Money Market instruments

In the financial system, the Money Market deals with short-term borrowing and lending of funds, generally for periods of less than one year. Governments, banks, and financial institutions frequently face temporary mismatches between their receipts and payments. To manage these short-term liquidity needs, they rely on instruments such as Treasury Bills (T-Bills), Cash Management Bills (CMBs), Call Money, Notice Money, and Term Money.

Treasury Bills (T-Bills)

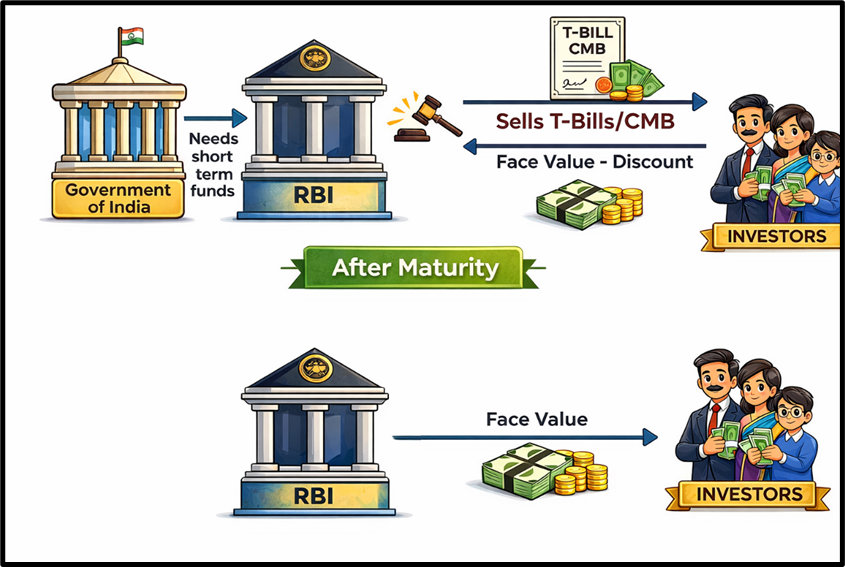

Treasury Bills, commonly known as T-Bills, are short-term debt instruments issued by the Reserve Bank of India (RBI) on behalf of the Government of India. Their primary purpose is to help the government meet short-term financial requirements, such as temporary budget gaps or immediate expenditure obligations.

T-Bills are issued for very short maturities. In India, they are commonly issued for → 14 days, 91 days, 182 days, 364 days

Since these instruments are backed by the sovereign guarantee of the Government of India, they are considered one of the safest financial investments in the market.

How T-Bills Work

A key feature of T-Bills is that they are issued at a discount to their face value, and investors earn profit from the difference between the purchase price and the maturity value.

Unlike many other securities, T-Bills do not pay periodic interest (coupon). Instead, the return is built into the discount mechanism.

Example

Suppose the government issues a 91-day T-Bill with a face value of ₹1,000.

During the auction, an investor purchases it for ₹990.

- Purchase price = ₹990

- Maturity value = ₹1,000

After 91 days, the investor receives ₹1,000, earning a profit of ₹10.

This profit represents the implicit interest earned on the investment.

Key Characteristics of T-Bills

- Issued by: RBI on behalf of Government of India

- Purpose: Financing government’s short-term needs

- Risk level: Extremely low (sovereign backing)

- Return structure: Discounted instrument

- Liquidity: Highly liquid and actively traded in the secondary market

For banks and financial institutions, T-Bills also serve as an important liquidity management tool.

Cash Management Bills (CMBs)

Cash Management Bills (CMBs) are also short-term debt instruments issued by the RBI on behalf of the Government of India. However, their purpose is slightly different from regular Treasury Bills.

While T-Bills are issued regularly according to a predetermined calendar, CMBs are issued on an ad-hoc basis to manage temporary cash flow mismatches of the government.

