Introduction to Economics

What Is Economics?

Economics is a social science because it studies human behaviour in society, not in isolation. At its heart lies one fundamental problem: scarcity.

- Human wants are unlimited

People want better food, better houses, better education, better healthcare—there is no natural end to desires. - Resources are limited

Land, labour, capital, time, and natural resources are all finite.

This mismatch between unlimited wants and limited resources creates the problem of scarcity.

👉 Economics, therefore, studies how societies deal with this problem.

In simple words, economics asks:

- What should be produced?

- How should it be produced?

- For whom should it be produced?

To answer these questions, economists study how:

- Individuals decide what to consume or save

- Businesses decide what to produce and how

- Governments decide how to allocate public resources

All these decisions revolve around allocating scarce resources such as labour, capital, and natural resources.

Goods

To understand how resources are used, we must first understand goods.

What Are Goods?

Goods are products that are produced and consumed in an economy.

Traditionally, goods were thought of as physical or tangible items, such as → Food, Clothing, Furniture, Vehicles, Machinery

However, in the modern economy, goods can also be intangible, such as → Software, Digital products, Intellectual property, Recorded online courses

Thus, goods may be physical or non-physical, but they must satisfy human wants.

Classification of Goods

1. Consumer Goods vs Capital Goods

Consumer Goods

These are goods directly used for personal consumption by individuals or households.

Examples → Food items, Clothing, Smartphones and televisions, Furniture and household appliances

These goods directly satisfy human wants.

Capital Goods

Capital goods are used to produce other goods or services. They are not meant for direct consumption.

Examples → Machinery and equipment, Tools, Factory buildings, A tractor used in farming, A printing press used to publish books

👉 Key distinction:

Consumer goods satisfy wants directly, while capital goods help in production.

2. Durable Goods vs Non-Durable Goods

This classification is based on lifespan.

Durable Goods

- Used over a long period, usually more than three years

- Examples: cars, refrigerators, furniture, laptops

Non-Durable Goods

- Consumed quickly

- Have a short lifespan

- Examples: food items, beverages, toiletries, stationery

3. Classification Based on Rivalry and Excludability

Before understanding the types, let us define two key terms:

- Rivalry: Does one person’s consumption reduce availability for others?

- Excludability: Can people be prevented from using the good?

Using these two criteria, goods are classified into four types. Let’s discuss them in detail.

Types of Goods Based on Rivalry and Excludability

1. Private Goods

- Rivalrous ✔

- Excludable ✔

These goods:

- Are owned privately

- Are bought and sold in markets

- Can be denied to others

Examples → Clothing, Personal electronics, privately owned vehicles

If you buy a smartphone, only you can use it, and your use prevents others from using it.

2. Public Goods

- Non-rivalrous ✔

- Non-excludable ✔

These goods:

- Are usually provided by the government

- Are available to everyone

- One person’s use does not reduce availability for others

Examples → Street lighting, Roads, Public parks

If a park exists in your area, everyone can enjoy it simultaneously without reducing its benefit to others

3. Common Goods

- Rivalrous ✔

- Non-excludable ✔

These goods:

- Are open for use by all

- But are limited in quantity

- Face the risk of overuse or depletion

Examples → Fisheries, Forests, Grazing lands

If many fishermen catch fish from the same lake, each fish caught reduces availability for others.

4. Club Goods

- Non-rivalrous ✔

- Excludable ✔

These goods:

- Require payment or membership

- Can be accessed only by members

- One person’s consumption does not reduce availability

Examples → Cable television, Private golf courses, Subscription services like Netflix

If you watch a movie on a streaming platform, your viewing does not prevent others from watching it, but only subscribers can access it.

Services

So far, we discussed goods, which are often physical. But a modern economy cannot function on goods alone. This brings us to services.

What Are Services?

Services are intangible—they cannot be touched, stored, or physically held. Instead, they are activities or tasks performed to satisfy human needs and wants.

Examples include → Hair salons, Education, Banking, Healthcare, Transportation, Entertainment

A key feature of services is that they are produced and consumed simultaneously.

- You cannot store a haircut.

- You cannot stockpile a classroom lecture.

- A medical consultation happens in real time.

Unlike goods, services are on-demand and rely heavily on:

- Human skills

- Expertise

- Interaction between provider and consumer

👉 This is why the service sector is often called labour-intensive.

Utility

Now comes a very important psychological concept in economics—utility.

What Is Utility?

Utility refers to the satisfaction or usefulness a person derives from consuming a good or service.

- It is subjective

- It varies from person to person

For example:

- When you are hungry and eat a slice of pizza, the happiness or satisfaction you feel is its utility.

