Public Expenditure Management

Public Expenditure Management refers to the systematic, prudent, and efficient use of government financial resources to achieve good governance and developmental outcomes.

It is not merely about spending money, but about → how well, where, and with what results public money is spent.

Core Objectives of PEM

PEM rests on three foundational pillars:

1. Aggregate Fiscal Discipline

- Ensuring that total government expenditure is aligned with → revenues, borrowing capacity

- Prevents unsustainable deficits and debt

In essence → Do not spend beyond long-term fiscal capacity.

2. Allocative Efficiency

- Resources must go to → priority sectors, programs aligned with national goals

- Avoids wasteful or low-impact spending

In simple terms → Are we spending on the right things?

3. Operational Efficiency

- Focuses on value for money

- Ensures → reasonable cost, acceptable quality of public services

This asks → Are we delivering services efficiently?

Challenges in India’s Public Expenditure Management

Despite reforms, India faces structural and operational challenges.

1. Fiscal Deficit Pressure

- Rising demands for → infrastructure, welfare, social security

- Must be balanced against → fiscal discipline, debt sustainability

This creates a policy trade-off between growth and prudence.

2. Subsidy Burden

- Large subsidies in fertilizers, food, welfare schemes

Issues → Leakage, Inefficient targeting, Rising fiscal cost

3. Banking Sector Stress

- Problems like → Twin Balance Sheet crisis, High Non-Performing Assets (NPAs)

Impact:

- Reduces effectiveness of public spending

- Weakens credit transmission

4. Public Sector Enterprises (PSEs)

- Many PSEs remain → loss-making, inefficient

Policy dilemma → Disinvestment, Strategic privatization, Revival vs exit

5. Populist Schemes

Examples → Farm loan waivers, Higher Minimum Support Prices (MSPs)

Challenges → Political appeal vs fiscal cost, Long-term distortion of incentives

6. Low Tax Base and Tax-to-GDP Ratio

- Narrow tax base

- Large informal sector

Result:

- Limited revenue mobilisation

- Higher dependence on borrowing

7. Operational Inefficiencies

- Bureaucratic delays

- Weak accountability

- Poor outcome monitoring

This directly affects service delivery quality.

Steps Taken by the Government to Address These Challenges

India has moved from spending control to spending quality.

Fiscal Reforms

Fiscal Responsibility and Budget Management (FRBM) Act

- Sets numerical targets for → fiscal deficit, revenue deficit, debt-to-GDP ratio

Objective:

Ensure fiscal discipline and long-term sustainability.

(We will examine FRBM in detail shortly.)

Outcome-Based Budgeting

- Links: allocations → outcomes

- Shifts focus from: spending → results

This directly improves allocative and operational efficiency.

Technology Adoption

Public Fund Management System (PFMS)

- Online platform to → track fund flow, monitor scheme implementation

Benefits → Reduces leakages, Improves transparency

Digital Platforms

- Direct Benefit Transfer (DBT)

- Real-time dashboards

Impact → Better accountability, Faster service delivery

Capacity Building

- Training government officials

- Strengthening implementing agencies

Why it matters → Even the best-designed budget fails without administrative capacity.

Subsidy Rationalization

- Reviewing existing subsidies

- Improving targeting

- Phasing out inefficient subsidies

Goal → Shift from blanket subsidies to need-based support.

Governance Strengthening

Anti-Corruption Measures → Transparency in procurement, Audits and vigilance

Institutional Mechanisms → Strengthening bodies responsible for:expenditure monitoring and evaluation. This ensures rule-based fiscal management.

Deepening Fiscal Federalism

- Higher devolution of taxes to states

- Empowering states to → plan, spend, innovate

This improves → regional responsiveness, accountability

Public Debt Management Agency (Proposed)