Their maturity period generally ranges from 14 days to 91 days

Thus, CMBs are essentially a flexible instrument used for urgent liquidity requirements of the government.

Working Mechanism

Similar to T-Bills:

- They are issued through an auction process.

- Investors purchase them at a discount to the face value.

- At maturity, the government pays the full face value.

Example

Suppose the government needs immediate funds and issues a 30-day Cash Management Bill with a face value of ₹10,000.

An investor buys the CMB for ₹9,950.

- Purchase price = ₹9,950

- Maturity value = ₹10,000

After 30 days, the investor receives ₹10,000, earning ₹50 as profit.

Key Characteristics of CMBs

- Purpose: Managing temporary cash mismatches of the government

- Tenure: Usually less than 91 days

- Issuance: Not regular, issued when required

- Return: Discount based

- Form: Issued in electronic form and traded in the secondary market

Thus, while T-Bills represent routine short-term borrowing, CMBs represent emergency liquidity management for the government.

Call Money

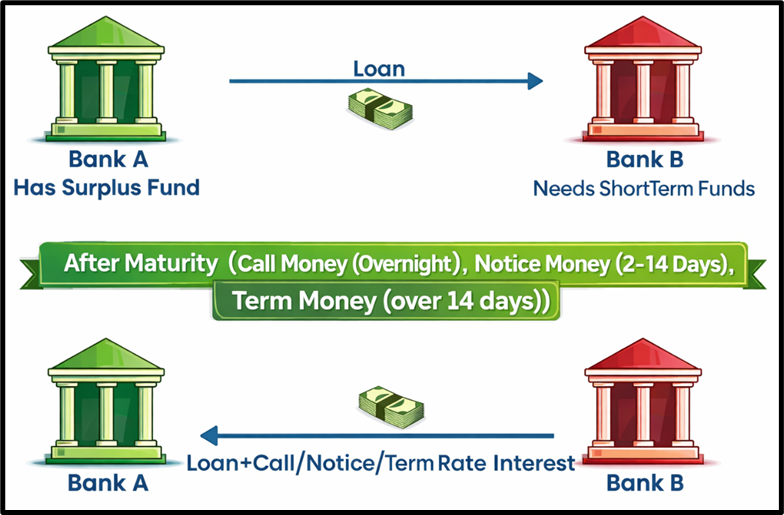

Call Money is a short-term money market instrument used by banks to borrow and lend funds in the inter-bank market.

The term “call” indicates that the lender can demand repayment at any time.

This instrument is primarily used for very short-term liquidity management, usually overnight.

Banks often experience daily fluctuations in liquidity due to → customer withdrawals, clearing of payments and settlement of transactions.

To manage such temporary shortages, banks rely on the call money market.

Example

Suppose:

- Bank A faces a temporary shortage of funds.

- Bank B has surplus liquidity.

Bank A borrows money from Bank B in the call money market at an agreed call rate (interest rate). Since the transaction is usually overnight, Bank A repays the amount the next day along with interest.

The call rate fluctuates daily depending on the demand and supply of funds in the banking system.

Key Characteristics

- Participants: Mainly banks and financial institutions

- Tenure: Usually overnight

- Flexibility: Lender can demand repayment anytime

- Purpose: Managing daily liquidity mismatches

Notice Money

Notice Money is similar to call money but involves a slightly longer borrowing period. It refers to inter-bank borrowing and lending for a period ranging from 2 days to 14 days.

The difference lies in the notice period.

Here, the lender provides advance notice specifying the date on which repayment is required.

Example

Suppose:

- Bank C requires funds for 7 days.

- Bank D has surplus liquidity.

Bank D lends money to Bank C in the notice money market for 7 days at an agreed interest rate. The notice ensures that Bank D knows in advance when the money will be returned, giving greater certainty compared to call money.

Key Characteristics

- Tenure: 2–14 days

- Participants: Mainly banks

- Certainty: Repayment date specified through notice

- Purpose: Short-term liquidity adjustment

Term Money

Term Money refers to inter-bank borrowing and lending for a period exceeding 14 days, typically up to one year.

