leading to improved credit conditions and a healthier banking system.

The external sector remains stable, with a moderate current account deficit and strong foreign exchange reserves, although challenges such as currency depreciation and volatile capital flows persist.

Meanwhile, labour market indicators show improvement, driven by structural reforms, labour codes, and skill development initiatives. Social sector progress is evident in declining poverty and improving human development indicators.

Overall, India’s macroeconomic framework reflects resilience, stability, and a transition towards sustainable and inclusive growth, even in a challenging global environment.

Key Points

1. Inflation Dynamics

- Headline CPI inflation declined sharply to around 1.7%, mainly due to falling food prices.

- Disinflation was supported by favourable agricultural conditions and supply-side interventions.

- Core inflation remains somewhat persistent but is softer when excluding gold and silver prices.

- Lower inflation has enhanced real purchasing power and supported consumption demand.

- The inflation outlook remains benign but requires monitoring of global commodity prices.

2. Fiscal Policy and Public Finance

- Fiscal strategy focused on balancing consolidation with growth-oriented expenditure.

- Strong tax collections were recorded, with direct taxes reaching about 53% of the annual target by November 2025.

- GST collections remained robust, reflecting strong economic activity.

- Capital expenditure increased significantly, improving the quality of public spending.

- Fiscal deficit is on track to reach the target of 4.4% of GDP in FY26.

3. Shift Towards Capital Expenditure

- Capital spending share increased from about 12.5% (FY20) to 22.6% (FY25).

- Effective capital expenditure rose from 2.6% to 4.0% of GDP.

- The central government incentivised states to maintain capital spending through targeted schemes.

- Rising revenue expenditure in states due to cash transfers poses long-term fiscal risks.

4. Monetary Policy and Financial Sector

- Policy repo rate was reduced by 125 basis points since February 2025.

- Liquidity was injected through CRR cuts, open market operations, and forex swaps.

- Lending rates declined, improving credit accessibility.

- Banking sector health improved with low NPAs (~2.2%) and strong profitability.

- Monetary transmission has strengthened the effectiveness of policy measures.

5. Changing Credit Landscape

- Non-food bank credit growth remained stable at around 11–12%.

- Corporates increasingly rely on non-bank sources such as capital markets and internal funds.

- Flow of financial resources from non-bank sources increased significantly (29.3% YoY).

- Reduced dependence on bank credit reflects financial market deepening.

6. External Sector Stability

- Total exports remained strong, with services exports providing stability.

- Current account deficit remained moderate at around 0.8% of GDP (H1 FY26).

- Forex reserves remain adequate, covering over 11 months of imports.

- FDI inflows increased, but FPI flows remained volatile due to global uncertainties.

- The rupee depreciated by about 6.5% but remained orderly.

7. Emerging External Challenges

- Rising trade deficits are offset by services exports and remittances.

- Geopolitical factors and trade restrictions may impact exports in the medium term.

- Migration restrictions may affect remittance inflows.

- Enhancing global competitiveness is critical for long-term stability.

8. Labour Market Developments

- Labour market conditions improved with declining unemployment rates.

- Labour force participation remained stable.

- Labour Codes aim to simplify regulations and improve labour market flexibility.

- Recognition of gig workers marks progress in formalising new forms of employment.

- Skill development initiatives are improving employability.

9. Social Sector Progress

- Poverty levels declined, with extreme poverty estimated at around 5.3%.

- Improvements observed in life expectancy, education, and health indicators.

- Welfare schemes and reforms have enhanced inclusive growth.

- Human capital development is strengthening long-term economic resilience.

Data & Facts

- CPI inflation: ~1.7% (FY26 Apr–Dec)

- Fiscal deficit target: 4.4% of GDP (FY26)

- Capital expenditure share: 22.6% of total expenditure (FY25)

- Repo rate cut: 125 basis points (2025)

- NPAs: ~2.2% (multi-decade low)

- Current account deficit: ~0.8% of GDP (H1 FY26)

- Forex reserves: Cover >11 months of imports

- Rupee depreciation: ~6.5% (FY26)

- Extreme poverty: ~5.3% (2022-23, revised WB line)

Concepts

- Headline Inflation: Overall inflation including food and fuel prices.

- Core Inflation: Inflation excluding volatile items like food and fuel.

- Fiscal Deficit: Difference between government expenditure and revenue.

- Current Account Deficit (CAD): Excess of imports over exports in goods, services, and transfers.

- Monetary Transmission: Process through which policy rate changes affect the economy.

Analysis

India’s macroeconomic fundamentals in FY26 reflect a rare combination of stability, growth, and structural improvement. The decline in inflation alongside strong growth indicates effective policy coordination.

Fiscal policy has improved the quality of expenditure by prioritising capital investment, while monetary policy has supported growth without triggering inflationary pressures. The financial sector’s improved health and diversification of credit sources indicate deeper financial maturity.

However, external vulnerabilities such as currency depreciation and volatile capital flows highlight the need for strengthening export competitiveness and reducing dependence on foreign capital. Overall, the economy is moving towards a more resilient and sustainable growth trajectory.

OUTLOOK AND WAY FORWARD (FY27 AND BEYOND)

The outlook for the Indian economy in FY27 is characterised by steady growth amid persistent global uncertainties. FY26 witnessed significant external challenges, including tariff disruptions and global trade instability, but policy responses such as GST rationalisation and deregulation have strengthened domestic fundamentals.

While the global economy is expected to remain fragile with downside risks such as financial instability from AI-led investments and prolonged trade conflicts, India faces these as manageable external uncertainties rather than immediate threats. Strong domestic drivers, including resilient consumption, improving private investment, low inflation, and healthy balance sheets across sectors, provide a stable foundation for growth.

