The Budget in Parliament (Article 112)

(“The Mirror of Government’s Policy — Presented Every Year”)

Meaning and Constitutional Basis

The Constitution never uses the word “Budget.”

It calls it the Annual Financial Statement (AFS) under Article 112.

💡 So in prelims, if asked “Which Article deals with the Union Budget?” → answer: Article 112.

📘 Definition:

“The Budget is a statement of the estimated receipts and expenditure of the Government of India for a financial year.”

🗓️ Financial year = 1st April to 31st March.

Contents of the Budget

The Budget isn’t just a list of income and expenses — it’s also a policy document.

It includes:

- Estimates of revenue and capital receipts.

- Ways and means to raise revenue (taxation proposals, borrowings, etc.).

- Estimates of expenditure — revenue + capital.

- Details of actual receipts & expenditure of the previous year, with explanation for surplus/deficit.

- Economic and financial policy for the coming year — including taxation plans, new schemes, and reforms.

🧩 Hence, the Budget is both a financial statement and a policy statement.

Merger of Railway Budget (2017)

Earlier, India had two budgets:

1️⃣ General Budget – all ministries except Railways.

2️⃣ Railway Budget – receipts and expenditure of Ministry of Railways.

📜 Background:

Separated in 1924 (Acworth Committee, 1921) — to make railway finances more business-like and autonomous.

🎯 Reasons for merger in 2017:

- To integrate transport policy and remove duplication.

- To allow Railway profits/losses to be seen in the broader fiscal framework.

- To reduce ritualism and allow unified resource allocation.

Now there is only one Union Budget.

Constitutional Provisions

Here’s a crisp summary of key provisions and their meanings 👇

| Article | Subject | Key Idea |

|---|---|---|

| 112 | Annual Financial Statement | President lays budget before both Houses. |

| 113 | Demands for Grants | Made only on President’s recommendation; voted only by Lok Sabha. |

| 114 | Appropriation Bill | Withdraw money from Consolidated Fund only via law. |

| 115 | Supplementary/ Excess Grants | If more money is needed or overspent during the year, Parliament can approve additional or excess grants. |

| 116 | Vote on Account / Exceptional Grants | Grants made in advance or for special purposes. |

| 117 | Financial Bills | Introduced only on President’s recommendation (esp. taxation). |

| 265 | Taxation Principle | “No tax shall be levied or collected except by authority of law.” |

| 109 | Money Bill Procedure | Can only originate in Lok Sabha; Rajya Sabha has limited powers. |

| 110 | Money Bill | Defines what constitutes a Money Bill (like taxation, borrowing, expenditure). |

Parliamentary Powers & Limitations

Let’s understand the balance between Lok Sabha & Rajya Sabha in financial control.

| Provision | Meaning |

|---|---|

| Only Lok Sabha can vote on Demands for Grants. (Art. 113) | Rajya Sabha can only discuss, not vote. |

| Money Bill / Finance Bill can be introduced only in Lok Sabha, not in Rajya Sabha. (Art. 109, 117) | Rajya Sabha must return within 14 days with or without recommendations. |

| President’s recommendation is compulsory for: introducing a Money/Finance Bill, and for any grant. (Arts. 113, 117) | Ensures executive initiative in financial matters. |

| Parliament may reduce or abolish a tax, but cannot increase it. (Art. 117) | Power is limited to control, not expansion. |

| No money withdrawn from Consolidated Fund of India except by law (Appropriation Act). (Art. 114) | Ensures legislative sanction for spending. |

💡 Takeaway: Budget is executive-initiated but legislature-approved.

Structure Of Expenditure

The Budget distinguishes between two categories of expenditure:

(A) Charged Expenditure — Non-votable but discussable

→ Charged directly on the Consolidated Fund of India (CFI)

→ Parliament cannot vote, only discuss.

(B) Votable Expenditure

→ Must be voted upon by Lok Sabha through Demands for Grants.

Charged Expenditure — (Non-votable list)

The following items are charged on the CFI (Art. 112(3)):

1️⃣ Emoluments & allowances of the President.

2️⃣ Salary & allowances of the Speaker, Deputy Speaker (Lok Sabha) and Chairman, Deputy Chairman (Rajya Sabha).

3️⃣ Salary, allowances & pensions of Supreme Court judges.

4️⃣ Pensions of High Court judges.

5️⃣ Salary, allowances & pensions of the CAG.