Unlike call or notice money, term money transactions have a fixed maturity date decided at the beginning of the contract.

Neither the borrower nor the lender can demand repayment before maturity unless both parties agree.

Therefore, term money provides greater predictability for liquidity planning.

Example

Suppose:

- Bank E has surplus funds for 90 days.

- Bank F anticipates a 90-day funding gap.

Bank E lends funds to Bank F in the term money market for 90 days at a fixed interest rate.

Both banks clearly know:

- when repayment will occur

- what interest will be paid

This helps them manage cash flows more effectively.

Key Characteristics

- Tenure: More than 14 days up to 1 year

- Participants: Mainly banks and financial institutions

- Repayment: Fixed maturity date

- Purpose: Managing medium-term liquidity needs

Repurchase Agreements (Repos)

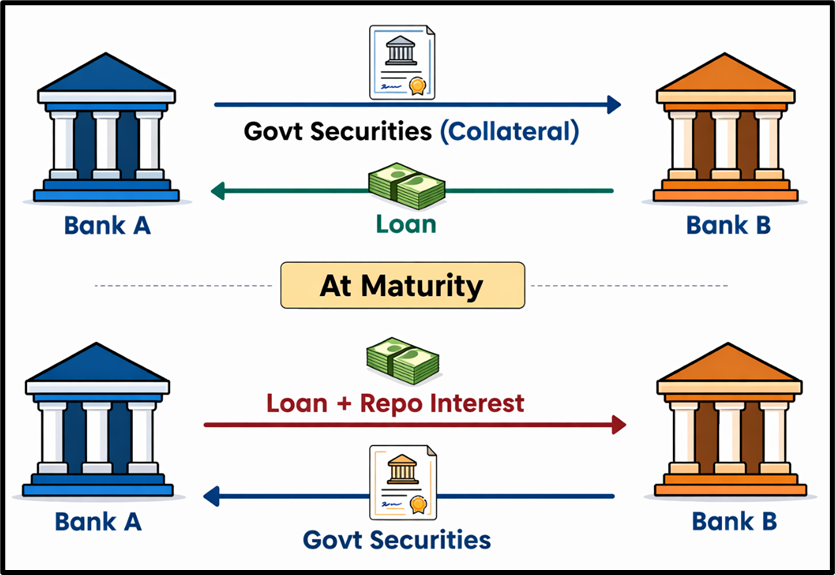

A Repurchase Agreement (Repo) is a short-term borrowing arrangement in the money market where one party sells securities with a promise to buy them back later at a predetermined price.

At first glance, it may appear like a simple sale and repurchase of securities, but economically it is actually a collateralised loan.

- The borrower receives funds immediately.

- The lender receives securities as collateral.

- Later, the borrower repurchases the securities, paying back the funds plus interest.

The interest component in this transaction is known as the Repo Rate.

In India, repos are commonly conducted using Government Securities (G-Secs) because they are safe and highly liquid.

How Repo Transactions Work

In a repo transaction, two key steps occur:

- Initial Sale

- The borrower sells securities to the lender.

- The borrower receives cash.

- Repurchase Agreement

- The borrower agrees to repurchase the same securities later.

- The repurchase price includes principal + interest (repo rate).

Thus, the difference between the sale price and repurchase price represents the interest on the short-term loan.

Example

Suppose Bank A needs funds for 3 days.

- Bank A sells Government Securities worth ₹100 crore to Bank B.

- The agreement states that Bank A will repurchase them after 3 days for ₹100.05 crore.

Here:

- Initial transaction: Bank A receives ₹100 crore

- Repurchase amount: ₹100.05 crore

The difference:

₹0.05 crore = interest earned by the lender

This interest reflects the repo rate applied for the duration of the transaction.

