Liquidity Adjustment Facility

Introduction

The Liquidity Adjustment Facility (LAF) is the mechanism through which the Reserve Bank of India manages day-to-day liquidity conditions in the banking system and signals the monetary policy stance.

In simple words, LAF is the RBI’s daily toolkit to inject or absorb money from banks, ensuring that liquidity remains neither too tight nor too excessive.

Why LAF Is Needed

In a modern economy:

- Some banks face temporary shortage of funds

- Others may have temporary surplus liquidity

LAF provides a formal, rule-based window through which banks can:

- Borrow from RBI when short of funds

- Park excess funds with RBI safely

Thus, LAF ensures smooth functioning of the financial system and effective monetary transmission.

Components of Liquidity Adjustment Facility (LAF)

LAF operates through three major instruments, which together create what is called the liquidity corridor.

- Repo and Reverse Repo Operations

Banks can either borrow money from the RBI (repo operations) or lend money to the RBI (reverse repo operations) depending on their liquidity situation. These operations can be overnight or for a specified term, and the rates can be fixed or variable - Marginal Standing Facility (MSF)

This allows banks to borrow funds overnight from the RBI against government securities, at a rate higher than the repo rate, thus forming the ceiling of the liquidity corridor. - Standing Deposit Facility (SDF)

This allows banks to deposit excess funds with the RBI without needing collateral, at a rate typically lower than the repo rate. It helps in setting the floor of the liquidity corridor.

We will discuss each of them further in detail later on in this section

How LAF Works in Practice

Liquidity Injection

When banks face a shortage of funds:

- They borrow through Repo operations

- Or use MSF in emergency situations

👉 Result: Liquidity is injected into the banking system

Liquidity Absorption

When banks have excess funds:

- They park money via Reverse Repo

- Or deposit funds under SDF

👉 Result: Surplus liquidity is absorbed, preventing inflationary pressures

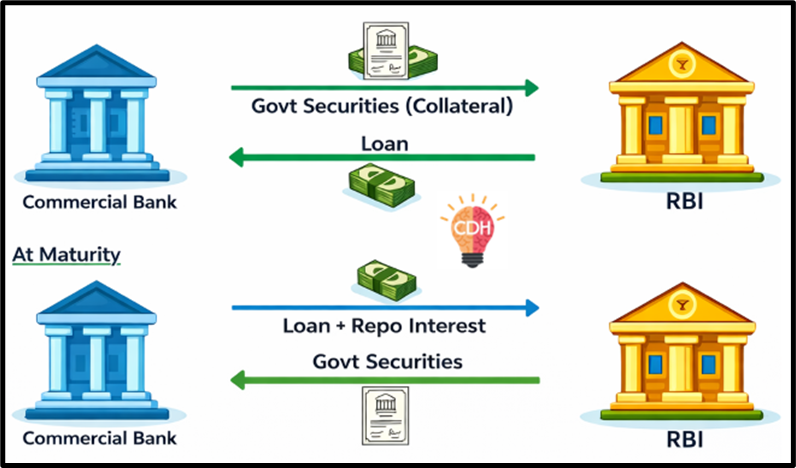

Repo Rate

The Repo Rate is the policy rate at which RBI lends short-term funds to commercial banks.

How a Repo Transaction Works

- Bank needs short-term funds

- Offers government securities to RBI

- RBI lends money

- Bank agrees to repurchase securities later at a higher price

- The difference is interest, calculated at the repo rate

Numerical Illustration

- Loan amount = ₹10 crore

- Repo rate = 6.5%

- Duration = 14 days

Interest charged: (6.5% × ₹10 crore × 14 / 365) ≈ ₹0.025 crore

Economic Impact of Repo Rate Changes

| Repo Rate | Impact |

|---|---|

| Repo ↑ | Borrowing cost ↑ → Lending rates ↑ → Credit demand ↓ → Inflation control |

| Repo ↓ | Borrowing cost ↓ → Lending rates ↓ → Credit demand ↑ → Growth stimulus |

📌 UPSC Insight:

Repo rate is the most visible signalling tool of monetary policy.

