Government Debt in India

Introduction

Government Debt refers to the total outstanding liabilities of the government arising from its past borrowings, undertaken to finance fiscal deficits when government expenditure exceeds its revenue.

In simple terms, whenever the government → Spends more than it earns through taxes and non-tax revenues, it borrows to bridge this gap,

These accumulated borrowings constitute government debt.

Government debt is therefore a stock variable (measured at a point in time), unlike fiscal deficit which is a flow variable (measured over a year).

Why Government Debt Matters

Government debt plays a central role in → Macroeconomic stability, Fiscal sustainability, Growth–inflation trade-off, Inter-generational equity, External sector vulnerability

For UPSC, government debt is critical because it links:

Fiscal deficit → Borrowing → Debt accumulation → Growth, inflation, interest rates, and external stability.

Broad Framework: Classification of Government Debt

Government debt in India is classified along three major dimensions:

- Level of Government

- Source of Borrowing

- Nature of Instrument

This leads to a clear conceptual hierarchy.

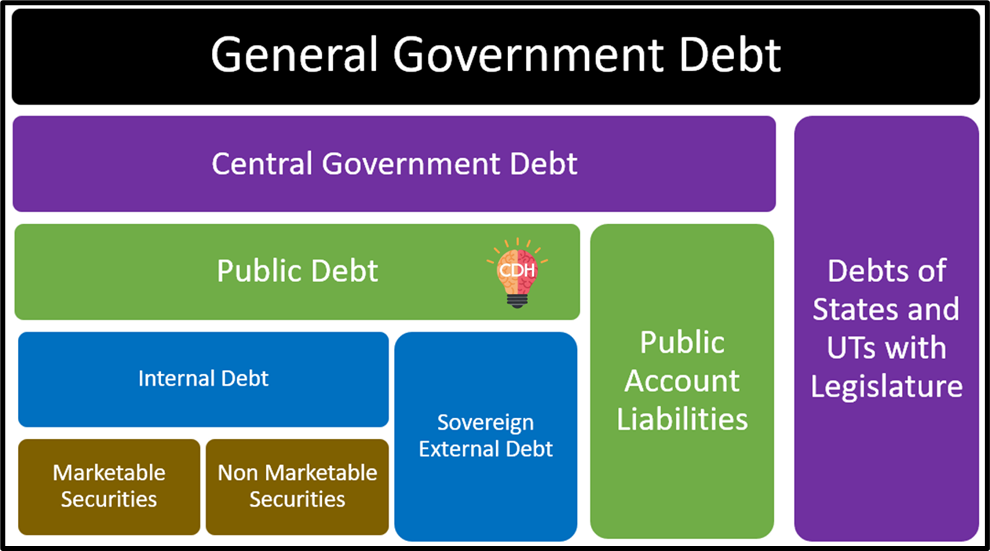

General Government Debt

General Government Debt refers to the total liabilities of the entire government sector, including →Central Government

- State Governments

- Union Territories with legislatures

❌ It excludes inter-governmental liabilities, such as → Loans given by the Centre to States

Importance

- Used by IMF and World Bank for international comparisons

- Reflects overall fiscal health of the country

- Basis for debt-to-GDP ratio

Before examining individual instruments such as government securities, treasury bills, or external borrowings, it is essential to first understand the overall architecture of government debt in India. At the broadest level, General Government Debt represents the total liabilities of both the Central Government and the State Governments/Union Territories with legislature.

Within this framework, Central Government Debt forms the core component and is further divided into Public Debt and Public Account Liabilities. Public Debt reflects funds borrowed by the government to finance its fiscal deficit and is classified into Internal Debt—raised domestically through marketable and non-marketable instruments—and Sovereign External Debt, which represents external borrowings contracted by the Centre. In contrast, Public Account Liabilities consist of obligations arising from schemes such as provident funds and small savings, where the government acts as a custodian of public money.

Parallelly, State Governments and Union Territories with legislature incur their own debt, primarily through domestic borrowings, as they are not constitutionally empowered to contract external debt. This layered classification provides a conceptual roadmap for understanding how different debt instruments fit into the broader fiscal system and helps in analysing issues related to debt sustainability, fiscal responsibility, and macroeconomic stability.

Now, let’s discuss them in detail:

Central Government Debt

This refers to the debt specifically incurred by the Union Government.

Central Government Debt consists of two components:

- Public Debt

- Public Account Liabilities

Public Debt

- Public Debt includes borrowings raised against the Consolidated Fund of India.

- These borrowings are used to finance → Fiscal deficit, Capital expenditure, Revenue shortfalls

- Public Debt is classified based on source of borrowing into:

- Internal Debt

- External Debt

Internal Debt

Internal Debt refers to debt borrowed within the domestic economy from → RBI, Banks and financial institutions, Insurance companies, General public

Internal debt is further classified based on market tradability.

Marketable Securities

These are government debt instruments that can be freely bought and sold in the financial market.