- The same slice may give less utility to someone who is already full.

Economics does not measure utility in exact numbers in real life, but uses it conceptually to understand consumer behaviour.

Marginal Utility: Satisfaction from One More Unit

While utility is total satisfaction, marginal utility focuses on change.

What Is Marginal Utility?

Marginal utility is the additional utility gained from consuming one more unit of a good or service.

Let us understand this clearly with the pizza example:

- First slice (very hungry):

Utility = 10 units - Second slice:

Utility = 8 units

The marginal utility of the second slice is lower than the first. The reduction shows how satisfaction declines as consumption increases.

Law of Diminishing Marginal Utility

This leads us to one of the most fundamental laws of economics.

The Law States:

As a person consumes more and more units of a good or service, the additional satisfaction from each extra unit decreases.

Continuing the example:

- Third slice of pizza:

- You are nearly full

- Utility may drop further, say to 5 units

Thus, with every additional unit, marginal utility diminishes.

Why Is This Law Important?

It explains:

- Why people do not consume unlimited quantities of one good

- Why people seek variety

- Why demand curves generally slope downward

As marginal utility falls, individuals start:

- Looking for alternatives

- Shifting consumption to other goods or services

This law is crucial for understanding consumer choice, demand, and welfare analysis.

Cost: The Producer’s Perspective

So far, we looked at consumption. Now let us shift to production.

What Is Cost?

Cost refers to expenses incurred to produce goods or services.

Costs are broadly classified into:

1. Fixed Costs

Fixed costs do not change with output.

Example:

- Rent of a bakery

- Monthly payment for baking equipment

Whether you produce 10 loaves or 1,000 loaves, these costs remain the same.

2. Variable Costs

Variable costs change with the level of production.

Example → Flour, Sugar, Ingredients used in baking

The more bread you produce, the higher the variable cost.

3. Total Cost

Total cost = Fixed cost + Variable cost

It shows the complete expenditure incurred in production.

4. Average Cost

Average cost is calculated as:

Average Cost = Total Cost ÷ Quantity Produced

It tells us the cost per unit of output, which is crucial for pricing and profitability decisions.

Opportunity Cost: The Cost You Do Not See

Opportunity cost is the value of the next best alternative forgone when a choice is made.

In simple words → Choosing one option automatically means giving up another.

Example:

- If you start a bakery using your skills, the opportunity cost may be:

- The income you could have earned as a chef in a restaurant

👉 Opportunity cost is not always money—it can be time, income, or satisfaction.

Why Is It Important?

Because:

- Resources are scarce

- Every decision involves a trade-off

- Rational decision-making requires comparing benefits and forgone alternatives

Price: The Monetary Expression of Value

What Is Price?

Price is the amount of money or value assigned to a good or service during exchange.

Prices are influenced by:

- Supply and demand

- Cost of production

- Competition

- Government intervention

- Market conditions

Price acts as a signal in the economy, guiding producers and consumers in their decisions.

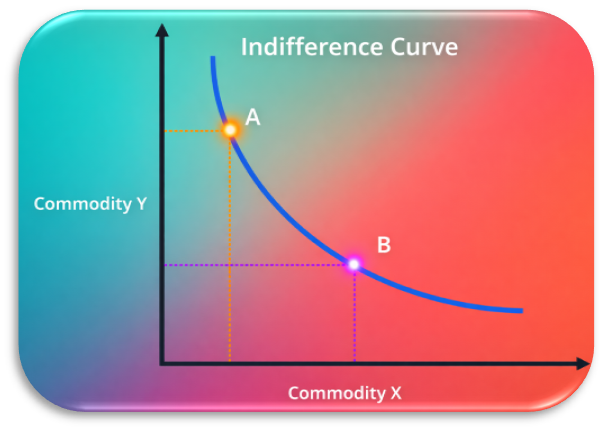

Indifference Curve: Understanding Consumer Choice

Now we move to a slightly analytical but very powerful tool.

What Is an Indifference Curve?

An indifference curve shows different combinations of two goods that give the consumer the same level of satisfaction.

The consumer is indifferent between all points on the curve.

Key Features of an Indifference Curve

- Downward Sloping

To consume more of one good, the consumer must give up some quantity of the other good to remain equally satisfied. - Marginal Rate of Substitution (MRS)

This refers to the rate at which a consumer is willing to substitute one good for another while maintaining the same level of utility. - Diminishing MRS

As consumption of one good increases, the consumer is willing to give up less of the other good.

Why Are Indifference Curves Important?

They help economists:

- Analyse consumer preferences

- Predict consumer choices

- Understand how individuals allocate limited income

- Study utility maximisation under budget constraints