Reverse Repo Rate

The Reverse Repo Rate is the rate at which:

- Banks lend money to RBI

- RBI absorbs surplus liquidity

Role in Current Framework

With the introduction of SDF, reverse repo:

- Is used selectively

- Becomes a supporting absorption tool, not the primary one

Overnight vs Term Repos

Based on duration, repos and reverse repos are:

- Overnight: One-day transactions

- Term: Longer duration (e.g., 7 days, 14 days)

This allows RBI to fine-tune liquidity depending on market conditions.

Overnight and Term Operations under LAF

Broadly, repo and reverse repo operations are classified into:

- Overnight Repo and Reverse Repo

- Term Repo and Term Reverse Repo

Overnight Repo and Overnight Reverse Repo

The overnight repo and reverse repo are the most frequently used liquidity instruments of the Reserve Bank of India. They help banks manage day-to-day liquidity mismatches.

How They Work

- If a bank faces a shortage of funds, it borrows from RBI through the overnight repo window.

- If a bank has surplus funds, it parks them with RBI through the overnight reverse repo window.

Key Feature: Duration

- These operations are strictly for one day (overnight).

- Funds are borrowed or parked today and returned the next working day.

Purpose

- Smooth functioning of the payment system

- Managing daily liquidity fluctuations

- Ensuring stability in overnight money market rates

📌 Conceptual Insight:

Overnight repo/reverse repo acts like a daily balancing mechanism, correcting small mismatches that arise due to withdrawals, payments, or settlements.

Term Repo (Variable Rate Repo – VRR)

A term repo is a repurchase agreement where banks borrow funds from RBI for a period longer than one day. The word “term” indicates extended duration.

Because the interest rate is decided through auctions, term repos are also called Variable Rate Repos (VRR).

Duration in India

Common tenors include → 7 days, 14 days, 28 days

How Term Repo Differs from Overnight Repo

- Funds are locked in for a longer duration

- Interest rate is not fixed

- Rate is decided via competitive auction

- Generally, the rate is higher than the repo rate

Auction-Based Mechanism

- RBI pre-announces the total amount to be injected

- Banks submit bids:

- Amount required

- Interest rate they are willing to pay

- RBI determines a cut-off rate

- Bids below the cut-off are rejected

📌 Important Rule:

The cut-off rate is above the repo rate, ensuring that term repos do not undercut the policy rate.

Example

- Bank A needs ₹1,000 crore for 14 days

- RBI announces a VRR auction of ₹5,000 crore

- Repo rate = 6%

- Bank A bids at 7% to increase chances of allotment

- If the cut-off is below 7%, Bank A:

- Gets ₹1,000 crore

- Pays interest at 7%

- Provides government securities as collateral

- At maturity, Bank A repurchases securities by paying principal + interest

Purpose of Term Repos

- Managing medium-term liquidity

- Reducing over-dependence on overnight borrowing

- Improving liquidity forecasting and stability

Term Reverse Repo (Variable Rate Reverse Repo – VRRR)

A term reverse repo is the opposite of a term repo:

- Banks deposit surplus funds with RBI

- Funds are parked for more than one day

Since rates are auction-determined, these are also called Variable Rate Reverse Repos (VRRR).

Why Higher Returns?

- Funds are locked for longer duration

- Hence, interest earned is higher than overnight reverse repo

Auction Process

- RBI announces:

- Total liquidity to be absorbed

- Duration (e.g., 7 days)

- Banks bid the minimum rate they are willing to accept

- RBI decides cut-off rate (usually above reverse repo rate)

Example

If post-festive season liquidity is excessive:

- RBI may absorb ₹20,000 crore for 7 days

- Banks bid in a VRRR auction

- Successful bids park surplus funds with RBI

- Excess liquidity is temporarily withdrawn, preventing inflationary pressure

Overnight vs Term Repo/Reverse Repo: Key Differences

| Feature | Overnight Repo / Reverse Repo | Term Repo / Reverse Repo |

| Duration | Overnight (1 day) | More than one day (7, 14, 28 days) |

| Purpose | Daily liquidity management | Medium-term liquidity management |

| Availability | Daily (Mon–Fri) | Scheduled by RBI (usually twice a week) |

| Rate | Fixed by RBI | Variable, via auction |

| Collateral | Government securities | Government securities |

| Use Case | Short-term deficits or surpluses | Liquidity planning and stability |

