Bonds

Suppose a government or a company wants to build a highway, expand a factory, or finance a large project. Instead of borrowing from a single bank, it borrows small amounts of money from thousands of investors. The instrument through which this borrowing happens is called a bond.

So, a bond is essentially a debt instrument. When an entity issues a bond, it is borrowing money from investors, and the investors become lenders. In return for this loan, the issuer promises two things:

- Periodic interest payments (called the coupon), and

- Repayment of the principal amount when the bond reaches its maturity date.

For example, if you buy a bond worth ₹10,000 with a 5% interest rate, the issuer will pay you ₹500 every year until the bond matures. At the end of the maturity period, you will receive your ₹10,000 back.

Thus, bonds represent a contractual financial relationship between borrower and lender, and they form an important component of the capital market.

Now let us understand the major types of bonds.

1. Coupon Bonds

A coupon bond is the traditional form of bond where investors receive periodic interest payments, known as coupon payments.

Earlier, these bonds had physical coupons attached, which investors would detach and submit to receive interest. Hence the name coupon bonds.

How it works

Suppose:

- Face value = ₹10,000

- Coupon rate = 5%

- Maturity = 10 years

Every year the investor receives ₹500 as interest

After 10 years, the investor receives:

- Final interest payment

- Principal amount of ₹10,000

Important feature: Price–Interest Rate Relationship

The coupon rate remains fixed, but market interest rates change.

This creates an important economic principle:

- If market interest rates rise, existing bonds become less attractive, so their price falls.

- If market interest rates fall, existing bonds become more attractive, so their price rises.

This inverse relationship is called the Bond Price–Yield Relationship.

This concept is extremely important in financial markets and monetary policy analysis.

2. Government Bonds

Government bonds are issued by governments to raise funds for public expenditure such as → infrastructure, welfare schemes and fiscal deficit financing

Since they are backed by the sovereign authority of the government, they are generally considered low-risk investments.

Examples in India include:

- Sovereign Gold Bond

- Government of India Savings Bonds

These bonds form a major part of the Government Securities (G-Sec) market.

3. Corporate Bonds

Corporate bonds are issued by companies to raise money for → business expansion, infrastructure, working capital and refinancing existing debt

Compared to government bonds:

| Feature | Government Bonds | Corporate Bonds |

|---|---|---|

| Risk | Low | Higher |

| Interest Rate | Lower | Higher |

The higher interest rate compensates investors for the greater risk of default.

Example: Tata Steel issued a 10-year bond with a coupon rate of 8.25% in 2021.

4. Municipal Bonds

Municipal bonds are issued by local governments or municipal corporations to finance urban infrastructure. Funds raised are used for projects like roads, water supply, sewage systems, hospitals and schools

Example: Municipal Corporation of Greater Mumbai issued ₹2000 crore municipal bonds in 2021 for infrastructure development.

Municipal bonds are becoming increasingly important for urban financing in India.

5. Zero Coupon Bonds

Unlike regular bonds, zero coupon bonds do not pay periodic interest. Instead, they are issued at a discount to their face value.

Example

- Face value = ₹1000

- Issue price = ₹800

The investor pays ₹800 today and receives ₹1000 at maturity. The difference (₹200) represents the investor’s return.

Thus, the investor’s gain comes entirely from capital appreciation, not periodic interest.

6. Sovereign Gold Bonds (SGBs)

A Sovereign Gold Bond is a government security linked to gold prices. These bonds are issued by the Reserve Bank of India on behalf of the Government of India.

Key features

- Denominated in grams of gold

- Maturity: 8 years

- Exit option after 5 years

- 2.5% annual interest (paid semi-annually)

- Price linked to gold market value

The gold price is based on data published by the India Bullion and Jewellers Association.

Why SGBs are important

They allow investors to invest in gold without holding physical gold, thus eliminating storage risk, theft risk and purity concerns

At maturity, investors receive the market value of gold, along with the interest earned during the holding period.

7. Green Bonds

A green bond is issued specifically to finance environmentally sustainable projects.

These projects may include renewable energy, wind farms, solar plants, pollution reduction and sustainable infrastructure

Due to growing concerns about climate change, green bonds have become a major instrument in sustainable finance.

Example: financing the construction of a wind energy project.

