Monetary Policy, Banking & Financial System (Economic Survey 2025–26 Explained)

GLOBAL FINANCIAL MARKETS AND MONETARY DEVELOPMENT

Monetary management and financial intermediation form the backbone of economic stability and growth, with the Reserve Bank of India (RBI) playing a central role in regulating money supply, interest rates, and liquidity.

In a globally interconnected financial system, while globalisation has improved access to capital and reduced borrowing costs, rising geopolitical fragmentation has made financial markets more vulnerable to shocks. Financial markets react quickly to uncertainty, leading to increased volatility, higher risk premiums, and delayed investment decisions. Emerging risks such as AI-driven herding behaviour, inflated asset valuations, and the rise of digital assets like stablecoins further complicate global financial stability.

In this context, India’s monetary policy in FY26 adopted an accommodative yet cautious approach, reducing the repo rate and CRR to boost liquidity, credit flow, and economic activity. Monetary aggregates indicate expansionary conditions, supported by strong growth in bank deposits and credit.

Effective liquidity management ensured surplus liquidity and robust monetary transmission, leading to lower lending rates. Overall, India’s monetary framework demonstrates a balanced approach—supporting growth while maintaining price and financial stability amid global uncertainties.

Key Points

1. Role of Monetary Management

- Monetary policy regulates money supply, interest rates, and liquidity to ensure price stability and growth.

- Effective transmission through banks ensures policy changes impact households and businesses.

- A stable financial system enables efficient resource allocation and economic resilience.

2. Global Financial Interconnectedness

- Globalisation has improved access to capital and reduced borrowing costs.

- Financial systems are now highly interconnected, increasing exposure to global shocks.

- Emerging markets must balance benefits of global finance with risks of volatility.

- Domestic financial development acts as a buffer against external shocks.

3. Financial Markets and Uncertainty

- Financial markets react immediately to uncertainty by adjusting prices and risk perceptions.

- Tariff-related shocks in 2025 led to capital shifts towards safe assets like gold.

- Equity markets declined and risk premiums increased during uncertainty episodes.

- Market stability returned after policy reversals, highlighting sensitivity to policy signals.

4. Channels of Impact of Uncertainty

- Uncertainty delays investment decisions due to “wait-and-see” behaviour.

- It increases cost of finance through higher credit spreads and intermediation costs.

- Prolonged uncertainty may trigger sharp market corrections and financial contagion.

5. Emerging Risks in Global Finance

- AI-driven trading may increase herding behaviour and amplify market volatility.

- Technology stocks show signs of concentration and potential overvaluation.

- Rising global public debt and risk-taking by non-bank institutions add systemic risks.

- Stablecoins are growing rapidly, posing potential spillover risks to traditional finance.

6. Firm-Level Impact of Uncertainty (India Evidence)

- Uncertainty shocks reduce capital formation, with firms cutting investments.

- Mid-sized firms are most affected due to limited flexibility and resources.

- Export-oriented firms are more vulnerable to global shocks.

- Sectoral impact varies, with services and traditional sectors showing resilience.

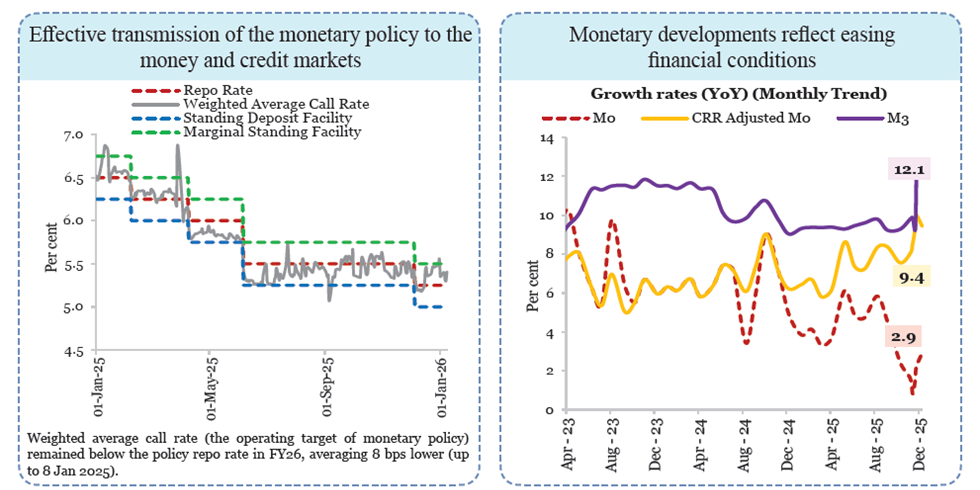

7. Monetary Policy Actions

- RBI reduced repo rate by 100 basis points (Apr–Dec 2025) to 5.25%.