Why Repos are Important

Repos are widely used because they allow banks to:

- Raise short-term funds quickly

- Retain ownership of their securities

- Use securities as collateral to reduce risk

For the lender, repos are relatively safe because if the borrower fails to repay, the lender can keep the securities.

Reverse Repo

The same transaction looks different depending on the perspective.

- From the borrower’s perspective → it is a Repo.

- From the lender’s perspective → it is called a Reverse Repo.

In other words:

- Repo: Borrowing funds against securities

- Reverse Repo: Lending funds while holding securities as collateral

This mechanism is also widely used by the Reserve Bank of India in monetary policy operations to manage liquidity in the banking system.

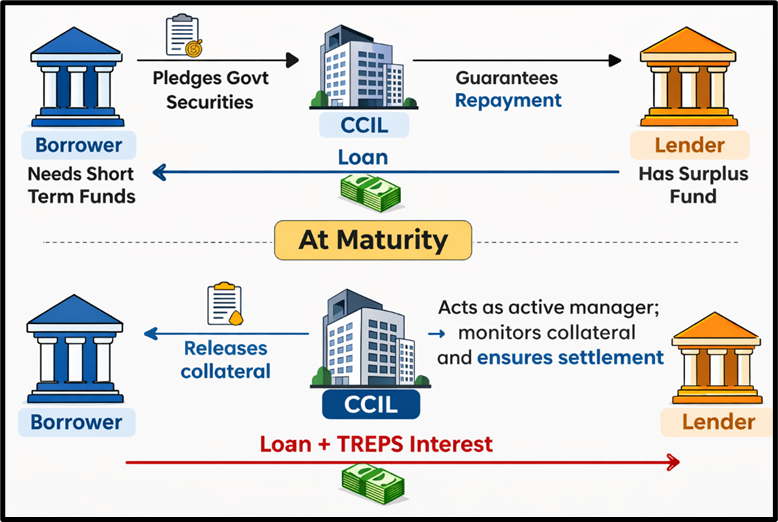

Collateralised Borrowing and Lending Obligation (CBLO)

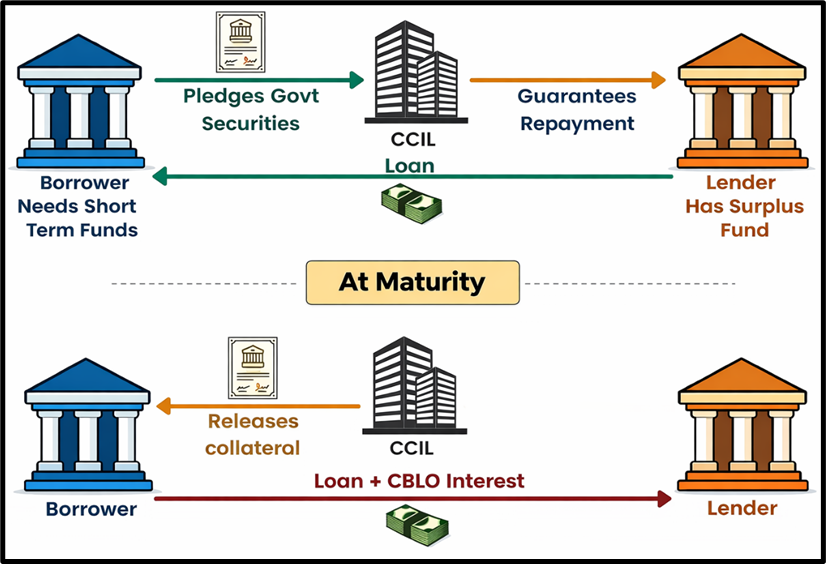

Collateralised Borrowing and Lending Obligation (CBLO) was a money market instrument introduced by the Clearing Corporation of India Ltd. (CCIL) to facilitate short-term borrowing and lending among market participants.

The key feature of CBLO was that all borrowing was backed by collateral, typically Government Securities.