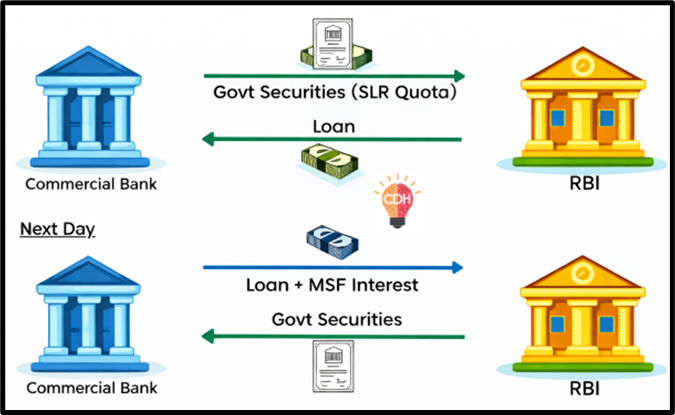

Marginal Standing Facility (MSF)

The Marginal Standing Facility (MSF) is an overnight borrowing facility under which commercial banks can borrow funds from the Reserve Bank of India by pledging government securities from their SLR holdings.

Key Characteristics

- Borrowing is overnight

- Securities are drawn from SLR quota

- Borrowing limit: up to 2% of NDTL

- MSF rate > Repo rate

- Minimum borrowing: ₹1 crore (and in multiples thereof)

📌 Because the rate is higher than the repo rate, MSF is treated as a penal or emergency rate.

Why MSF Is Needed

In normal situations, banks meet liquidity needs through → Inter-bank market, Repo window

However, during sudden liquidity stress (large withdrawals, settlement mismatches, market panic), these avenues may be insufficient. MSF acts as a last-resort safety valve.

Numerical Illustration

Assume:

- Bank A’s NDTL = ₹100 crore

- Required SLR = 18% → ₹18 crore

Under MSF:

- Maximum borrowing allowed = 2% of NDTL = ₹2 crore

Scenario:

- Due to unexpected withdrawals, Bank A faces a cash shortage

- It pledges ₹2 crore worth of SLR securities

- Borrows ₹2 crore overnight from RBI at MSF rate

👉 Even though borrowing is costlier, the bank survives the liquidity stress without defaulting or triggering panic.

Importance of MSF Rate

1. Emergency Liquidity Support

MSF ensures that temporary liquidity stress does not turn into a systemic crisis.

2. Upper Ceiling of LAF Corridor

In the liquidity corridor:

- Repo rate → policy anchor

- MSF rate → upper bound

This prevents short-term interest rates from rising uncontrollably during stress.

3. Discipline in Banking System

Since MSF is a penal rate, banks avoid habitual dependence on it, encouraging:

→ Better liquidity planning

→ Responsible risk management

📌 UPSC Keyword: MSF acts as lender-of-last-resort window within LAF.

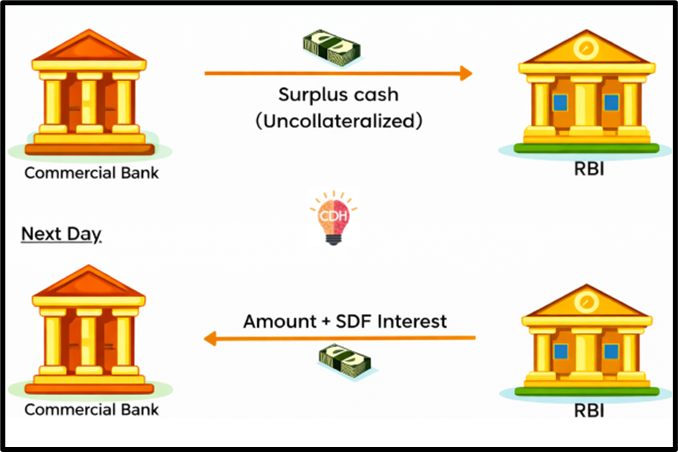

Standing Deposit Facility (SDF)

The Standing Deposit Facility (SDF) is the rate at which RBI accepts uncollateralized overnight deposits from commercial banks.