6️⃣ Salary, allowances & pensions of UPSC Chairman & Members.

7️⃣ Administrative expenses of SC, CAG, and UPSC (including staff).

8️⃣ Debt charges of the Government of India (interest, sinking fund, redemption, etc.).

9️⃣ Amounts required to satisfy court decrees or arbitration awards.

🔟 Any other expenditure declared by Parliament to be so charged.

💡 Key logic: These offices must remain financially independent of political control.

Revenue Vs Capital Account

Under Article 112, the Budget must distinguish:

| Type | Meaning | Examples |

| Revenue Account | Day-to-day income/expenditure — recurring in nature. | Salaries, pensions, interest payments, tax receipts. |

| Capital Account | Long-term investments or liabilities. | Loans, repayment of debt, creation of assets, disinvestment. |

Key Principles to Remember

| Principle | Article | Meaning |

| Executive initiative in finance | 113 & 117 | No demand for grant or money bill without President’s recommendation. |

| Legislative control over public purse | 114 & 116 | No withdrawal without Appropriation Act; Vote on Account possible. |

| Financial accountability | 112–117 | Ensures transparency and control by elected House. |

| Taxation by authority of law | 265 | No tax can be imposed without legal sanction. |

Enactment Of the Union Budget

(Article 112–117 read with Parliamentary Rules)

6 Stages of Budget Enactment

“The Budget is not passed in one day — it evolves through six constitutionally and procedurally defined stages.”

| Stage | Process | Key Idea |

| 1️⃣ | Presentation of Budget | Laying the ‘Annual Financial Statement’ before Parliament |

| 2️⃣ | General Discussion | Broad debate, no voting |

| 3️⃣ | Scrutiny by Departmental Committees | Detailed, ministry-wise examination |

| 4️⃣ | Voting on Demands for Grants | Lok Sabha’s exclusive power |

| 5️⃣ | Passing of Appropriation Bill | Legalises withdrawals from the Consolidated Fund |

| 6️⃣ | Passing of Finance Bill | Legalises taxes and revenue side |

1️⃣ Presentation of the Budget

📅 When?

- Conventionally: Last working day of February

- Since 2017: Advanced to 1st February

(Purpose → to complete the process before the financial year starts on 1 April, avoiding interim “Vote on Account.”)

🧾 Who presents?

- Finance Minister presents in Lok Sabha (with the famous “Budget Speech”).

- Immediately after, the Budget is laid before Rajya Sabha, which can discuss but not vote on Demands for Grants.

⚙️ Key budget documents include:

| Category | Document |

|---|---|

| (i) | Budget Speech |

| (ii) | Annual Financial Statement |

| (iii) | Demands for Grants |

| (iv) | Finance Bill |

| (v) | FRBM Statements: Macro-Economic Framework, Fiscal Policy Strategy, Medium Term Fiscal Policy |

| (vi) | Expenditure Budget |

| (vii) | Receipts Budget |

| (viii) | Expenditure Profile |

| (ix) | Memorandum on Finance Bill |

| (x) | Budget at a Glance |

| (xi) | Outcome Budget (Output–Outcome Framework) |

| (xii) | Key Features of Budget |

| (xiii) | Implementation of Previous Announcements |

| (xiv) | Key to Budget Documents |

📘 Note:

Earlier, the Economic Survey was presented along with the Budget;

now, it is presented one or a few days before the Budget.

2️⃣ General Discussion

- Begins a few days after presentation (to allow MPs to study documents).

- Occurs in both Houses, usually lasting 3–4 days.

- Focus: overall policy, principles, and general issues, not specific figures.

- No cut motion, no voting.

- Finance Minister replies at the end.

🎯 Purpose: To set the tone and let the government sense the mood of Parliament.

3️⃣ Scrutiny by Departmental Standing Committees

- After general discussion, Houses adjourn for 3–4 weeks.

- During this recess, 24 Departmentally Related Standing Committees (DRSCs) examine Demands for Grants of respective ministries.

- Committees submit detailed reports back to Parliament.

💡 Significance:

Introduced in 1993 (expanded in 2004).

It made financial control specialised, continuous, and expert-based, instead of just political.

4️⃣ Voting on Demands for Grants (Lok Sabha only)

⚖️ Constitutional Base: Article 113

- After committee reports are received, the Lok Sabha considers and votes on each Demand for Grant.

