Utilisation of Public Funds

Imagine the government of India allocates ₹55,000 crore for secondary education over five years. At the end of that period, only ₹17,723 crore — just 32% — is actually spent. The rest? Surrendered, lapsed, or sitting unspent in accounts.

Meanwhile, millions of children remain in crumbling schools with absent teachers and no textbooks. This is the tragedy of public fund utilisation in India — and it is the subject of this section

The question is not just HOW MUCH money the government spends — it is WHAT that money achieves. Public fund utilisation is not a finance topic; it is an ethics topic.

Every rupee of public money is a rupee taken from the taxpayer. Wasting it, misrouting it, or failing to spend it on the poor who need it most — is a moral failure, not just an administrative one.

| 🏛️ 5 Dimensions of Public Fund Utilisation |

| ① EFFICIENCY — Are funds being used optimally? Is there value for money? ② MANNER — Are procedures, rules and accounting norms being followed? ③ OUTPUTS & OUTCOMES — Are physical targets met? Are ultimate objectives achieved? ④ SOURCE — Budget (legislative approval) is the only valid source; no unauthorised expenditure ⑤ AUDIT — All expenditure must be audited by CAG for regularity, propriety and performance PLUS: No waste or fraud; officers must follow Canons of Financial Propriety |

Budget: The Foundation of Public Expenditure

Before a government spends a single rupee, it needs permission from Parliament. This is the bedrock principle of democratic governance — no expenditure without legislative sanction. This permission comes through the Budget.

Article 112 of the Constitution mandates that the Annual Financial Statement (the Budget) be laid before Parliament every year. The Lok Sabha then passes an Appropriation Act, which formally authorises the government to withdraw money from the Consolidated Fund of India.

How Do Ministries Spend Money?

Ministries and departments spend money in two ways:

- Directly (departmentally) — spending from their own offices, such as salaries, office expenses.

- By transferring funds — sending money to implementing agencies such as State Governments, Urban Local Bodies (ULBs), Panchayati Raj Institutions (PRIs), registered societies, and NGOs. These agencies are called ‘Transferee Agencies.’

A Major Reform: Abolition of Plan/Non-Plan Distinction

For decades, India’s budget was divided into ‘Plan’ expenditure (spending linked to Five Year Plans) and ‘Non-Plan’ expenditure (routine spending like salaries). This division was confusing, artificial, and often misleading. For example, building a school was ‘Plan’, but paying teachers’ salaries was ‘Non-Plan’ — even though both are essential for education!

Following the recommendation of the C. Rangarajan Committee, this distinction was abolished from the Union Budget 2017-18 onwards. Now, all government expenditure is classified into just two clear categories:

| Capital Expenditure | Revenue Expenditure |

| Creation or acquisition of assets (buildings, infrastructure), equity, loans | Current / recurring expenditure: salaries, subsidies, maintenance, pensions |

| Example: Building a new highway | Example: Paying highway maintenance workers |

| ✅ This is a far more transparent and meaningful classification. It tells us whether the government is investing for the future (capital) or spending on daily operations (revenue). |

Union Budget 2026-27 at a Glance

Data Source: Union Budget 2026-27 – CDH IAS

| Expenditure Category | Amount (BE 2026-27) |

| Total Expenditure | ₹ 53.5 lakh crore |

| Capital Expenditure | ₹ 12.2 lakh crore (~2.9% of GDP) |

| Revenue Expenditure | ₹ 41.3 lakh crore (approx.) |

| Fiscal Deficit (BE) | 4.3% of GDP |

| Centre’s Net Tax Receipts | ₹ 28.7 lakh crore |

Fund Utilisation — From Spending to Impact

Three Levels of Evaluation

How do we judge whether public money is being used well? There are three progressive levels of evaluation:

| Level | Parameter | Explanation |

| 1 | Financial Target (Expenditure) | Was all the money spent? (Necessary but NOT sufficient) |

| 2 | Output | Were the physical deliverables achieved? (Roads built, schools constructed) |

| 3 | Outcome (Most Important) | Did it change people’s lives? (Did children learn better? Did maternal deaths fall?) |

| 💡Analogy: Imagine a government spends ₹100 crore on mid-day meals. Level 1 asks: Was ₹100 crore spent? Level 2 asks: Were meals served to children? Level 3 asks: Did children’s nutrition improve and school attendance increase? Only Level 3 tells us whether the money truly worked. |

Funds Lapse on 31st March

In India, government funds generally lapse at the end of the financial year on 31st March. Unutilised funds must be surrendered to the finance department around 15th March. This creates a perverse incentive — agencies rush to spend whatever is left in the last few weeks of the year, often recklessly.