The purpose of CBLO was to create a secure and efficient platform for short-term funds, especially for institutions that did not have direct access to the inter-bank call money market.

Role of CCIL

In CBLO transactions, the Clearing Corporation of India Ltd. (CCIL) acted as a central counterparty.

This means:

- CCIL guaranteed the settlement of transactions.

- Even if the borrower defaulted, the lender would still receive repayment.

This guarantee significantly reduced counterparty risk.

How CBLO Worked

- The borrower pledges Government Securities as collateral with CCIL.

- CCIL facilitates borrowing from lenders in the CBLO market.

- The lender provides funds to the borrower.

- At maturity, the borrower repays the principal plus interest.

- The pledged securities are released back to the borrower.

Example

Suppose Bank A needs funds for 5 days.

- Bank A pledges Government Securities with CCIL.

- CCIL allows Bank A to borrow funds from another participant in the CBLO market.

- At maturity, Bank A repays the loan with interest.

- CCIL then releases the pledged securities.

The lender feels secure because CCIL guarantees the repayment.

Important Development

CBLO played an important role in India’s money market for many years. However:

- CBLO was phased out in 2018

- It was replaced by a more advanced system called TREPS (Triparty Repo).

Triparty Repo (TREPS)

TREPS (Triparty Repo) is the modern money market instrument introduced to replace CBLO.

As the name suggests, a Triparty Repo involves three parties:

- Borrower

- Lender

- Triparty Agent (CCIL)

The third party—CCIL—manages the collateral, settlement, and risk management, ensuring the smooth functioning of the transaction.

Thus, TREPS combines the structure of repo transactions with the security of a central clearing mechanism.

How TREPS Works

The process follows these steps:

- The borrower sells Government Securities to the lender.

- CCIL acts as the triparty agent, managing the collateral.

- The borrower agrees to repurchase the securities later.

- The difference between the two prices represents the repo interest.

TREPS transactions can be conducted for:

- Overnight borrowing

- Short-term borrowing

Example

Suppose Bank A needs overnight funds.

- Bank A sells Government Securities to Bank B.

- CCIL manages the transaction as the triparty agent.

- The next day, Bank A repurchases the securities at a slightly higher price.

The difference between the two prices represents the interest paid on the short-term borrowing.

Why TREPS is Important

TREPS improves the money market in several ways:

- Reduces counterparty risk

- Ensures transparent settlement

- Provides better collateral management

- Enhances market efficiency

Because CCIL manages the entire process, participants can transact with greater confidence and lower risk.

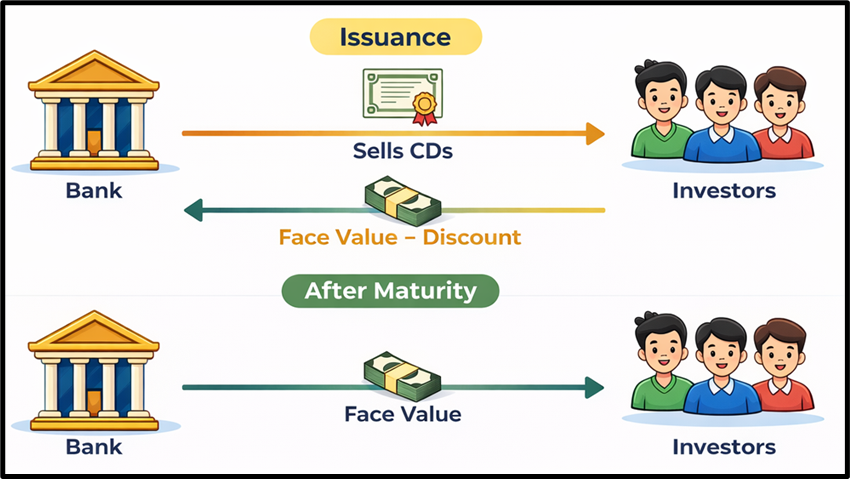

Certificate of Deposit (CD)

A Certificate of Deposit (CD) is a short-term negotiable promissory note issued by banks and financial institutions to raise funds from the market.