8. Masala Bonds

Masala bonds are rupee-denominated bonds issued in foreign markets.

Indian companies issue these bonds in global financial centres such as London, Singapore and Hong Kong. The name “Masala” symbolizes their Indian origin.

Important feature

The bond is denominated in Indian rupees, so exchange rate risk falls on the investor, not the issuing company.

Example

An Indian company issues:

- Bonds worth ₹100 crore

- Coupon rate 7%

- Maturity 5 years

Foreign investors purchase these bonds and receive interest in rupees.

This allows Indian firms to raise global capital without bearing currency risk.

9. Social Impact Bonds

A Social Impact Bond (SIB) is a unique financial instrument that links investment returns to social outcomes.

Here the structure is different:

- Private investors fund a social program

- Non-profit organizations implement the program

- Government repays investors only if targets are achieved

Example:

A job training program for homeless individuals.

If employment rates increase by a predetermined target (say 20%), the government repays investors with returns. If the program fails, investors may lose their money.

Thus, financial incentives are aligned with social outcomes.

10. Inflation-Indexed Bonds (IIBs)

One major risk faced by investors is inflation, which reduces the purchasing power of money.

To address this problem, governments issue Inflation-Indexed Bonds (IIBs).

In these bonds:

- Principal value adjusts with inflation

- Interest is calculated on the inflation-adjusted principal

Example

Initial investment = ₹10,000. If inflation in the first year = 3%

Adjusted principal becomes: ₹10,300

If interest rate = 2%, Interest payment = ₹206

Thus, the bond protects investors from inflation erosion.

11. Convertible Bonds

Convertible bonds combine characteristics of both debt and equity. They give the bondholder the option to convert the bond into shares of the company.

Example

- Face value = ₹10,000

- Conversion ratio = 10:1

This means the investor can convert the bond into 10 shares of the company.

Why investors like them

They provide:

- Fixed income through interest payments, and

- Potential equity gains if the company’s share price rises.

If the share price rises significantly, the investor converts the bond and benefits from capital appreciation.

If not, they continue receiving interest payments like a normal bond.

Concluding Insight

From a broader perspective, bonds are one of the most important instruments in the capital market because they perform a crucial economic function:

- They allow governments, corporations, and local bodies to raise long-term capital.

- They provide stable income opportunities to investors.

- They help channel savings into productive investment, which ultimately supports economic growth and development.

Bond Prices

The bond price is simply the amount an investor pays to purchase the bond in the market.

When a bond is first issued, it usually sells at its face value (par value). But after issuance, the bond is traded in the secondary market, where its price may rise or fall depending on economic conditions.

The most important principle governing bond prices is:

Bond prices and interest rates move in opposite directions.

- When interest rates rise → bond prices fall

- When interest rates fall → bond prices rise

This is known as the inverse relationship between bond prices and interest rates.

Example

Suppose a bond has:

- Face value = ₹1000

- Coupon rate = 5%

- Annual interest payment = ₹50

Now imagine that market interest rates increase from 5% to 6%.

New bonds entering the market will now offer ₹60 interest on ₹1000.

Compared to these new bonds, your old bond paying ₹50 looks less attractive.

To sell it, you must reduce its price. For instance, → You may sell the bond for ₹900 instead of ₹1000.

This lower price compensates the new buyer for receiving a lower coupon payment.

Thus, market interest rates determine the market price of existing bonds.

Bond Yield

While bond price tells us how much the bond costs, bond yield tells us how much return the investor earns.

In simple terms:

This means yield changes whenever the bond price changes.

To see this clearly:

Suppose the bond pays ₹50 interest per year.

If the bond price remains ₹1000, the yield is:

Yield = 50/1000 = 5%

But if the bond price falls to ₹900, the same interest payment now produces a higher return.

Yield = 50/900 = 5.56%

So, we observe an important relationship:

- Bond price falls → Yield rises

- Bond price rises → Yield falls

This inverse relationship between bond price and bond yield is fundamental to understanding financial markets and monetary policy transmission.

Factors Affecting Bond Prices

Bond prices are influenced by several macroeconomic and financial factors.

(1) Interest Rates

The most powerful determinant of bond prices is the prevailing interest rate in the economy.