- Each demand corresponds to a ministry/department.

- Once passed, a “demand” becomes a grant.

🗳️ Only the votable portion of expenditure is voted;

the charged expenditure is only discussed, not voted.

✂️ Cut Motions — Tools for Parliamentary Control

Members can move cut motions to reduce a Demand for Grant.

| Type | Purpose | Formula |

|---|---|---|

| Policy Cut | Disapproval of policy | Reduce amount to ₹1 |

| Economy Cut | Suggests economy in expenditure | Reduce by specific amount |

| Token Cut | Ventilates a grievance | Reduce by ₹100 |

Conditions for admissibility:

- Must relate to one demand only, clearly expressed, not defamatory.

- Must be specific, not suggesting amendment of law.

- Must concern Union affairs, not state subjects.

- Cannot relate to charged expenditure, matters in court, or questions of privilege.

Significance:

- Enables focused discussion on departmental spending.

- Reinforces responsible government.

- In practice → symbolic, not successful, because the government enjoys majority.

- If passed → considered no-confidence in government → leads to resignation.

⏰ Guillotine

On the last day allotted for discussion, the Speaker puts all remaining Demands to vote without discussion.

This automatic disposal is called “Guillotine.”

(Purpose: ensures timely passage of Budget.)

5️⃣ Passing of the Appropriation Bill (Article 114)

After demands for grants are passed:

- Appropriation Bill is introduced to authorise withdrawal from the Consolidated Fund of India (CFI) for:

1️⃣ Grants voted by Lok Sabha, and

2️⃣ Expenditure charged on CFI.

No amendment is allowed that alters the amount/destination of any grant or charged expenditure.

Once passed and assented by President → becomes Appropriation Act.

📘 This Act legalises all government expenditure.

Vote on Account (Art. 116)

Since passing the full Budget takes time, Vote on Account allows temporary funds for short period (normally 2 months, about 1/6th of the year’s total expenditure).

In an election year, may cover 3–5 months.

🕓 After 2017, because Budget is presented on 1st February, Parliament can usually pass the Appropriation Bill before 31 March,

so Vote on Account is required only in election years when an Interim Budget is presented.

Interim Budget vs Vote on Account

| Feature | Interim Budget | Vote on Account |

|---|---|---|

| Meaning | Complete estimates of expenditure and receipts during election year | Temporary grant to carry on till full Budget is passed |

| Covers | Full year (estimates) | Usually 2–4 months |

| Voting | On Demands for Grants | On advance sum only |

| Presented by | Outgoing government | Current government (routine) |

6️⃣ Passing of the Finance Bill

📜 Meaning:

- The Finance Bill gives legal effect to the taxation proposals and revenue side of the Budget.

- It is governed by Article 110 (Money Bill).

⚙️ Key Features:

- Introduced along with the Budget.

- Amendments allowed to reduce or reject a tax proposal.

- Must be enacted within 75 days (Provisional Collection of Taxes Act, 1931).

- Once passed → becomes Finance Act.

- This completes the process of Budget enactment —

expenditure side via Appropriation Act, income side via Finance Act.

💬 Insightful Lines:

“The Budget process reflects the essence of democracy —

the Executive proposes, but the Legislature disposes.

Through cut motions, guillotine, appropriation and finance bills,

the Lok Sabha asserts that no rupee leaves or enters the public purse without the people’s sanction.”

Quick Revision Snapshot

| Stage | Instrument | Authority | Key Point |

|---|---|---|---|

| 1️⃣ Presentation | Budget Speech | Finance Minister | 1 Feb, President’s recommendation |

| 2️⃣ Discussion | General Discussion | Both Houses | No voting |

| 3️⃣ Scrutiny | Standing Committees | 24 DRSCs | Detailed study of Demands for Grants |

| 4️⃣ Voting | Cut Motions, Guillotine | Lok Sabha only | Exclusive power to grant or refuse funds |

| 5️⃣ Expenditure Legalisation | Appropriation Bill | Lok Sabha → President | Withdrawals from CFI authorised |

| 6️⃣ Revenue Legalisation | Finance Bill | Lok Sabha → President | Taxation proposals made law |

Other Grants

“The Budget is for the ordinary year; but life is never ordinary.

That’s why the Constitution provides for extraordinary grants and funds.”