- Policy stance shifted from accommodative to neutral to maintain flexibility.

- CRR reduced by 100 basis points to 3%, releasing liquidity into the system.

- Policy aimed to balance growth support with inflation control.

8. Trends in Monetary Aggregates

- Reserve money (M0) growth declined to 2.9%, but adjusted growth rose to 9.4%.

- Currency in circulation increased significantly, reflecting higher demand.

- Broad money (M3) growth rose to 12.1%, indicating expansionary conditions.

- Growth driven mainly by bank deposits and credit expansion.

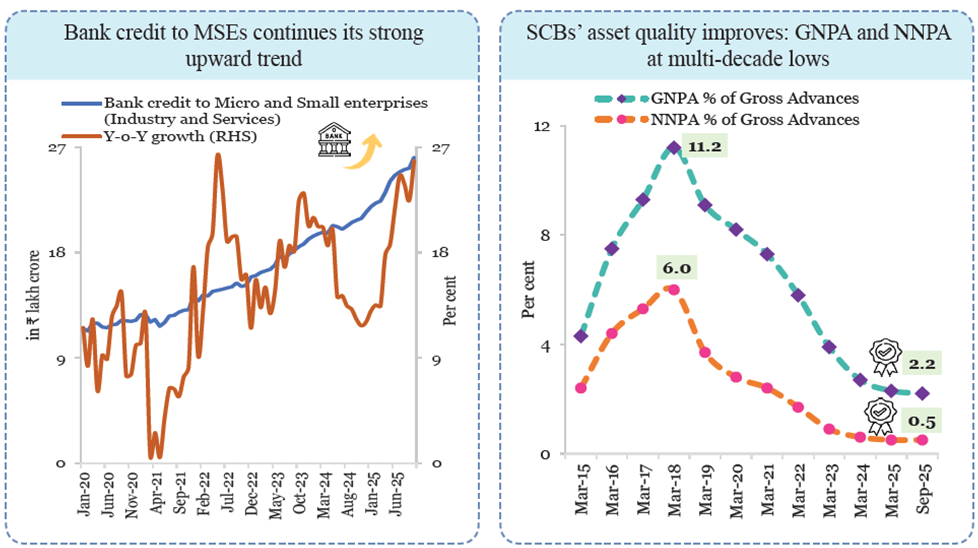

9. Credit and Financial Intermediation

- Bank credit to the commercial sector grew by 14.1% (YoY).

- Deposits grew by 12.3%, supporting money supply expansion.

- Money multiplier increased, indicating improved financial intermediation.

10. Liquidity Management

- RBI injected liquidity through CRR cuts, OMOs, and forex swaps.

- System liquidity remained in surplus (~₹1.89 lakh crore).

- Banks relied less on emergency borrowing and parked more funds with RBI.

- Liquidity conditions supported credit growth and market stability.

11. Monetary Transmission

- Lending rates declined in response to repo rate cuts.

- WALR on fresh loans declined by 64 basis points to 8.71%.

- WALR on outstanding loans declined by 56 basis points.

- Strong transmission reflects effective monetary policy implementation.

Data & Facts

- Repo rate: 5.25% (Dec 2025)

- CRR: 3%

- Liquidity injection: ~₹2.5 lakh crore (CRR cut)

- M3 growth: 12.1%

- Bank credit growth: 14.1% (YoY)

- Deposit growth: 12.3% (YoY)

- Money multiplier: 6.21

- System liquidity surplus: ~₹1.89 lakh crore

- Stablecoin market cap: USD 305.4 billion (+49.6%)

Concepts

- Monetary Policy: Central bank actions to control money supply and interest rates.

- Repo Rate: Rate at which RBI lends money to banks.

- CRR (Cash Reserve Ratio): Portion of bank deposits kept with RBI.

- M0 (Reserve Money): Currency in circulation plus bank reserves with RBI.

- M3 (Broad Money): Total money supply including deposits.

- Money Multiplier: Ratio of total money supply to base money.

- Liquidity: Availability of funds in the financial system.

- Weighted Average Lending Rate (WALR): to measure how effectively monetary policy (like repo rate changes) is transmitted to the real economy.