If central banks increase policy rates:

- New bonds offer higher interest rates

- Older bonds become less attractive

- Their market price falls

Conversely, when interest rates fall:

- Existing bonds offering higher coupons become more valuable

- Their price increases

This is why the bond market closely follows decisions of the Reserve Bank of India and other central banks.

(2) Credit Quality

Another important factor is the creditworthiness of the issuer. Bonds are rated by credit rating agencies based on the issuer’s ability to repay debt.

Typical ratings include:

- AAA – Highest safety

- AA / A – High quality

- BBB – Moderate risk

- Below BBB – High risk or speculative

If a company’s financial health deteriorates and its rating is downgraded, investors may fear default risk.

As a result:

- Investors start selling the bond

- Market price falls

Thus, credit risk directly affects bond valuation.

(3) Inflation Expectations

Inflation reduces the purchasing power of money. Since bonds pay fixed interest payments, high inflation reduces the real value of those payments.

Example:

Suppose you bought a bond:

- Price = ₹1000

- Interest = ₹40 annually

- Yield = 4%

Now suppose expected inflation rises to 5%. Investors will demand higher returns to compensate for inflation risk.

To provide that higher return, the bond price must fall.

For instance, → Bond price falls to ₹800

Now → ₹40 interest on ₹800 gives a yield of 5%

Thus, inflation expectations push bond prices downward.

(4) Market Demand

Like any financial asset, bond prices also depend on supply and demand conditions.

If investors strongly prefer a particular bond → Demand rises, Price rises and Yield falls

Example:

Suppose the government issues bonds to finance a sustainable public transport project. If investors trust the government and like the project’s objectives, demand may increase.

- Initial price = ₹1000

- Yield = 5%

If demand increases:

- Price may rise to ₹1100

- Yield falls because investors accept lower returns for safety.

Thus, investor sentiment and market demand also influence bond prices.

The Bond Yield Curve

Now we come to one of the most powerful analytical tools in macroeconomics: the bond yield curve.

The yield curve is a graph that plots:

- Bond yields (interest rates) on the vertical axis

- Bond maturity periods on the horizontal axis

Typically it uses government bonds because they are considered risk-free benchmarks.

The yield curve shows how interest rates differ for short-term and long-term borrowing.

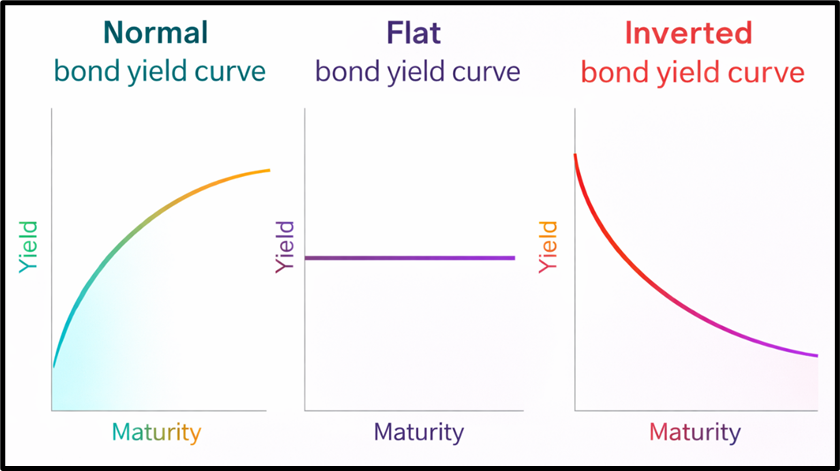

Types of Yield Curves

There are three major shapes of yield curves.

(1) Normal Yield Curve

A normal yield curve slopes upward.

This means → Long-term bonds offer higher yields than short-term bonds.

Example:

- 1-year bond → 5%

- 5-year bond → 6%

- 10-year bond → 7%

What it indicates

A normal curve suggests → Economic growth, Rising demand for credit and Moderate inflation expectations

Investors demand higher returns for locking money for longer periods.

(2) Inverted Yield Curve

An inverted yield curve slopes downward. This means → Short-term interest rates become higher than long-term rates

This unusual pattern typically signals economic pessimism.

Investors expect → economic slowdown and future interest rate cuts by central banks

So, they start buying long-term bonds, pushing their prices up and yields down.