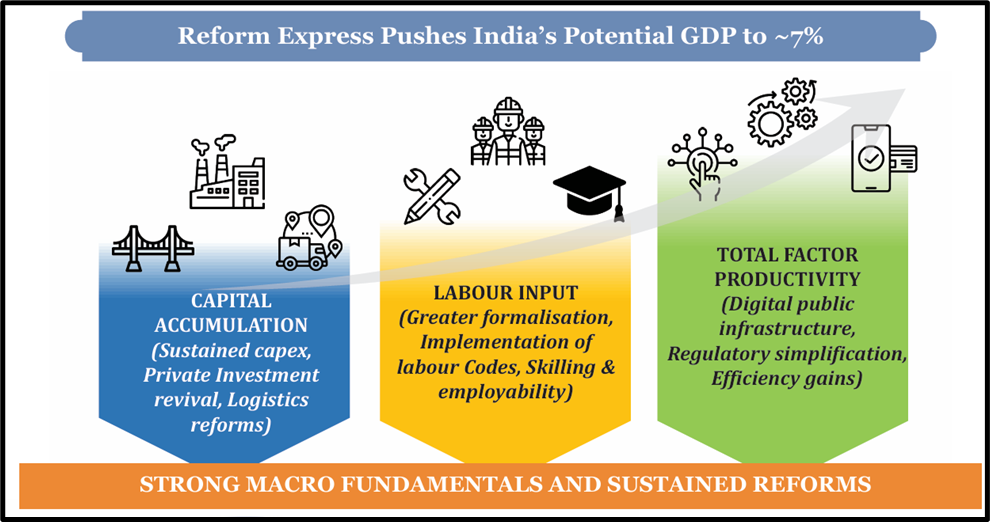

Structural reforms undertaken in recent years have enhanced India’s medium-term growth potential to around 7%. Consequently, real GDP growth for FY27 is projected in the range of 6.8% to 7.2%. The overall outlook emphasises cautious optimism, where maintaining macroeconomic stability, strengthening buffers, and continuing reforms are essential for sustaining growth in a volatile global environment.

Key Points

1. FY26 Experience and Transition to FY27

- FY26 was marked by global trade disruptions and tariff-related uncertainties affecting business confidence.

- Policy reforms such as GST rationalisation and deregulation were accelerated in response.

- FY27 is expected to be a transition year with adaptation by firms and households.

- Domestic demand and investment are expected to strengthen further.

2. Global Economic Outlook

- Global growth is expected to remain modest with persistent downside risks.

- Inflation is easing globally, leading to a more accommodative monetary stance.

- Risks include potential correction in AI-driven asset bubbles and prolonged trade conflicts.

- The global environment remains fragile, with uncertainty as a structural feature.

3. Implications for India

- External risks may affect exports, capital flows, and investor sentiment.

- Trade negotiations, particularly with the United States, may reduce uncertainty.

- External challenges are manageable due to strong domestic fundamentals.

- Maintaining policy credibility and adequate buffers is essential.

4. Domestic Strengths Supporting Growth

- Inflation remains low, supporting purchasing power and demand.

- Balance sheets of households, firms, and banks are healthy.

- Public investment continues to drive economic activity.

- Private investment intentions are improving, indicating a strengthening cycle.

5. Growth Projections

- India’s potential growth has increased to around 7% due to sustained reforms.

- Real GDP growth for FY27 is projected at 6.8% to 7.2%.

- Growth outlook is stable with balanced risks.

- Emphasis is on cautious optimism rather than pessimism.

6. Medium-Term Growth Potential

Drivers of Higher Potential Growth

- Sustained public capital expenditure and infrastructure expansion.

- Manufacturing push through initiatives like PLI and FDI liberalisation.

- Improved corporate and banking sector balance sheets.

- Rising formalisation of employment and better labour market conditions.

- Digital public infrastructure enhancing efficiency and productivity.

Growth Accounting Insights

- Growth is driven by capital, labour, and total factor productivity (TFP).

- Capital formation is strengthening due to public and private investment.

- Labour input is improving due to higher participation and formalisation.

- TFP is rising due to digitalisation, reforms, and better resource allocation.

7. Policy Priorities Ahead

- Maintain macroeconomic stability and fiscal discipline.

- Strengthen export competitiveness and global integration.

- Continue structural reforms in manufacturing, labour, and finance.

- Build resilience against global shocks through buffers and diversification.

- Enhance coordination between Centre and States for sustained growth.

Data & Facts

- FY27 GDP growth projection: 6.8% – 7.2%

- India’s potential growth: ~7% (revised upward)

- Capital expenditure: ~4% of GDP (recent years)

- Capital share in growth: ~0.49 (KLEMS data)

- Labour input growth expected to stabilise above pre-pandemic levels

Concepts

- Potential Growth Rate: The maximum sustainable growth rate an economy can achieve without inflationary pressure.

- Total Factor Productivity (TFP): Efficiency with which capital and labour are used in production.

- Growth Accounting: Method to decompose growth into contributions from capital, labour, and productivity.

- Capital Deepening: Increase in capital per worker leading to higher productivity.

- Policy Credibility: Trust in government policies that ensures stable economic expectations.

Analysis

The outlook highlights a shift from short-term crisis management to long-term capacity building. India’s growth resilience is increasingly rooted in domestic drivers rather than external conditions. The upward revision in potential growth reflects the cumulative impact of structural reforms, digital infrastructure, and improved macro-financial stability.

However, global uncertainties necessitate a cautious approach, particularly regarding exports and capital flows. The emphasis on buffers, policy credibility, and institutional coordination indicates a move towards a more resilient economic framework. Sustaining this trajectory will depend on continued reforms and effective governance.

One Comment