Analysis

The monetary and financial sector in FY26 reflects a careful balancing act between supporting growth and maintaining stability in a volatile global environment. While global financial markets are increasingly shaped by uncertainty, technological disruption, and geopolitical fragmentation, India’s policy response has remained proactive and calibrated.

The expansionary monetary stance, combined with effective liquidity management, has ensured robust credit flow and strong transmission. However, emerging global risks such as AI-driven volatility and digital financial instruments require continuous regulatory vigilance. The key takeaway is that monetary policy is no longer just about inflation control—it has become central to managing financial stability in an uncertain and interconnected world.

FINANCIAL INTERMEDIATION

India’s financial sector in FY26 reflects strong resilience, improved intermediation, and proactive regulatory oversight amid global uncertainty. The banking sector remains robust, supported by strong balance sheets, declining non-performing assets, and sustained credit growth.

Capital markets have expanded significantly, with increased retail participation and strong equity performance, although concerns of overvaluation persist in certain segments. The debt market has deepened, supported by government securities and corporate bond issuances, improving financing avenues beyond banks.

Foreign portfolio investment flows have remained volatile due to global conditions, highlighting India’s exposure to external financial cycles. Pension and insurance sectors have continued to expand, contributing to long-term financial stability and inclusion.

Regulatory bodies have played a crucial role in maintaining systemic stability through timely interventions, enhanced supervision, and adoption of digital technologies. However, emerging risks such as global financial volatility, technological disruptions, and evolving market structures require continuous vigilance.

Going forward, strengthening financial resilience, deepening markets, and ensuring effective regulation will be critical for sustaining growth and stability in India’s financial ecosystem.

Key Points

1. Banking Sector Performance

- Banks’ balance sheets improved with lower NPAs and higher profitability.

- Credit growth remained strong, supporting economic activity.

- Capital adequacy ratios remained above regulatory requirements.

- Improved asset quality reflects effective regulatory oversight and risk management.

2. Credit Trends and Financial Intermediation

- Bank credit continued to grow across sectors, particularly industry and services.

- Financial intermediation improved, supported by liquidity and policy measures.

- Non-bank financial channels are increasingly complementing bank credit.

- Diversification of financing sources reduces systemic risk.

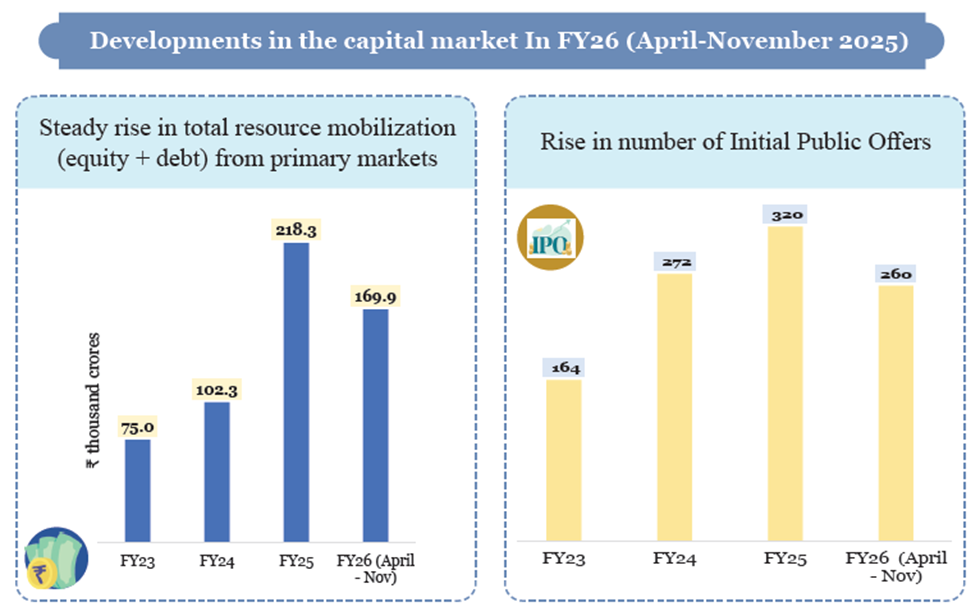

3. Capital Market Developments

- Equity markets witnessed strong participation, including retail investors.

- Market capitalisation expanded significantly, reflecting investor confidence.

- Concerns of overvaluation exist in select sectors, especially technology stocks.

- Capital markets are becoming an important source of corporate financing.

4. Debt Market and Government Securities

- Government securities market remains the backbone of the debt market.

- Corporate bond market is gradually deepening, providing alternative financing.

- Yield movements reflect both domestic and global financial conditions.