Purpose → Professional management of internal debt and external debt

Objective → Reduce borrowing costs, Improve risk management

This separates debt management from monetary policy

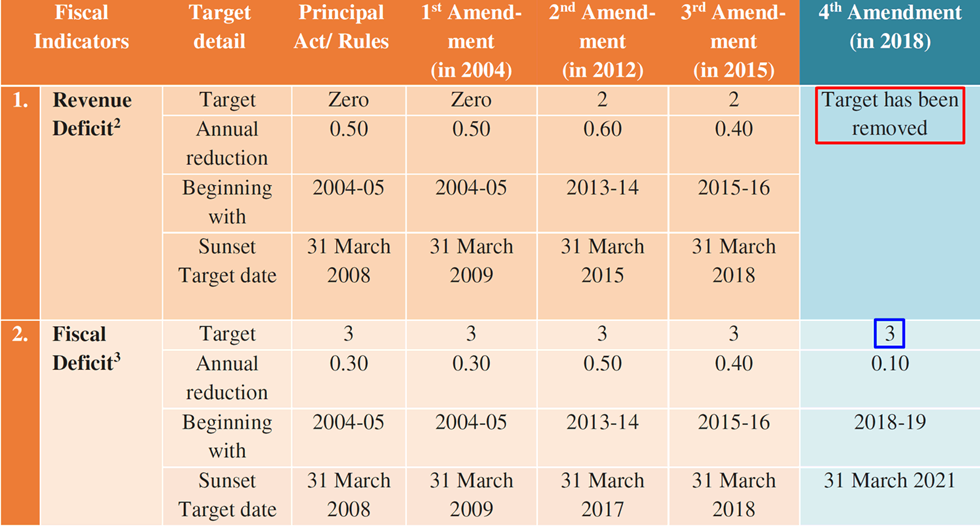

Fiscal Responsibility and Budget Management (FRBM) Act, 2003

The Fiscal Responsibility and Budget Management Act, enacted in 2003, is essentially about bringing discipline to government finances.

Think of the government like a household.

If expenditure keeps exceeding income year after year, debt piles up and stability is lost. The FRBM Act was introduced to prevent exactly this situation at the national level.

Core Idea

👉 Balance between Government Revenue and Government Expenditure, not necessarily zero deficit, but controlled and sustainable deficits.

Objectives of the FRBM Act

The Act clearly lays down why fiscal discipline is necessary:

- Fiscal discipline

– To prevent reckless borrowing and overspending. - Efficient management of expenditure, revenue, and debt

– Borrow only what you can responsibly repay. - Macroeconomic stability

– Stable inflation, sustainable growth, and investor confidence. - Better coordination between fiscal and monetary policy

– Government borrowing should not clash with the RBI’s monetary objectives. - Transparency in fiscal operations

– Parliament and citizens should clearly know the fiscal position of the government.

Deficit Targets under FRBM

The Act introduced numerical targets for deficits—this is its most distinctive feature.

- Targets were prescribed as a percentage of GDP

- Applicable to Union and State Governments

- Targets have evolved through amendments in 2012, 2015, and 2018, reflecting changing economic realities.

Salient Features (Section 4 and Section 5)

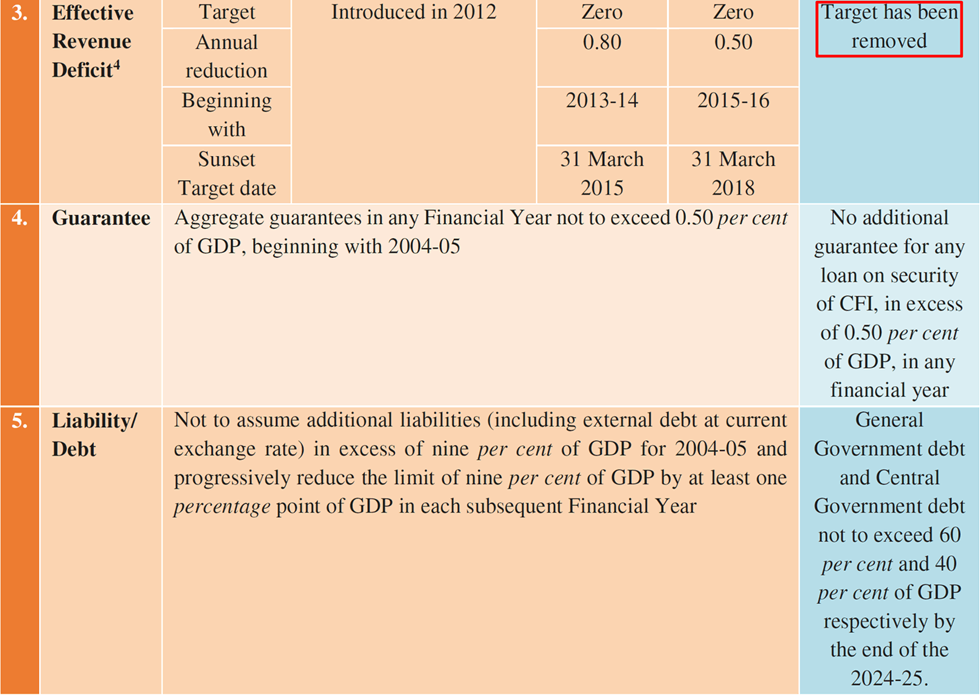

Section 4(1): Fiscal and Debt Targets

The Central Government must:

- Limit fiscal deficit to 3% of GDP

- Ensure by FY 2024–25:

- General Government Debt ≤ 60% of GDP

- Central Government Debt ≤ 40% of GDP

- Cap guarantees on loans backed by the Consolidated Fund of India to 0.5% of GDP per year

- Make continuous efforts to not exceed targets after stipulated deadlines

📌 Note: “Endeavour” is a carefully chosen word—it allows flexibility without abandoning responsibility.

Section 5: Borrowing from RBI

- Except under special circumstances, the Central Government cannot borrow directly from the RBI

- This avoids monetisation of deficit, which can fuel inflation

Here, the independence of the Reserve Bank of India is protected.

Parliamentary Oversight and Accountability

- The Finance Minister must conduct half-yearly reviews of receipts and expenditure

- These reviews must be placed before both Houses of Parliament

This ensures democratic scrutiny, not just executive control.

CAG Audit (2012 Amendment)

- The Comptroller and Auditor General (CAG) was empowered to periodically review compliance with FRBM provisions

- This transformed FRBM from a policy intent into an auditable fiscal rule

FRBM Review Committee (N.K. Singh Committee)

Over time, the government felt that FRBM targets had become too rigid, especially during economic slowdowns.

Why the Committee was formed (2016)?

- To reassess the framework

- To introduce flexibility without fiscal irresponsibility

The committee was chaired by N. K. Singh.

Key Recommendations

1. Debt as the Primary Fiscal Anchor

- Debt is more stable and long-term than annual deficits.

Target Debt-to-GDP Ratio: 60% overall → 40% Centre, 20% States

2. Fiscal Deficit Targets

- Reduce to 2.5% of GDP by March 31, 2023

- Minimum annual reduction: 0.3% of GDP

3. Revenue Deficit Targets

- Reduce to 0.8% of GDP by March 31, 2023

- Minimum annual reduction: 0.5% of GDP

📌 This reflects a shift from borrowing for consumption to borrowing for investment

FRBM Act – Escape Clause (2018 Amendment)

Economic reality is unpredictable. Hence, flexibility was formally introduced through Section 4(2).

What is the Escape Clause?

It allows temporary deviation from fiscal targets under exceptional circumstances.

Trigger Conditions:

- National security / Act of war

- National calamity

- Collapse in agricultural output and farm incomes

- Sharp fall in real GDP growth

- Structural reforms with unforeseen fiscal impact

Extent of Deviation

- Fiscal deficit can exceed the target by up to 0.5% of GDP

- States may also over-cross by 0.5% of GSDP, after amending their FRBM laws

📌 If triggered, RBI can participate directly in primary bond auctions, formally allowing deficit financing.

Post-Pandemic Relaxations

- For 2019-20 and 2020-21, structural reforms were cited to invoke the escape clause

- Budget 2021 amended FRBM to set:

- Fiscal deficit target of 4.5% by 2025–26

- As recommended by the 15th Finance Commission

Key Terms for UPSC

- Fiscal Glide: Gradual reduction of fiscal deficit over time

- Fiscal Profligacy: Reckless or wasteful public expenditure

- Fiscal Slippage: Failure to meet fiscal deficit targets

Transparency: Documents Mandated by FRBM

To ensure informed debate, the government must present these along with the Budget:

- Macroeconomic Framework Statement

– GDP growth, inflation, receipts, expenditure - Medium-Term Fiscal Policy Statement

– Fiscal goals over the medium term - Fiscal Policy Strategy Statement

– Strategy to achieve fiscal objectives - Medium-Term Expenditure Framework

– Future expenditure commitments

This topic is covered under the Indian Economy notes series designed for UPSC Prelims, Mains, and Interview preparation.