Introduction to Financial Market

Imagine an economy as a vast network of people and institutions where some participants have surplus money, while others need funds to expand their activities. For instance, a household may save part of its income but may not know where to invest it profitably. At the same time, a growing company may need capital to build a new factory, purchase advanced machinery, or expand its production.

Similarly, governments require funds to build infrastructure such as highways, railways, and power plants. Financial markets act as the meeting ground where these two sides—savers and borrowers—connect. Through this system, individuals who want to invest their savings can purchase financial instruments like stocks, bonds, or other securities, while businesses and governments obtain the funds they need for development.

In this sense, financial markets function as the circulatory system of the economy, ensuring that money flows continuously from areas of surplus to areas where it can be used productively.

To understand this intuitively, imagine financial markets as a large organized marketplace for money and financial claims. Just as farmers bring their produce to a market and buyers purchase what they need, financial markets allow investors to buy financial assets and sellers to raise funds.

For example, when a company issues shares or bonds, it is essentially inviting the public to participate in its growth by investing money. Investors, in return, expect returns in the form of dividends, interest, or capital appreciation. Similarly, currency and commodity markets enable participants to trade currencies or raw materials, facilitating international trade and price discovery.

Thus, financial markets do not merely enable transactions; they perform a deeper economic function—they mobilize savings, allocate capital efficiently, and support economic growth, making them one of the most critical pillars of a modern financial system.

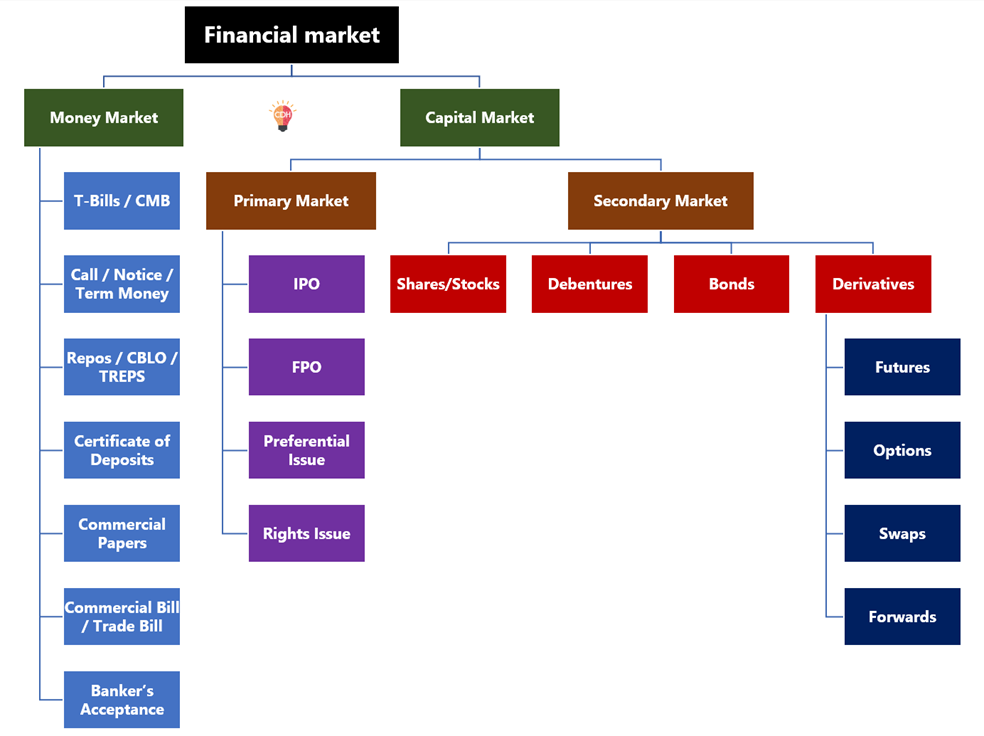

Structural Overview of the Financial Market

So, guys, Financial Market, is essentially the institutional mechanism through which funds move from savers (those with surplus money) to borrowers (those who need capital). Broadly, the financial market is divided into two segments based on the time horizon of funds: the Money Market and the Capital Market.

The Money Market deals with short-term funds, usually with maturity of less than one year, and its primary objective is liquidity management in the financial system. Instruments such as Treasury Bills (T-Bills) and Cash Management Bills (CMB) represent short-term borrowing by the government, while Call/Notice/Term Money reflects very short-term lending among banks to manage daily liquidity needs.

Similarly, instruments like Repos, CBLO, and TREPS are mechanisms through which institutions borrow funds against securities for a very short period. Other instruments such as Certificates of Deposit (CDs) and Commercial Papers (CPs) allow banks and corporations to raise short-term funds from investors. In essence, the money market acts like the circulatory system of the financial sector, ensuring that institutions facing temporary liquidity shortages can quickly obtain funds.

The Capital Market, on the other hand, deals with long-term financing, typically for periods greater than one year, and its purpose is capital formation for economic growth. It is divided into the Primary Market and the Secondary Market.

The Primary Market is where new securities are issued for the first time, meaning funds flow directly from investors to companies. For example, in an Initial Public Offering (IPO) a private company offers its shares to the public for the first time. An FPO (Follow-on Public Offer) allows a company already listed on the stock exchange to raise additional capital. Preferential issues allocate shares to selected investors such as institutional investors or promoters, while a Rights Issue allows existing shareholders to purchase additional shares before the public. Thus, the primary market is essentially the capital-raising mechanism of corporations and governments.

Once securities are issued in the primary market, they begin trading in the Secondary Market, which is where investors buy and sell already-issued financial instruments among themselves. Instruments like shares/stocks, debentures, and bonds are traded here, allowing investors to convert their investments into cash whenever needed, thereby providing liquidity to the capital market.

The secondary market also includes derivatives, which are financial contracts whose value is derived from underlying assets like stocks or bonds. These include futures, options, swaps, and forwards, which are used mainly for risk management (hedging), speculation, and price discovery. Therefore, while the money market ensures short-term liquidity, the capital market supports long-term investment and wealth creation, together forming the backbone of a modern financial system.

Key Differences Between Money Market and Capital Market

| Criteria | Money Market | Capital Market |

|---|---|---|

| Time Horizon | Short-term (less than 1 year) | Long-term (more than 1 year) |

| Purpose | Manage liquidity and working capital | Raise funds for long-term investments |

| Instruments | T-Bills, Commercial Paper, CDs, Repo, Call Money | Shares, Debentures, Bonds, Securities, Derivatives |

| Risk Level | Low | Higher |

| Returns | Lower | Potentially higher |

| Regulator | RBI | SEBI |

This article forms part of the broader Indian Economy syllabus for UPSC preparation.