When a bank needs additional liquidity—for example, to support its lending activities—it can issue CDs to investors. By purchasing a CD, the investor is essentially lending money to the bank for a fixed short period.

The typical maturity period of CDs ranges from 7 days to 1 year

CDs are usually issued at a discount to their face value, meaning investors buy them at a lower price and receive the full-face value at maturity.

Because they are negotiable, CDs can also be traded in the secondary market, which improves their liquidity.

Example

Suppose a bank wants to raise funds and issues a 90-day Certificate of Deposit.

- Face value = ₹1,00,000

- Issue price = ₹98,000

An investor purchases the CD for ₹98,000. After 90 days, the bank pays ₹1,00,000 to the investor.

The investor earns ₹2,000 as profit, which represents the return on the investment.

Key Characteristics

- Issuer: Banks and financial institutions

- Tenure: 7 days to 1 year

- Nature: Negotiable promissory note

- Return: Discount-based

- Liquidity: Tradable in secondary market

Thus, CDs allow banks to mobilize short-term funds from investors efficiently.

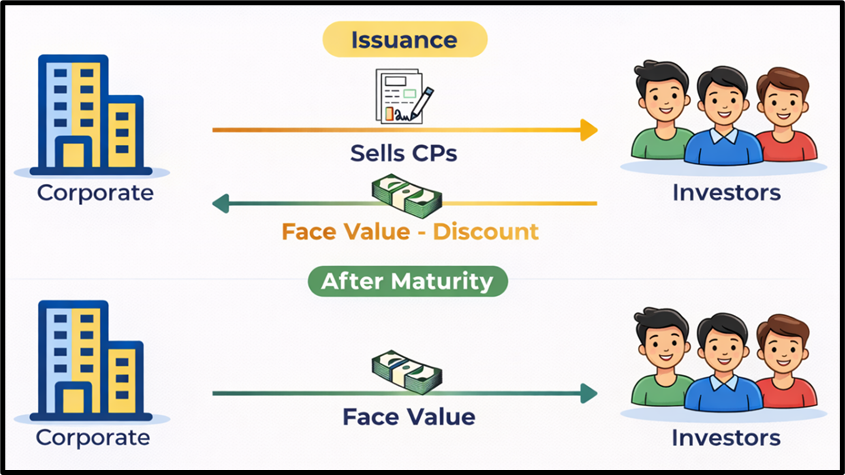

Commercial Papers (CP)

Commercial Papers (CPs) are short-term unsecured debt instruments issued by highly rated companies and financial institutions.

Unlike CDs, which are issued by banks, CPs are issued by corporations to meet working capital requirements, such as:

- purchasing raw materials

- paying salaries

- financing short-term operational expenses

Since CPs are unsecured instruments, meaning they are not backed by collateral, only financially strong companies with high credit ratings are allowed to issue them.

The maturity period generally ranges from 7 days to 1 year

Like many money market instruments, CPs are also issued at a discount to face value.

Example

Suppose a corporation requires funds for working capital and issues a 60-day Commercial Paper.

- Face value = ₹1,00,000

- Issue price = ₹98,500

An investor buys the CP for ₹98,500.

After 60 days, the company pays ₹1,00,000.

Profit earned by the investor → ₹1,500

This difference represents the interest earned on the investment.

Key Characteristics

- Issuer: Corporates and financial institutions

- Nature: Unsecured short-term debt

- Tenure: 7 days to 1 year

- Requirement: High credit rating

- Return: Discount-based

Thus, CPs allow companies to raise funds directly from the market instead of borrowing from banks, often at lower interest costs.