This ‘March Rush’ is a well-known governance problem.

Output-Outcome Monitoring Framework

Introduced from 2017-18 onwards, the Output-Outcome Monitoring Framework is now a mandatory companion document to every Union Budget. Every Ministry must define measurable outcomes for all schemes they implement.

The Outcome Budget 2026-27 lists specific, time-bound targets for every major scheme — so accountability is built in from day one.

Fund Utilisation in the Social Sector

India’s social sector covers education, health, water supply, sanitation, social security, and nutrition. These are the sectors that directly touch the lives of common people — especially the poor and vulnerable.

Key Statistics — Social Sector Spending

| Social Sector Indicator | Data / Status |

| Combined Social Service Expenditure (2023-24) | 7.8% of GDP |

| Education Expenditure (Centre + States, BE 2024-25) | ₹ 9.2 lakh crore (CAGR 12%) |

| Health Expenditure as % of GDP (FY24) | 1.9% |

| Govt Share in Total Health Expenditure (FY22) | 48% (up from 29% in FY15) |

| Govt Social Service Exp. as % of Total Expenditure (FY25 BE) | 26.2% |

| MGNREGA Allocation (2025-26 BE) | ₹ 86,000 crore (highest-ever at BE stage) |

| MGNREGA Person-days (2024-25) | 290.60 crore; 15.99 crore households |

Centrally Sponsored Schemes (CSS) — Evolution and Rationalisation

Centrally Sponsored Schemes are one of the most important instruments through which the Central Government channels funds to States for national priority programmes. Understanding their classification and rationalisation is crucial for UPSC.

Classification of Government Schemes

| Type | Funding | How it Works |

| Central Sector Schemes (CS) | 100% Centre | Formulated, funded & implemented entirely by the Central Government through its own agencies. |

| Centrally Sponsored Schemes (CSS) | Shared: 60:40 (General States); 90:10 (NE/Hilly States) | Designed by Centre + States. States share funding and are responsible for implementation on the ground. |

| State Schemes | 100% State | Fully formulated, funded, and implemented by the respective State Government. |

CSS Sub-Classification (Post-2016 Rationalisation)

A major rationalisation exercise was undertaken in 2016 on the recommendation of a Sub-Group of Chief Ministers under NITI Aayog, reducing over 130 CSSs to a leaner structure under three tiers:

- Core of the Core Schemes: Highest national priority. Addresses social protection and social inclusion (e.g., MGNREGS, PM Awas Yojana, National Social Assistance Programme). These have the FIRST CHARGE on available funds — meaning they are funded before anything else.

- Core Schemes: Key national development agenda requiring Centre-State cooperation (e.g., National Health Mission, PM Gram Sadak Yojana, Jal Jeevan Mission).

- Optional Schemes: States may choose to implement or not. Funds released as a lump sum by the Ministry of Finance, giving States greater flexibility.

| 📊 As of 2026: 54 Centrally Sponsored Schemes + 260 Central Sector Schemes. Government of India initiated a 5-yearly appraisal cycle in 2025. New five-year cycle begins April 2026. |

Constraints on Fund Utilisation — Why Money Doesn’t Always Reach People

India has significantly increased social sector allocations over the years. But allocation ≠ utilisation. Money sitting in government accounts is not the same as children getting meals, roads getting built, or wells getting dug. Several structural and procedural constraints prevent full and efficient fund utilisation.

Structural and Procedural Constraints

| Constraint | Explanation |

| Delayed Financial Sanctions | Approvals for new and continuing schemes are frequently delayed. Even after approval, agencies must follow procurement rules (tenders, GeM), consuming more time. |

| Inadequate Delegation of Powers | Many implementing agencies lack delegated financial powers beyond certain thresholds, forcing them to seek approvals from higher authorities — causing unnecessary delays. |

| Outdated Unit-Cost Norms | Schemes are funded on fixed unit costs (per head, per unit). In an inflationary environment, these norms quickly become inadequate. Example: PM-POSHAN (Mid-Day Meal) faces recurring challenges due to rising food costs. |

| Staff Shortages | Social sector schemes suffer from acute shortages of trained staff at district and sub-district levels. States constrained by fiscal deficit targets reduced staff recruitment over years, weakening implementation capacity. |

| Weak PRI Capacity | Despite the 73rd Constitutional Amendment transferring several functions to PRIs, many Panchayati Raj Institutions — especially in poorer States — lack the managerial and financial capacity to plan and implement programmes. |

| Centre-State Rigidities | Central Ministries historically formulated schemes with an identical all-India pattern, leaving little flexibility for States to adapt to regional conditions. Flexi-fund provisions (post-2015) partially address this. |

Transfer of Funds — From Treasury to the Last Mile

Even after allocating funds and sanctioning schemes, the government faces the challenge of actually transferring money from Delhi to a beneficiary in a remote village in Odisha or Rajasthan. This is where the architecture of fund transfer becomes critical.