- Development of debt markets reduces reliance on bank financing.

5. Foreign Portfolio Investment (FPI)

- FPI flows remained volatile due to global uncertainty and interest rate differentials.

- Capital inflows are sensitive to global monetary policy and risk perceptions.

- India continues to attract long-term investments despite short-term volatility.

- Managing external vulnerability remains a policy priority.

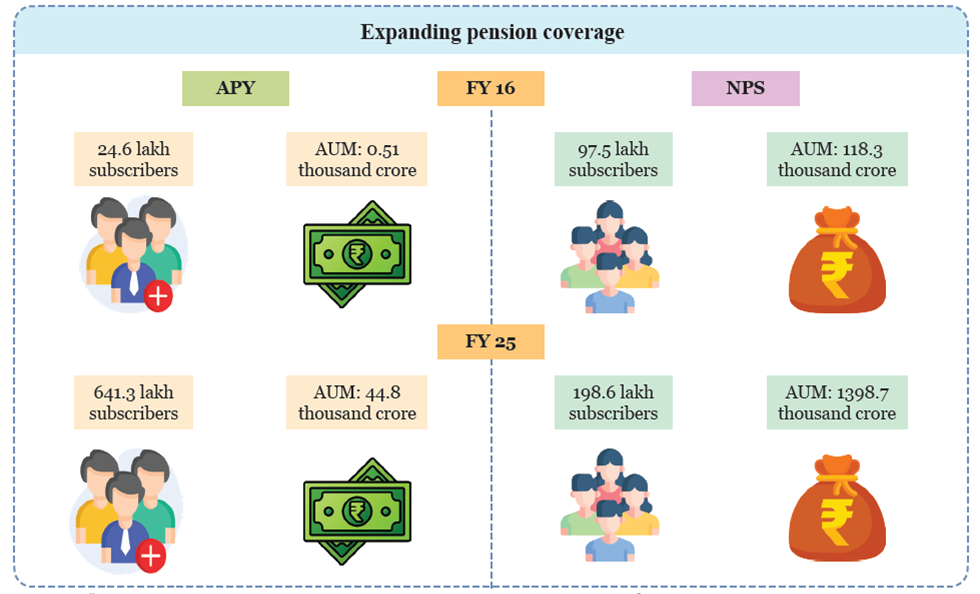

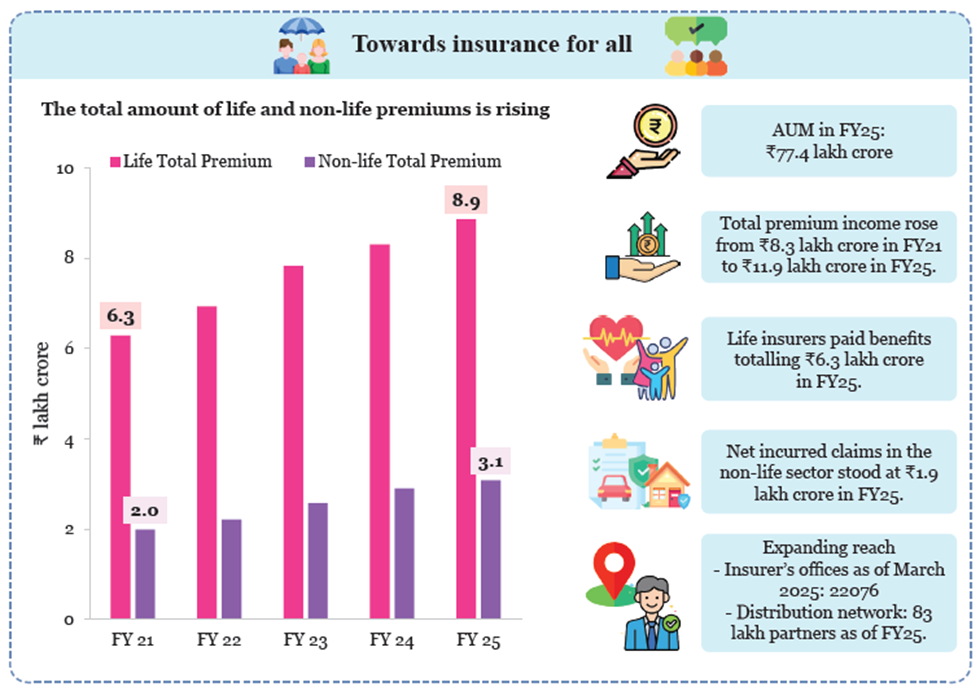

6. Pension and Insurance Sector Growth

- Pension sector assets expanded, enhancing long-term savings mobilisation.