Introduced to strengthen liquidity absorption, SDF allows banks to park excess funds safely with RBI without providing collateral.

How SDF Works (Intuitive View)

Think of SDF as a safe parking space for excess cash.

- If a bank has surplus liquidity at the end of the day

- And does not want to lend it in the market

- It can deposit the amount with RBI overnight

- And earn interest at the SDF rate

Simple Example

- SDF rate = 6%

- Bank has surplus = ₹10 crore

The bank deposits ₹10 crore with RBI overnight and earns interest at 6% per annum (pro-rated for one day).

While the absolute amount earned is small, the certainty and safety are crucial.

Importance of SDF Rate

1. Efficient Liquidity Management

SDF helps RBI absorb excess liquidity smoothly without flooding the system with cheap money that could fuel inflation.

2. Floor of the Liquidity Corridor

SDF forms the lower bound of the corridor:

- Banks will not lend below SDF rate

- Because they can earn a risk-free return from RBI

This stabilises overnight money market rates.

3. Financial Stability

By providing a risk-free return, SDF:

- Prevents interest rates from falling too low

- Discourages excessive risk-taking in search of returns

📌 UPSC Value Addition:

SDF strengthens RBI’s control over short-term rates without collateral constraints, unlike reverse repo.

MSF and SDF in the Liquidity Corridor (Big Picture)

| Instrument | Role |

|---|---|

| MSF | Upper ceiling (penal borrowing rate) |

| Repo | Policy anchor |

| SDF | Lower floor (safe deposit rate) |

👉 This corridor ensures that market interest rates remain stable, predictable, and policy-aligned.

Analogy:

Imagine RBI managing liquidity like traffic:

- MSF is the emergency lane—used only when normal routes fail

- Repo is the main highway—regular movement of funds

- SDF is the parking zone—where excess vehicles are safely kept

Together, MSF and SDF complete the operational architecture of LAF, making India’s monetary policy framework robust, disciplined, and crisis-resilient.

Liquidity Adjustment Facility (LAF) Corridor

(The Operating Framework of Monetary Policy)

After understanding repo, MSF, and SDF individually, we now integrate them into a single operational structure called the Liquidity Adjustment Facility (LAF) Corridor. This is one of conceptually important, because it explains how RBI stabilises short-term interest rates in practice.

The LAF Corridor is a framework used by the Reserve Bank of India to:

- Manage systemic liquidity, and

- Keep short-term money market rates within a predictable range.

Structure of the LAF Corridor

The corridor has three clearly defined layers:

1. MSF Rate – Upper Bound (Ceiling)

2. Policy Repo Rate – Middle (Anchor)

3. SDF Rate – Lower Bound (Floor)

Together, they form a rate corridor within which the Call Money Rate (overnight interbank lending rate) fluctuates.

MSF Rate – Ceiling of the Corridor

- The Marginal Standing Facility (MSF) rate is normally set 25 basis points (0.25%) above the repo rate.

- It acts as a hard ceiling for overnight interest rates.

Why a Ceiling Is Needed

During liquidity shortages:

- Banks may scramble for funds

- Interbank rates can spike sharply

The MSF ensures that:

No bank will borrow at rates higher than MSF, because it can always borrow from RBI at that rate.

📌 Result: Overnight rates are prevented from rising uncontrollably.

SDF Rate – Floor of the Corridor

- The Standing Deposit Facility (SDF) rate is usually set 25 basis points below the repo rate.

- It forms the floor of the corridor.

Why a Floor Is Needed

During excess liquidity:

- Banks may try to lend at very low rates

- This can distort markets and encourage risk-taking

SDF ensures that:

Banks will not lend below the SDF rate, because they can earn a safe return from RBI.

📌 Result: Overnight rates do not crash downward.

Policy Repo Rate – Middle of the Corridor

- The Repo Rate is the policy signal rate.

- RBI intends short-term market rates to gravitate around this rate.

📌 Think of the repo rate as the gravitational centre of the money market.

