Goods and Services Tax (GST)

The introduction of Goods and Services Tax (GST) marks a structural transformation in India’s indirect tax regime. It is not merely a change in tax rates; it is a shift in taxation philosophy—from fragmented, origin-based taxes to a unified, destination-based value-added tax system.

What is GST?

GST is an indirect tax introduced in India on 1 July 2017. It replaced a large number of indirect taxes such as VAT, excise duty, and service tax with a single unified tax.

Core Features of GST

- Levied on supply of goods and services

- Value-added based taxation

- Destination-based tax (tax accrues to the state of consumption)

- Final burden borne by the consumer

In essence, GST ensures that tax is levied only on value addition, not on the total value repeatedly.

Types of GST in India

To accommodate India’s federal structure, GST is divided into four components:

1. CGST (Central Goods and Services Tax)

- Levied by the Central Government

- Applicable on intra-state supply of goods and services

2. SGST (State Goods and Services Tax)

- Levied by State Governments

- Applicable on intra-state supply

- Collected alongside CGST

3. IGST (Integrated Goods and Services Tax)

- Levied by the Central Government

- Applicable on inter-state supply of goods and services

- Later apportioned between Centre and destination State

4. UTGST (Union Territory Goods and Services Tax)

- Levied by Union Territories

- Applicable on intra-UT supply (without legislature)

➡️ Key exam line:

“GST preserves fiscal federalism through dual taxation on a common tax base.”

GST Council

The GST Council is a constitutional body created under the 101st Constitutional Amendment Act, 2016.

Composition

- Chairperson: Union Finance Minister

- Members:

- Finance Ministers of all States

- Finance Ministers of Union Territories

Functions

- Recommends → GST tax rates, Exemptions, Threshold limits, Model GST laws

Significance

- Institutionalises cooperative federalism

- Ensures consensus-based decision-making

- Acts as a forum for Centre–State coordination

Significance of GST

GST has brought systemic improvements in India’s tax administration:

1. Simplification of Tax Administration

- Replaced multiple taxes with a single tax framework

- Reduced multiplicity of laws and authorities

2. Reduction in Tax Evasion

- Input Tax Credit (ITC) creates a self-policing mechanism

- Encourages invoice-based compliance

3. Boost to Economic Growth

- Reduces transaction costs

- Improves ease of doing business

- Enhances competitiveness of Indian firms

GST Rate Structure in India and GST 2.0 Reforms

India follows a multi-rate GST structure to balance simplicity, equity, and revenue mobilisation.

The 56th meeting of the GST Council introduced GST 2.0, significantly rationalising GST slabs to improve compliance and reduce classification disputes.

Revised GST Slabs (Effective from 22 September 2025)

| GST Rate | Category | Illustrative Examples |

|---|---|---|

| 0% (Nil / Exempt) | Essential goods & services | Milk and dairy products, basic food items, 33 lifesaving drugs, educational materials, education services, healthcare services, individual health & life insurance |

| 5% (Merit / Essentials Rate) | Daily-use & socially important goods | Agricultural goods, basic packaged food items, healthcare equipment, essential household items |

| 18% (Standard Rate) | Majority of goods & services | Electronics, appliances, small cars, motorcycles, telecom services, IT services |

| 40% (Demerit / Sin Goods Rate) | Luxury & harmful goods | Pan masala, aerated and caffeinated beverages, luxury vehicles, select high-end consumer goods |

Note: Tobacco products continue under a separate treatment with additional cesses and are excluded from some of these rationalisations.

For a detailed breakdown of the actual items covered, you may explore the complete list here.

Key Features of GST 2.0 Reforms

- Slab Rationalisation

- Earlier slabs of 12% and 28% have been removed.

- GST now primarily operates with three effective rates: 5%, 18%, and 40%, apart from nil-rated items.

- Equity Orientation

- Essential consumption items and merit goods are either exempted or taxed at 5%, protecting vulnerable sections.