Treasury Mode vs. Society Mode

| Treasury Mode | Society Mode |

| Funds flow through RBI → State Treasury → Departments. Reflected in Accountant-General records. More transparent and auditable. | Central Ministries directly release funds to district-level implementing agencies/societies. Faster but harder to track, audit, and monitor. |

A key reform: District Rural Development Agencies (DRDAs) were abolished in 2013. Their functions were merged with Zila Panchayats, aligning rural development funds directly with elected local government bodies — a move that strengthened democratic decentralisation.

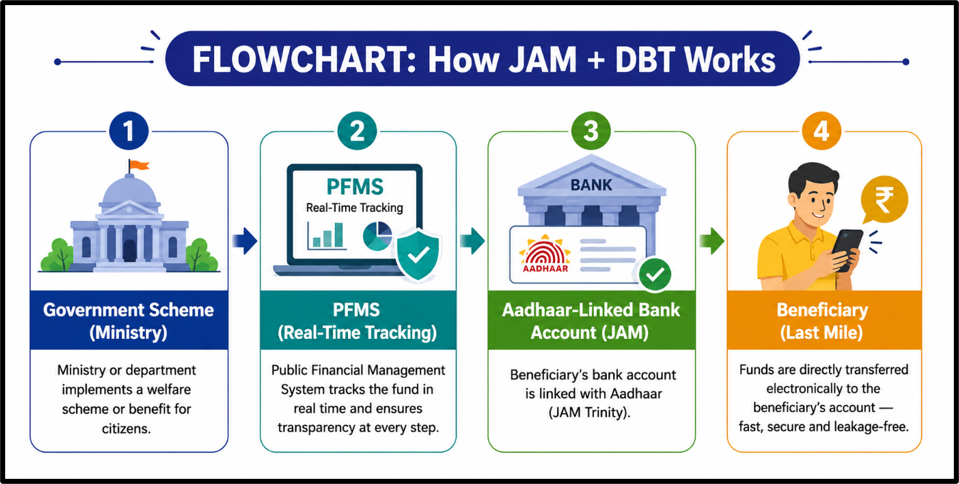

PFMS — Public Financial Management System

The Central Plan Scheme Monitoring System (CPSMS) has been upgraded and rebranded as the Public Financial Management System (PFMS), now under the Controller General of Accounts (CGA). PFMS is India’s centralised government financial information system — the digital nervous system of public spending.

| PFMS provides real-time fund tracking from the initial Central release all the way down to the last-mile implementing agency. It integrates with State treasuries and Accountant General offices, enabling transparency at every stage. |

The JAM Trinity — A Revolution in Fund Transfer

JAM stands for Jan Dhan bank accounts + Aadhaar unique identification + Mobile connectivity. This trinity has fundamentally transformed the architecture of public fund utilisation in India. By linking beneficiary accounts to Aadhaar and enabling direct electronic transfers, JAM has dramatically reduced leakages and eliminated ghost beneficiaries.

| 💡 Historical Contrast: A 2005 Planning Commission estimate suggested it cost the government ₹3.65 to transfer ₹1 worth of food — implying ~70% leakage. DBT has reduced this drastically, though challenges of last-mile connectivity and Aadhaar exclusion errors remain. |

Government e-Marketplace (GeM) — Procurement Reform

Every year, the government buys enormous quantities of goods and services — furniture, computers, vehicles, construction materials, consulting services. Traditionally, this procurement was plagued by corruption, cartelisation, and lack of transparency. GeM was launched in 2016 to fix this.

GeM is a dedicated national public procurement portal that enables government ministries, departments, PSUs, and autonomous bodies to procure goods and services in a transparent, competitive, and efficient manner.

It acts as an Amazon for the government — but with the guarantee of fair pricing and audit trails.

| GeM ensures competitive bidding, standardised product specifications, price transparency, and audit trail — thereby upholding the Canons of Financial Propriety in government procurement. It is integrated with PFMS for seamless payment processing. |

Fiscal Devolution and Intergovernmental Transfers

India is a Union of States. The Central Government collects most taxes, but States are responsible for most development spending (health, education, agriculture). How should tax revenues be shared between the Centre and States? This is the domain of Fiscal Federalism, and the Finance Commission is its arbiter.