- Insurance penetration improved, supporting financial inclusion.

- These sectors contribute to stable, long-term capital formation.

- Growth reflects rising financial awareness and institutional development.

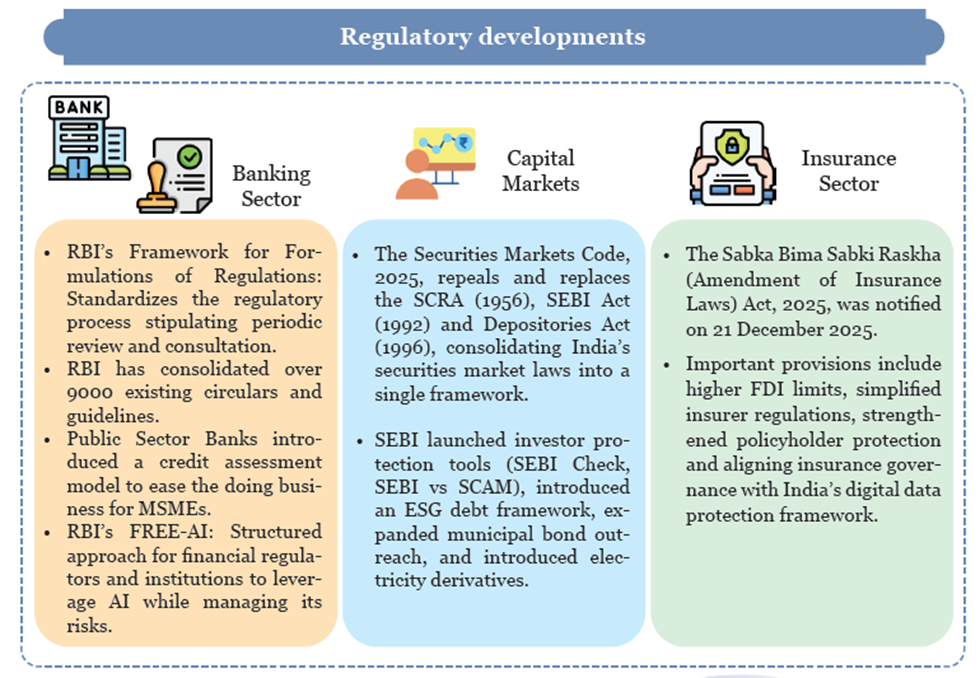

7. Role of Financial Sector Regulators

- Regulators ensured stability through timely interventions and supervision.

- Adoption of digital tools improved monitoring and compliance.

- Regulatory coordination across sectors strengthened systemic resilience.

- Focus remains on balancing innovation with risk management.

8. Emerging Risks and Challenges

- Global financial volatility poses risks to capital flows and markets.

- Technological disruptions, including AI and digital assets, create new risks.

- Market concentration and asset overvaluation require monitoring.

- Non-bank financial institutions may amplify systemic risks.

9. Financial Sector Outlook

- Financial sector expected to remain stable with continued policy support.

- Market deepening and diversification will enhance resilience.

- Strengthening regulatory frameworks is essential for future stability.

- Focus on inclusion and innovation will drive long-term growth.

Data & Facts

- Banking NPAs: At multi-year lows (~2–3%)

- Credit growth: Double-digit growth (~12–14%)

- Capital adequacy: Above regulatory norms

- Equity market participation: Rising retail share

- Pension and insurance assets: Steady expansion

Concepts

- NPA (Non-Performing Asset): Loan where repayment has stopped for a specified period.

- Capital Adequacy Ratio (CAR): Measure of a bank’s financial strength and risk absorption capacity.

- FPI (Foreign Portfolio Investment): Investment in financial assets like stocks and bonds by foreign investors.

- Corporate Bond Market: Market where companies raise funds through debt instruments.

- Financial Intermediation: Process of channeling funds from savers to borrowers.

Analysis

India’s financial sector is undergoing a structural transformation, moving towards greater diversification, digitalisation, and resilience. The banking sector’s improved health and the growing role of capital markets indicate a shift towards a more balanced financial system.

However, global uncertainties and technological disruptions introduce new complexities that require adaptive regulation. The increasing role of non-bank financial institutions and digital assets necessitates stronger oversight to prevent systemic risks. The key challenge ahead lies in sustaining growth while ensuring stability, particularly in an increasingly interconnected and rapidly evolving global financial environment.

One Comment