(a) Dated Government Securities (G-Secs)

- Long-term bonds (usually 5 to 40 years)

- Carry fixed or floating interest

- Major source of government borrowing

- Traded in the secondary market

Economic role → Financing capital expenditure, Developing the government securities market, Benchmark for interest rates

(b) Treasury Bills (T-Bills)

- Short-term instruments (less than 1 year)

- Issued for 91, 182, and 364 days

- Zero-coupon securities (issued at discount)

Purpose → Short-term liquidity management, Not meant for long-term financing

(c) Cash Management Bills (CMBs)

- Very short-term instruments

- Maturity less than 91 days

- Issued to manage temporary cash mismatches

Non-Marketable Securities

These instruments cannot be traded in the market and are usually held till maturity.

(a) 14-Day Intermediate Treasury Bills

- Issued to State Governments

- Used for temporary liquidity support

(b) Special Central Government Securities

- Issued to banks, LIC, and financial institutions

- Often used to meet regulatory or statutory requirements

(c) Sovereign Gold Bonds (SGBs) / Gold Monetisation Scheme

- Encourage households to invest in financial gold

- Reduce gold imports

- Help in managing current account deficit

(d) Ways and Means Advances (WMA)

Ways and Means Advances are:

- Short-term advances by RBI to the government

- Meant to bridge temporary mismatches in receipts and payments

📌 Key distinction:

- WMA ≠ deficit financing

- It is temporary and must be repaid quickly

External Debt (Sovereign External Debt)

External debt refers to borrowings from foreign sources.

When such borrowing is done by the government, it is called sovereign external debt.

Components of Sovereign External Debt

(a) Multilateral Loans

- Loans from institutions like → World Bank, IMF, Asian Development Bank

(b) Bilateral Loans

- Loans from foreign governments

- Example: Japan International Cooperation Agency (JICA)

(c) Defence and Civilian Debt

- Borrowings for defence equipment

- Civilian infrastructure projects

(d) Foreign Investment in Government Securities

- Investments by → Foreign Portfolio Investors, Foreign central banks, International institutions

- Considered external because creditor is foreign

(e) Special Drawing Rights (SDR) Allocation

- Reserve asset allocated by IMF

- Creates a liability on the country

Public Account Liabilities

These are liabilities held in trust, not raised to finance expenditure.

Major components → National Small Savings Fund (NSSF), Provident Funds, Post Office Savings

Key Features

- Do not form part of fiscal deficit

- Government is obligated to repay

- Used as an internal source of funds

Debt of State Governments and UTs with Legislatures

State debt includes → Market borrowings, Loans from the central government

📌 Important rule:

- States cannot directly borrow externally

- External borrowing is done only by the Centre

Total External Debt (Economy-wide Concept)

Total External Debt includes all liabilities owed by India to foreign creditors, irrespective of the borrower.

It is divided into:

- Sovereign External Debt

- Non-Sovereign External Debt

Non-Sovereign External Debt

Borrowed by non-government entities.

Components:

- External Commercial Borrowings (ECBs)

Loans taken by Indian companies from abroad - Trade Credits

Credit for imports and exports - NRI Deposits

Deposits by Non-Resident Indians in Indian banks

Debt–to–GDP Ratio?

Think of a country like a household.

- Debt → total loans the household has taken

- GDP → total annual income of the household

Now ask a simple question:

👉 How heavy is the loan burden compared to income?

That’s exactly what Debt–to–GDP Ratio measures.

Debt–to–GDP Ratio= (Total Government Debt / GDP) × 100

If a country has → Debt = ₹100 lakh crore, GDP = ₹200 lakh crore

➡️ Debt–to–GDP = 50%

🧠 Why is this ratio so important?

Because debt by itself is meaningless.

A ₹10 lakh loan is scary for someone earning ₹20,000 a month—but normal for someone earning ₹5 lakh.

Similarly, what matters is not how much a country owes, but how much it earns.

That’s why this ratio is closely watched by:

- Policymakers – to judge fiscal sustainability

- Investors – to assess risk

- Credit rating agencies – to decide a country’s credit rating

In one line → Debt–to–GDP ratio tells us whether a country can comfortably service its debt.

⚠️ What happens when the ratio becomes too high?

A persistently high Debt–to–GDP ratio can trigger multiple problems:

Higher interest burden

More debt → more interest payments → less money for: Education, Health, Infrastructure

Loss of investor confidence

Investors fear → Higher future taxes, Inflation, Possibility of default

Result → capital outflows or higher borrowing costs.

Fiscal rigidity

Government loses flexibility. Even during emergencies, it has little room to spend.

🚨 But is high debt always bad?

Not necessarily.

During extraordinary situations, higher debt is justified →Economic recession, Pandemic (like COVID-19), War or natural disasters

In such times → Borrowing becomes a tool of survival and recovery, not fiscal irresponsibility.

The key is how productively the borrowed money is used and whether the economy grows faster than debt in the long run.

📜 India’s legal benchmark: FRBM targets

To ensure discipline, India adopted clear limits under the Fiscal Responsibility and Budget Management (FRBM) framework.

🎯 Targeted Debt–to–GDP Ratios:

- Central Government → 40% of GDP

- General Government (Centre + States) → 60% of GDP

Why these numbers?

- They are considered safe and sustainable for a growing economy like India.

- They balance growth needs with long-term fiscal stability.

This topic is covered under the Indian Economy notes series designed for UPSC Prelims, Mains, and Interview preparation.