Finance Commission — The Constitutional Authority

Article 280 of the Constitution establishes the Finance Commission. It determines the formula for sharing Central tax revenues (the ‘divisible pool’) between the Union and the States.

The 16th FC retains states’ tax share at 41% and shifts fiscal transfers toward performance- and compliance-based criteria, including a new weight for contribution to GDP.

Read about the 16th Finance Commission Report here.

Persistent Problems in Fund Releases and Utilisation

Despite all these systemic reforms — PFMS, DBT, JAM, GeM — some recurring problems continue to plague the system. These have been documented by CAG audit reports, Parliamentary Committees, and independent researchers.

| Problem | Impact |

| Mechanical Fund Releases | Central Ministries release funds without considering absorption capacity of States, leading to parking of large unspent balances in implementing agency accounts. |

| Last-Quarter Rush (March Rush) | A large proportion of scheme funds is released in January-March, making it impossible to spend productively before 31st March. Results in wasteful or hurried spending. |

| Over-Reporting of Expenditure | CAG and PFMS data reveal discrepancies between expenditure reported by agencies and actual verified expenditure. Over-statement of physical and financial performance is a persistent concern. |

| Weak Internal Audit | Internal audit functions in many implementing societies remain inadequate or largely non-functional. The focus on expenditure booking over actual delivery persists. |

| Intra-Scheme Fund Diversion | Funds earmarked for specific scheme components are sometimes diverted to meet other expenditures, distorting programme implementation. |

| Beneficiary Account Issues (DBT Exclusion Errors) | Despite JAM, elderly, disabled, and tribal populations face barriers to Aadhaar linkage and bank account maintenance, creating exclusion errors in DBT delivery. |

| Institutional Response: NITI Aayog’s Development Monitoring and Evaluation Office (DMEO) conducts third-party evaluations of major Central schemes. The Aspirational Districts Programme (ADP, 2018) and Aspirational Blocks Programme focus data-driven attention on India’s most lagging regions. |

Audit of Expenditure — The CAG: Guardian of Public Money

Once money is spent, how do we check whether it was spent correctly? This is the function of audit — specifically, the constitutional audit conducted by the Comptroller and Auditor General (CAG) of India.

The CAG derives authority from Articles 149-151 of the Constitution and the CAG (Duties, Powers and Conditions of Service) Act, 1971. CAG is the head of the Supreme Audit Institution (SAI) of India — the nation’s most powerful financial watchdog.

Who Does the CAG Audit?

- All Union and State Government departments and offices (including Indian Railways)

- ~1,500 government companies under the Companies Act, 2013

- Autonomous bodies substantially funded by the government (universities, research institutes)

- Local bodies and Panchayati Raj Institutions (where mandated)

Three Types of CAG Audit

| Type of Audit | What It Checks | Key Question |

| Regularity Audit (Compliance Audit) | Was expenditure authorised? Did it conform to laws and rules? Was sanction given by the competent authority? | Was the money spent LEGALLY? |

| Propriety Audit (Sub-type of Compliance) | Goes beyond procedural compliance — examines whether expenditure was PRUDENT and WISE, not just legal. | Was the money spent WISELY? |

| Performance Audit | Were programme objectives achieved at lowest cost with intended benefits? The Three E’s: Economy, Efficiency, Effectiveness. | Was the money spent EFFECTIVELY for the intended purpose? |

| Certification of Finance & Appropriation Accounts | CAG certifies Finance Accounts (receipts, disbursements, assets, liabilities) and Appropriation Accounts (actual vs. authorised expenditure). | Was expenditure WITHIN the amounts authorised by Parliament? |

The Three E’s of Performance Audit

| E | Concept | Simple Explanation |

| Economy | Minimising input costs | Did we buy the same quality goods at the least cost? Getting value for money spent. |

| Efficiency | Maximising output per input | Did we get maximum output (roads built, beds created) from the resources deployed? |

| Effectiveness | Achieving intended impact | Did the programme actually achieve its goal? Were intended beneficiaries actually benefited? |

Read in detail about CAG here: Comptroller and Auditor General of India (CAG) – CDH IAS