Other Grants — Beyond the Regular Budget

When expenditure goes beyond what was planned or when new demands arise mid-year, Parliament can authorise special grants.

| Type | When Required | Key Idea | Passed By |

|---|---|---|---|

| Supplementary Grant | When sanctioned amount proves insufficient during the same financial year | To cover extra spending under an existing head | Lok Sabha |

| Additional Grant | For new service or scheme not in the original budget | To fund unforeseen/new activity | Lok Sabha |

| Excess Grant | When expenditure exceeds the sanctioned amount | Voted after the year ends; must first be vetted by the Public Accounts Committee (PAC) | Lok Sabha |

| Vote of Credit | For unforeseen large or indefinite expenditure (e.g., war, natural calamity) | Like giving a blank cheque to the Executive | Lok Sabha |

| Exceptional Grant | For a specific, one-time purpose not part of current service | Granted separately | Lok Sabha |

| Token Grant | When funds can be met by re-appropriation within existing allocations | Only ₹1 or ₹100 token shown; allows shifting of funds | Lok Sabha |

🧩 Note:

All these follow the same procedure as the regular budget — laid before Lok Sabha, voted, and then included in an Appropriation Act.

Understanding Re-appropriation

“Re-appropriation” = transfer of funds from one head to another without increasing total expenditure.

Example — If the Defence Ministry saves ₹50 crore under “procurement of uniforms,” it can re-allocate the same to “medical supplies.”

✅ Used with Token Grant when new service needs symbolic approval.

Funds of the Central Government

(Articles 266–267)

The Constitution creates three separate funds — each with distinct constitutional status, control mechanism, and operational rule.

| Fund | Article | Nature | Control / Withdrawal Authority |

|---|---|---|---|

| Consolidated Fund of India (CFI) | Art. 266(1) | Main account of the Central Govt — all revenues, loan receipts, and repayments go here. | Withdrawals only by law of Parliament (Appropriation Act) |

| Public Account of India | Art. 266(2) | For money that doesn’t belong to Govt — PFs, judicial deposits, remittances, etc. | Operated by Executive action; no Parliamentary vote required |

| Contingency Fund of India | Art. 267(1) | Emergency fund for unforeseen expenditure | At President’s disposal, operated by Finance Secretary; later replenished by Parliament |

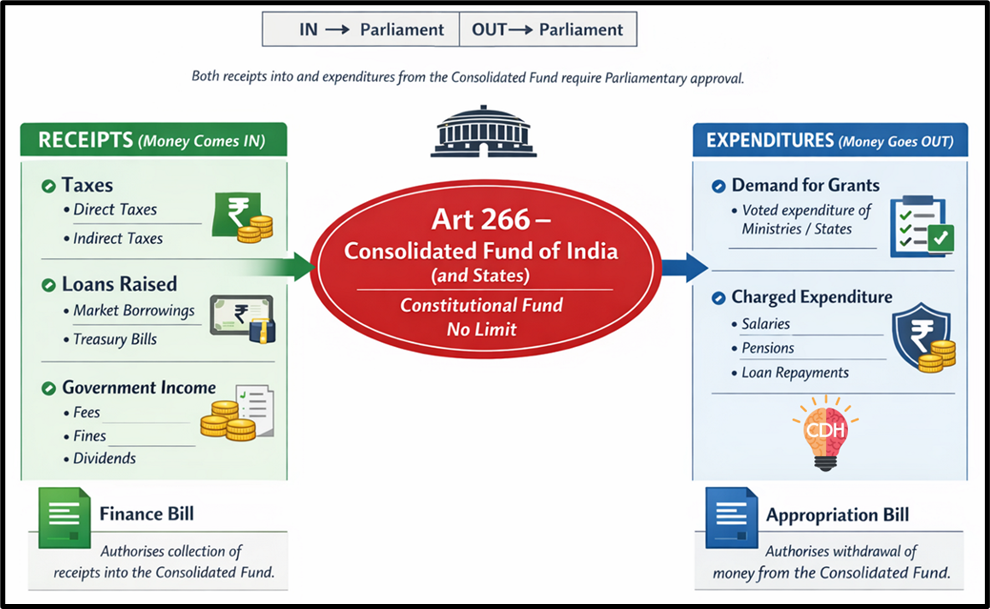

📘 Consolidated Fund of India (CFI)

It’s the main treasury of the Union Government.

💰 Credits

- All revenues (tax & non-tax).

- All borrowings (treasury bills, loans, etc.).