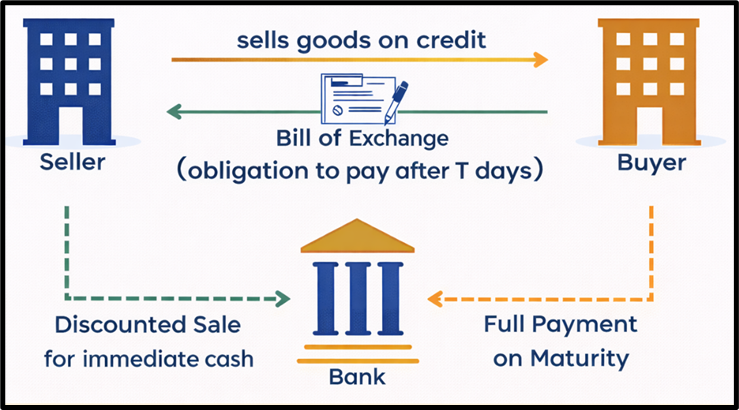

Commercial Bills (Trade Bills)

A Commercial Bill, also known as a Trade Bill, is a short-term negotiable instrument used to finance trade transactions.

These instruments arise from credit sales between businesses.

Consider a situation where a seller supplies goods but allows the buyer to pay later. In such cases, the seller draws a bill of exchange demanding payment at a future date.

The process involves three parties:

- Drawer → the seller who issues the bill

- Drawee → the buyer who must make payment

- Holder → the person who holds the bill (seller or bank)

Once the buyer accepts the bill, it becomes a legally binding promise to pay.

Discounting of Bills

Often, the seller may not want to wait until maturity to receive payment. In such cases, the seller can discount the bill with a bank.

The bank pays the seller immediate funds after deducting a discount, and later collects the full amount from the buyer at maturity.

This process is known as bill discounting.

Example

Suppose, Company A sells goods worth ₹50 lakh to Company B on 90-day credit.

Company A draws a bill of exchange for ₹50 lakh payable after 90 days, and Company B accepts it.

If Company A needs funds immediately, it may discount the bill with a bank.

The bank may pay ₹49.5 lakh immediately. After 90 days, the bank collects ₹50 lakh from Company B. The bank earns ₹0.5 lakh as interest (discount).

Importance

Commercial bills are important because they:

- Facilitate smooth trade transactions

- Improve business liquidity

- Provide short-term financing backed by actual trade activity

Because they arise from genuine trade backed by goods movement, they are generally considered relatively safe instruments.

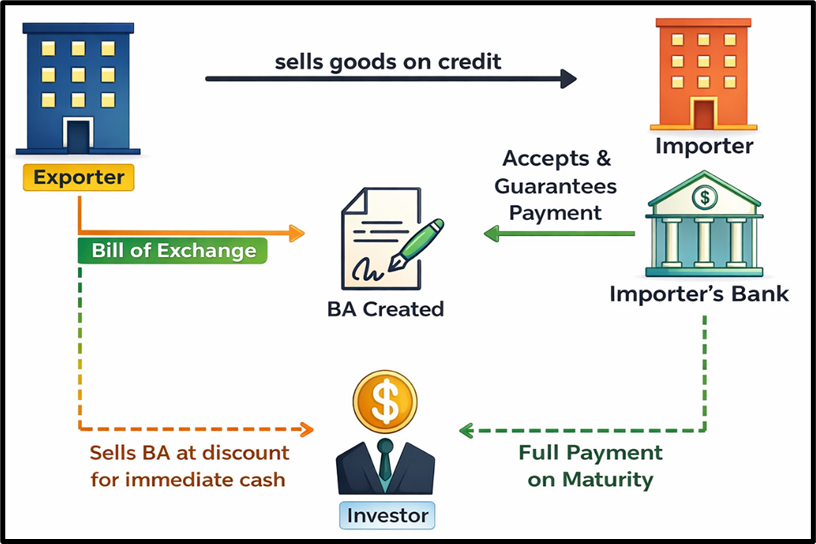

Banker’s Acceptance (BA)

A Banker’s Acceptance (BA) is a short-term negotiable instrument in which a bank guarantees payment of a bill of exchange at a future date.