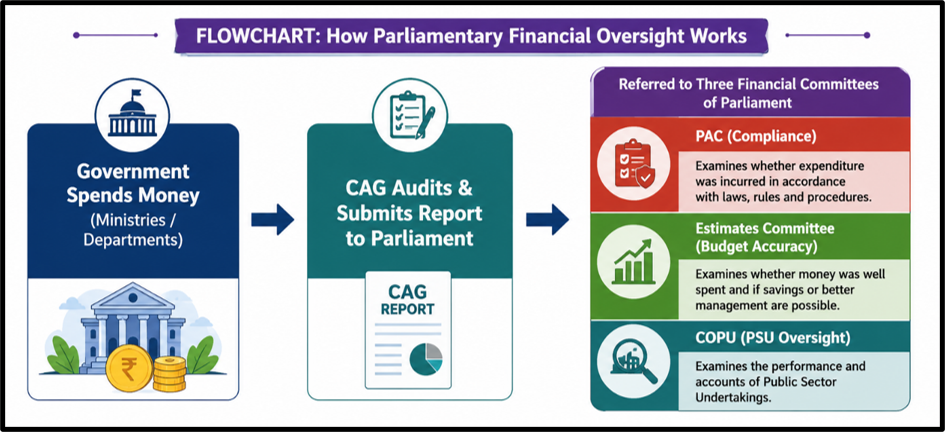

Parliamentary Control on Expenditure — The Three Financial Committees

CAG audits alone are not sufficient for accountability. Parliament itself needs mechanisms to scrutinise government expenditure. This is achieved through three specialised Financial Committees of Parliament. CAG reports stand automatically referred to these Committees upon presentation to Parliament.

| Committee | What It Scrutinises | Key Focus |

| Public Accounts Committee (PAC) | CAG’s Compliance & Finance Account reports. Checks if money was used legally and for its appropriated purpose. | Legality and appropriateness of past expenditure |

| Estimates Committee | Accuracy of Budget Estimates vs. actual expenditure. Scrutinises surrenders and re-appropriations of funds. | Budget accuracy and fiscal discipline |

| Committee on Public Undertakings (COPU) | Financial oversight over PSUs — examines policies, programmes, and financial workings based on CAG performance audit reports. | PSU efficiency and commercial performance |

Read in detail about financial Committees here: Financial Committees – CDH IAS

Canons of Financial Propriety — The Ethical Foundation

We have seen the systems, the schemes, the audits, and the committees. But underlying all of this is an ethical foundation — the Canons of Financial Propriety. These are codified in the General Financial Rules (GFR), 2017 (which replaced GFR 2005). Every government officer who handles public money must observe these canons.

| 💡 Core Idea: These canons are not just bureaucratic rules. They are the moral principles of public financial management. A civil servant who internalises these canons doesn’t need external supervision — they become the internal auditor of their own conscience. |

The Seven Canons of Financial Propriety (GFR 2017, Rule 21)

| # | Canon of Financial Propriety |

| I | Prudent Stewardship: Every officer must exercise the same vigilance over public money as a person of ordinary prudence would exercise over their own money. |

| II | No Extravagance: Expenditure should not be more than the occasion demands — no ostentation or lavishness in public spending. |

| III | No Self-Benefit: No authority should sanction expenditure that will be directly or indirectly to its own advantage. |

| IV | Public Interest Only: Public funds should not be used for the benefit of a particular person or group, unless a legal claim exists or it is in pursuance of a recognised policy. |

| V | No Profit from Allowances: Allowances granted to meet specific expenditure (e.g., TA, HRA) should not be a source of profit for the recipients. |

| VI | No Waste or Misappropriation: There must be no waste, misappropriation, or fraudulent use of public resources. Economy must be enforced while ensuring delivery of intended services. |

| VII | Transparent Procurement: All procurement must be done with transparency, competition, and fairness — principles now operationalised through GeM and GFR 2017 procurement rules. |

Conclusion — Ethics at the Heart of Public Finance

The framework for utilisation of public funds in India has undergone fundamental transformation since 2014. The abolition of the Planning Commission and Five Year Plans, the removal of the Plan/Non-Plan distinction, the launch of PFMS and the DBT-JAM ecosystem, the rationalisation of CSSs, and the creation of GeM — together represent a new architecture of public financial management in India.

The Union Budget 2026-27, with total expenditure of ₹53.5 lakh crore and capital expenditure of ₹12.2 lakh crore, reflects the expanding scale of public financial operations. Social sector spending has risen to 7.8% of GDP (2023-24), and the JAM trinity has enabled DBT savings of ₹3.48 lakh crore.

Yet, persistent challenges remain: delayed fund releases and last-quarter bunching, over-reporting of programme performance, inadequate PRI capacity, staff shortages, and exclusion errors in DBT delivery.

| The Civil Servant’s Ethical Duty: For a civil servant, the utilisation of public funds is ultimately an ethical responsibility. Public money is held in trust — it belongs to the citizens whose taxes and borrowings finance government. The Canons of Financial Propriety as codified in GFR 2017 demand that every official exercise the vigilance of a trustee, not a spendthrift. Accountability is not just a procedural requirement — it is a moral imperative. |