Historically, inverted yield curves have often preceded recessions. For example, the U.S. yield curve inverted briefly in 2019, which many economists interpreted as a warning of an economic slowdown.

(3) Flat Yield Curve

A flat yield curve occurs when short-term and long-term yields are almost equal. This indicates uncertainty about the economic outlook.

Investors are unsure whether → interest rates will rise or fall in the future. Therefore, they do not strongly prefer either short-term or long-term bonds.

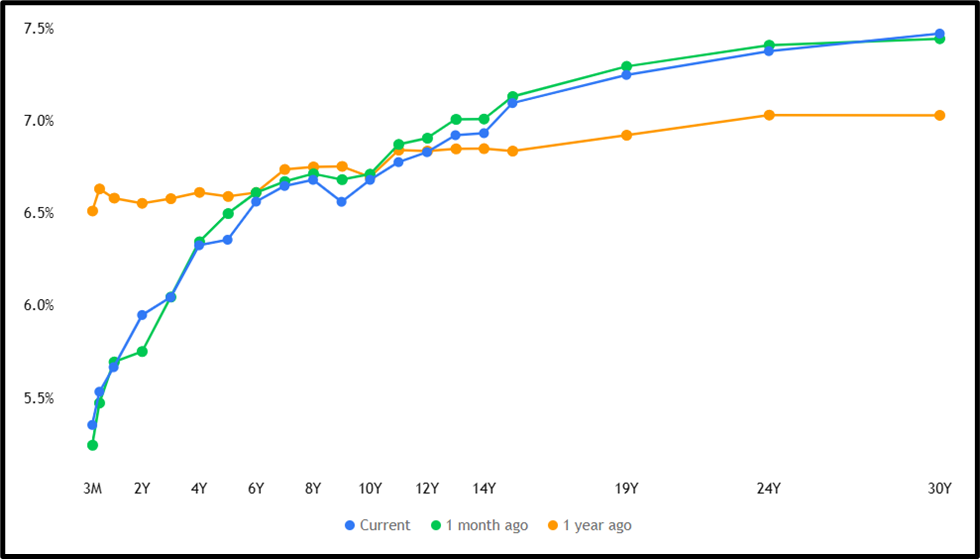

Example

The following chart (as on 13 Mar. 26) illustrates the Government of India bond yield curve across different maturities, comparing three time periods: current yields (blue), yields one month ago (green), and yields one year ago (orange).

The horizontal axis represents bond maturity, ranging from 3 months to 30 years, while the vertical axis shows the yield or interest rate (%) demanded by investors. The curve generally slopes upward from left to right, indicating that long-term bonds offer higher yields than short-term bonds, which is characteristic of a normal yield curve.

This reflects the fact that investors demand higher returns for lending money for longer periods due to greater risks such as inflation and interest-rate uncertainty. A comparison of the three curves shows that short-term yields are lower at present than they were a year ago, while long-term yields have increased slightly, suggesting that the yield curve has steepened over time.

The close proximity of the blue and green curves indicates that bond yields have remained relatively stable over the past month, while the noticeable gap between the current and one-year-ago curves highlights how market expectations about inflation, economic growth, and future interest rates have evolved over the past year.

Why the Yield Curve is Important

The yield curve is not just a financial graph; it is a powerful economic signal.

(1) Economic Indicator

An inverted yield curve has historically predicted recessions in many countries. Economists closely watch it to assess future economic trends.

(2) Borrowing Costs

The yield curve influences → mortgage rates, corporate borrowing costs and government borrowing costs

Thus it affects investment, consumption, and economic growth.

(3) Investment Decisions

Investors use the yield curve to decide whether to invest in short-term bonds or long-term bonds

Portfolio managers, pension funds, and central banks all use yield curve analysis for asset allocation decisions.

Concluding Insight

If we step back and see the broader picture, bond markets perform a crucial role in the economy.

They do not just provide funding to governments and companies; they also act as a barometer of economic expectations.

- Bond prices reflect investor sentiment.

- Bond yields determine returns and borrowing costs.

- The yield curve reveals expectations about growth, inflation, and future interest rates.

That is why economists often say:

If you want to understand where the economy is heading, look carefully at the bond market.