- Compliance & Ease of Doing Business

- Fewer slabs reduce disputes over classification and valuation.

- Notifications also align exemptions, refunds, and procedural rules with new rates.

- Revenue & Health Objectives

- A sharply higher 40% slab targets sin and luxury goods, serving both revenue mobilisation and public health goals.

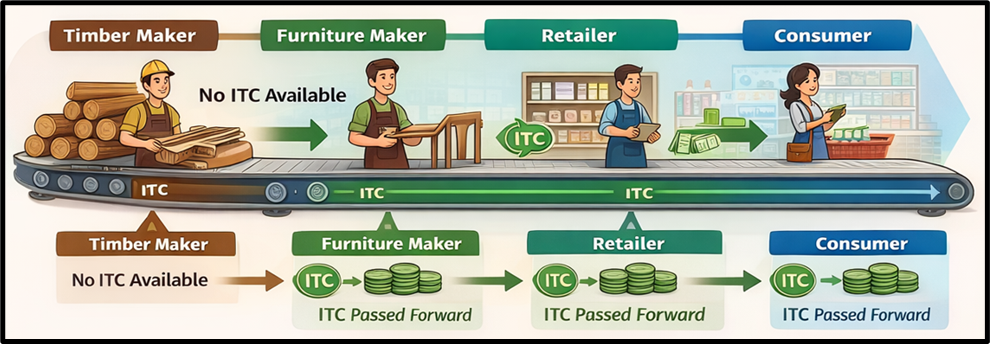

Understanding the Working of GST

GST is designed to eliminate the cascading effect of taxes through Input Tax Credit (ITC).

Input Tax Credit (ITC)

- Credit for tax paid on inputs

- Can be adjusted against output tax liability

- Ensures tax is paid only on value added

Illustration: GST Working Within a State

Stage A: Timber Maker → Furniture Maker

- Value of timber = ₹100

- GST @ 20% = ₹20

- Total price = ₹120

- GST paid to government = ₹20

(no ITC available)

Stage B: Furniture Maker → Retailer

- Value of furniture = ₹200

- GST @ 20% = ₹40

- ITC available = ₹20

- Net GST paid = ₹20

👉 Tax effectively on ₹100 value added

Stage C: Retailer → Consumer

- Sale price = ₹300

- GST @ 20% = ₹60

- ITC available = ₹40

- Net GST paid = ₹20

👉 Tax on ₹100 value added

Final Outcome

| Participant | GST Paid |

| Timber Maker | ₹20 |

| Furniture Maker | ₹20 |

| Retailer | ₹20 |

| Total GST | ₹60 |

➡️ The entire tax burden is borne by the consumer, while businesses act as tax collectors with credit protection.

Benefits of GST

- Elimination of cascading effect

- Uniform tax structure across India

- Increased tax compliance

- Higher revenue efficiency

- Integrated national market

Compensation to States

Why Compensation Was Needed?

The shift to GST risked short-term revenue loss for States.

Legal Framework

- GST (Compensation to States) Act, 2017

- Compensation guaranteed for five years

Funding Mechanism

- GST Compensation Cess

- Levied on luxury and sin goods

- Collected into GST Compensation Fund

Compensation Logic

- If actual revenue growth < projected growth

- Shortfall compensated from the fund

➡️ Objective: Ensure smooth transition and fiscal stability for States.

Challenges with GST

Despite its success, GST faces challenges:

1. Technical Issues

- GST Network (GSTN) glitches

- Return filing delays

2. Compliance Burden

- Especially heavy for small businesses

- Frequent rule changes

3. Revenue Concerns

- Some States experienced revenue shortfalls

- Dependence on compensation mechanism

Concluding Insight

GST represents a paradigm shift from “many taxes” to “one tax”, from fragmentation to integration, and from cascading to value addition. While challenges remain, GST has laid the foundation for a modern, transparent, and efficient indirect tax system in India.

This topic is covered under the Indian Economy notes series designed for UPSC Prelims, Mains, and Interview preparation.

One Comment