Numerical Illustration

Suppose:

- Repo Rate = 4.00%

- MSF Rate = 4.25%

- SDF Rate = 3.75%

This creates a 50 basis point corridor (±25 bps).

Case 1: Liquidity Tight

- Banks face fund shortages

- They borrow via MSF at 4.25%

- Call money rate cannot exceed 4.25%

Case 2: Excess Liquidity

- Banks park funds at SDF at 3.75%

- Call money rate cannot fall below 3.75%

👉 Thus, interest rate volatility is contained within the corridor.

Why the LAF Corridor Is So Important

- Anchors short-term interest rates

- Improves monetary transmission

- Enhances predictability and credibility of policy

- Allows RBI to manage liquidity without frequent CRR/SLR changes

📌 So, we can say:

The LAF corridor operationalises monetary policy by aligning overnight market rates with the policy repo rate.

Who Can Avail the Liquidity Adjustment Facility (LAF) Window of RBI

After understanding how LAF works, a very natural question is:

👉 Who is actually allowed to access this liquidity window?

The Liquidity Adjustment Facility (LAF) of the Reserve Bank of India is primarily designed to help regulated financial institutions manage short-term liquidity mismatches, while ensuring systemic stability and discipline.

Eligible Participants in the LAF

1. Scheduled Commercial Banks (SCBs)

Scheduled Commercial Banks are the primary and most frequent users of the LAF.

This category includes → Public Sector Banks, Private Sector Banks, Foreign Banks operating in India, Small Finance Banks, Payments Banks

📌 Why SCBs are central to LAF

They form the backbone of India’s credit system, and their liquidity conditions directly affect → Credit flow, Payment systems, Monetary transmission

2. Cooperative and Regional Banking Institutions (Expanded Coverage)

To deepen liquidity management and ensure financial inclusion, RBI gradually expanded LAF access beyond commercial banks.

a) Scheduled Urban Cooperative Banks (UCBs) – since 2014

UCBs are eligible subject to conditions, such as:

→ Implementation of Core Banking Solution (CBS)

→ Minimum CRAR of 9%

CRAR is Capital to Risk-Weighted Assets Ratio

b) State Cooperative Banks (StCBs) – since 2018

→ Included under conditions similar to UCBs

→ Strengthened liquidity support for state-level cooperative banking

c) Regional Rural Banks (RRBs) – since 2020

Eligibility conditions include → CBS implementation; Minimum CRAR of 9%

📌 Significance

This move ensured better liquidity management in rural and agricultural credit systems, especially during stress periods.

Positive List and Negative List Mechanism

To maintain discipline, RBI follows a filtering mechanism:

- Positive List → Institutions that meet eligibility norms and are allowed to participate in LAF

- Negative List → Institutions that fail to meet norms and are barred from participation

👉 This ensures that only financially sound institutions access RBI liquidity

Role of Primary Dealers (PDs) in LAF

Apart from banks, Primary Dealers (PDs) are also key participants in LAF operations.

Primary Dealers are specialised institutions (mostly NBFCs) authorised by RBI to deal in government securities.

Examples include:

- Goldman Sachs (India) Capital Markets Pvt. Ltd.

- ICICI Securities Primary Dealership Ltd.

- Morgan Stanley India Primary Dealer Pvt. Ltd.

Why PDs Matter in Monetary Operations

1. Market Making

PDs continuously quote buy and sell prices for government securities.

This:

- Ensures liquidity in the G-sec market

- Prevents sharp price volatility

- Allows smooth entry and exit for investors

📌 Without PDs, the government securities market would become thin and unstable.

2. Underwriting Government Borrowings

PDs commit to subscribing to government bond issues.

Example:

- Government issues ₹10,000 crore worth of bonds

- Market bids come for only ₹9,000 crore

- PDs absorb the remaining ₹1,000 crore

👉 This guarantees successful completion of government borrowing programmes.

3. Participation in RBI Operations

PDs actively participate in:

- Open Market Operations (OMOs)

- Repo and reverse repo auctions

Thus, PDs act as a bridge between RBI and the bond market.

To explore all Indian Economy topics in a structured manner, visit the complete Indian Economy UPSC Notes page.

One Comment