When a bank accepts a bill, it essentially promises that it will make the payment on the maturity date, even if the original borrower fails to pay.

Because the payment is guaranteed by a reputable bank, the instrument becomes highly secure and easily tradable in financial markets.

Role in International Trade

Banker’s acceptances are particularly important in international trade, where exporters may be unsure about the reliability of foreign buyers.

By involving a bank as a guarantor, the exporter gains confidence that payment will be received.

Example

Suppose an Indian exporter sells machinery worth $1 million to a U.S. buyer, with payment due after 90 days.

The exporter draws a bill of exchange on the buyer’s bank. If the buyer’s bank accepts the bill, it becomes a Banker’s Acceptance.

This means the bank promises to pay $1 million after 90 days, even if the buyer defaults.

The exporter can:

- Hold the BA until maturity, or

- Sell it in the market at a discount to obtain immediate funds.

Key Characteristics

- Issuer/Guarantor: Bank

- Nature: Guaranteed payment instrument

- Usage: Widely used in international trade finance

- Liquidity: Tradable in secondary market

Thus, a Banker’s Acceptance combines trade finance with banking credibility, reducing risk for exporters.

Summary of Money Market Instruments (India)

| Instrument | Issuer / Participants | Typical Tenure | Secured / Unsecured | Purpose / Use |

| Treasury Bills (T-Bills) | Government of India (issued through RBI) | 14, 91, 182, 364 days | Secured (sovereign backed) | Raise short-term funds for government expenditure |

| Cash Management Bills (CMBs) | Government of India (via RBI) | 14–91 days | Secured | Manage temporary cash flow mismatches of the government |

| Call Money | Banks & financial institutions | Overnight | Unsecured | Manage immediate short-term liquidity in the inter-bank market |

| Notice Money | Banks & financial institutions | 2–14 days | Unsecured | Short-term inter-bank borrowing with prior notice |

| Term Money | Banks & financial institutions | More than 14 days up to 1 year | Unsecured | Manage predictable short-term liquidity requirements |

| Repo (Repurchase Agreement) | Banks, financial institutions, RBI | Overnight to short-term | Secured (collateral: government securities) | Borrow funds by selling securities with an agreement to repurchase |

| Reverse Repo | Banks lending to RBI or other banks | Overnight to short-term | Secured | Lending funds against securities |

| CBLO (Collateralised Borrowing and Lending Obligation) | Market participants via CCIL | Short-term | Secured (government securities) | Collateralised borrowing and lending platform (phased out in 2018) |

| TREPS (Triparty Repo) | Banks, financial institutions, mutual funds via CCIL | Overnight to short-term | Secured | Repo transactions with CCIL acting as triparty agent |

| Certificate of Deposit (CD) | Banks and financial institutions | 7 days – 1 year | Generally unsecured but backed by bank credibility | Raise short-term funds from investors |

| Commercial Paper (CP) | Highly rated corporates & financial institutions | 7 days – 1 year | Unsecured | Raise working capital funds directly from the market |

| Commercial Bills / Trade Bills | Businesses (seller draws bill on buyer) | Usually up to 90 days | Secured by underlying trade transaction | Finance domestic trade transactions |

| Banker’s Acceptance (BA) | Banks (guaranteeing payment) | Usually 30–180 days | Bank guaranteed | Facilitate and secure international trade payments |

Quick Classification for UPSC Revision

| Category | Instruments |

|---|---|

| Government Borrowing | Treasury Bills, Cash Management Bills |

| Interbank Liquidity | Call Money, Notice Money, Term Money |

| Collateralised Borrowings | Repo, Reverse Repo, TREPS (earlier CBLO) |

| Market Borrowing | Certificate of Deposit, Commercial Paper |

| Trade Financing | Commercial Bills, Banker’s Acceptance |

This article forms part of the broader Indian Economy syllabus for UPSC preparation.