- All repayments of loans to Government.

🏦 Debits

- All legally authorised expenditures, both votable and charged.

⚖️ No withdrawal without Appropriation Act.

This ensures Parliamentary control over the purse — a fundamental feature of responsible government.

So, a vote of parliament is required for any expenditure made from the CFI, except for expenditure that is ‘charged’ on the CFI, which is non-votable. The CFI is used for two types of expenditure:

- Expenditure ‘charged’ on the CFI

This refers to those expenses that are required to be made by law, such as the salary of the President, judges of the Supreme Court and High Courts, and other expenses relating to the constitutional provisions. - Expenditure ‘made’ from the CFI

This refers to those expenses that are approved by parliament every year in the form of the Union Budget.

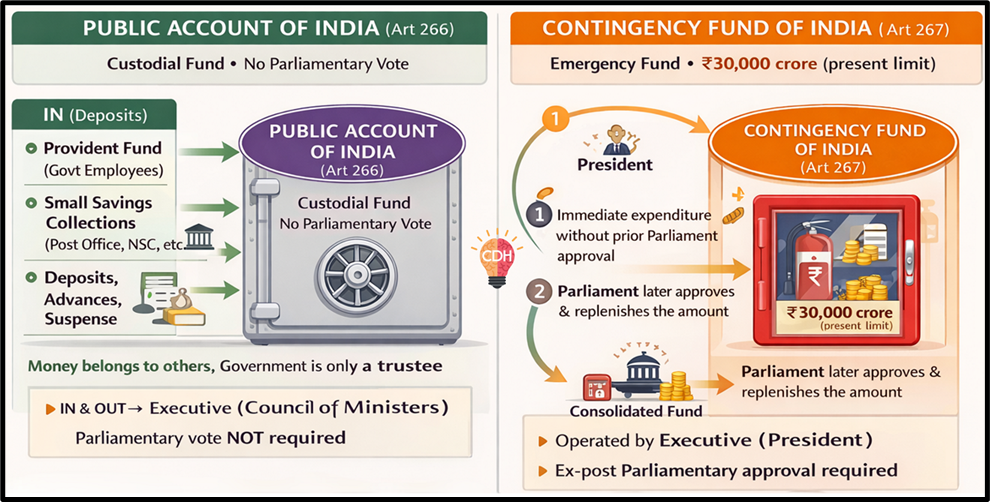

📘 Public Account of India

This account keeps other public money held by Government in trust.

Examples 👇

- Provident Fund deposits (e.g., GPF, NPS).

- Postal savings deposits.

- Judicial & departmental deposits.

- Remittances and suspense accounts.

🧩 Key Point → No Parliamentary appropriation needed because this money belongs to others, not the Government.

Withdrawals are made by executive authority (Ministry of Finance, CAG oversight).

📘 Contingency Fund of India

Created under Article 267(1) → implemented by Contingency Fund of India Act (1950).

⚙️ Features:

- Fund kept at President’s disposal.

- Held and operated by Finance Secretary on behalf of President.

- Used to meet unforeseen expenditure pending Parliamentary approval.

- Amount withdrawn is later recouped from the CFI once Parliament passes the supplementary grant.

- No vote of parliament is required for any expenditure made from the Contingency Fund of India, and the maximum amount that can be kept in this fund is INR 30,000 crore. The amount spent from this fund is later replenished by the approval of the Parliament.

🔹 Similar Funds in States → Contingency Fund of the State (Art. 267(2)) at the Governor’s disposal.

Comparative Snapshot — Three Central Funds

| Feature | Consolidated Fund | Public Account | Contingency Fund |

|---|---|---|---|

| Constitutional Basis | Art. 266(1) | Art. 266(2) | Art. 267(1) |

| Ownership of Money | Government of India | Public / Trust Money | Government (for emergencies) |

| Control | Parliament | Executive | President |

| Withdrawal Condition | Only after Appropriation Act | No Parliament vote | Executive advance, later regularised |

| Examples | Tax revenue, borrowings | PF, postal deposits | Disaster relief, war expenses |

| Audit | CAG | CAG | CAG |

💬 Closing Thought

“These funds reflect three faces of governance:

– The Consolidated Fund shows democracy’s discipline,

– The Public Account shows government’s trusteeship,

– The Contingency Fund shows administration’s agility.

Together they ensure that every rupee of India is handled with legality, accountability and flexibility.”