Cooperative Banks

To begin with, we must understand the philosophy behind cooperative banking.

A Cooperative Bank is a financial institution that is owned, controlled, and operated by its members. These members usually belong to the same locality, profession, or community, and they come together voluntarily to pool their financial resources.

Instead of profit maximization like commercial banks, cooperative banks operate on the principle of mutual help and collective welfare.

The basic idea is simple:

People who face difficulty accessing formal banking services join together, create their own bank, and provide financial services to each other.

Thus, cooperative banks emerged as a grassroots financial system designed to improve financial inclusion, particularly for small traders, farmers, low-income households, Rural populations and small businesses

They provide normal banking services such as Savings accounts, Fixed deposits, Loans and credit facilities and Remittance services

However, their primary objective is not profit, but service to members.

Democratic Principle of Cooperative Banks

One of the most unique features of cooperative banks is democratic control.

Unlike commercial banks where power depends on shareholding, cooperative banks follow the rule:

“One member – One vote.”

This means:

→ A member with ₹1 share

→ A member with ₹10,000 shares

both have equal voting power.

This ensures that:

- Decision-making remains democratic

- Banks operate in the collective interest of members

- Control does not concentrate in the hands of wealthy individuals

Members vs Account Holders

It is important to distinguish between two groups:

Members

- Owners of the cooperative bank

- Must buy at least one share

- Have voting rights

Account Holders

- Only use banking services

- Do not necessarily own shares

- Have no voting rights

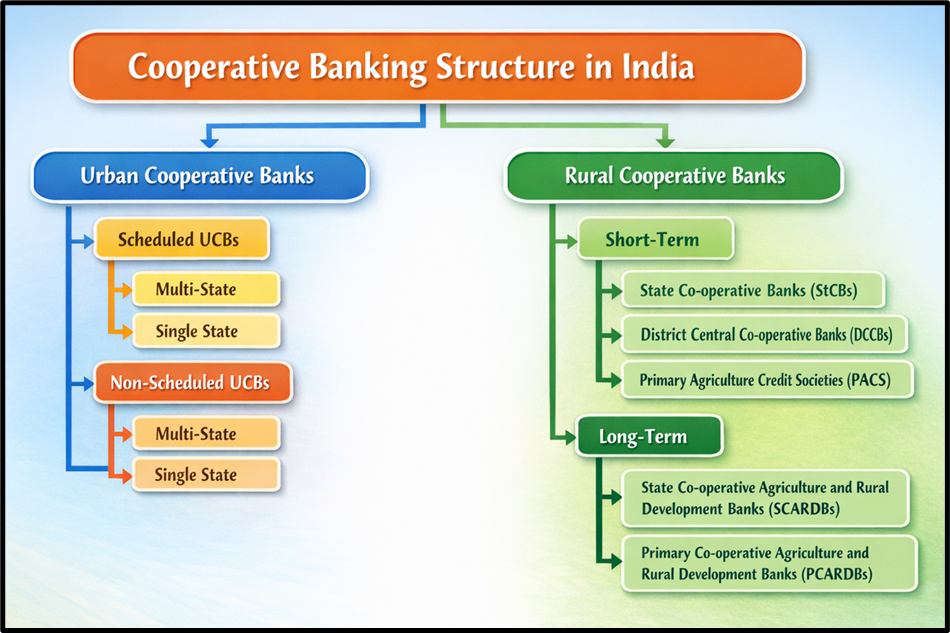

Types of Cooperative Banks

In India, cooperative banks are broadly classified into two categories based on their area of operation:

- Urban Cooperative Banks (UCBs)

- Rural Cooperative Banks (RCBs)

Let us understand each of them.

Urban Cooperative Banks (UCBs)

Urban Cooperative Banks mainly serve the urban and semi-urban population.

Their customers typically include → Small businesses, Traders, Self-employed professionals, Urban middle-class households, Small industries

These banks function much like commercial banks but operate under cooperative principles.

Classification Based on RBI Schedule

Urban Cooperative Banks are further classified depending on whether they are included in the Second Schedule of the RBI Act, 1934.

1. Scheduled Urban Cooperative Banks

These banks are included in the Second Schedule of the RBI Act, 1934.

Because of this status, they must:

- Maintain certain reserve requirements

- Meet RBI regulatory standards

Advantages of being a scheduled bank:

- Greater credibility

- Better regulatory supervision

- Access to RBI facilities

Examples include:

- Ahmedabad Mercantile Co-operative Bank Ltd.

- Bombay Mercantile Co-operative Bank Ltd.

2. Non-Scheduled Urban Cooperative Banks

These banks are not included in the Second Schedule of the RBI Act.

They still function under the regulatory framework but:

- Reserve requirements are generally lower

- Their operations are usually smaller in scale

Examples:

- Akhand Anand Co-operative Bank Ltd. (Surat)

- Sadhana Sahakari Bank Ltd. (Pune)

Classification Based on Area of Operation

Urban Cooperative Banks can also be classified based on their geographical jurisdiction.

1. Single-State Urban Cooperative Banks

These banks operate within one state only.

They are governed by the State Cooperative Societies Act.

This means:

- State government regulates their formation

- State authorities supervise their functioning

Under the Indian Constitution, cooperative societies are a State subject.

2. Multi-State Urban Cooperative Banks

These banks operate in more than one state.

They are governed by the Multi-State Co-operative Societies Act, 2002, which comes under the Central Government.

Example:

- Bombay Mercantile Co-operative Bank Ltd.

Rural Cooperative Banks (RCBs)

While Urban Cooperative Banks focus on urban areas, Rural Cooperative Banks focus on agricultural credit and rural development.

Their primary goal is to provide institutional credit to farmers and rural households.

Historically, farmers depended heavily on moneylenders, who charged extremely high interest rates. Cooperative banks were introduced to provide affordable agricultural credit.

Rural cooperative banks are divided based on loan duration:

- Short-Term Cooperative Credit Structure

- Long-Term Cooperative Credit Structure

Short-Term Rural Cooperative Structure (Three-Tier System)

Short-term agricultural credit in India operates through a three-tier institutional structure.

This system ensures that credit flows from the state level to the village level.

Structure

State Cooperative Banks (StCBs)

↓

District Central Cooperative Banks (DCCBs)

↓

Primary Agricultural Credit Societies (PACS)

1. State Cooperative Banks (StCBs)

These banks operate at the state level.

They act as the apex institutions in the short-term cooperative credit structure.

Their main roles include:

- Supervising cooperative credit institutions in the state

- Providing funds to District Central Cooperative Banks

- Acting as a link between RBI/NABARD and cooperative institutions

Examples:

- Andhra Pradesh State Co-operative Bank Ltd.

- Haryana State Co-operative Apex Bank Ltd.

2. District Central Cooperative Banks (DCCBs)

These banks operate at the district level.

They serve as intermediaries between the state-level banks and village-level societies.

Functions include:

- Providing loans to PACS

- Mobilizing deposits from rural areas

- Channelizing agricultural credit

Examples:

- Anantapur District Co-operative Bank Ltd.

- Chittoor District Co-operative Bank Ltd.

3. Primary Agricultural Credit Societies (PACS)

PACS operate at the village level, making them the grassroots institutions of cooperative credit.

They deal directly with → Farmers, Rural households and Agricultural workers

They provide credit for → Crop production, Fertilizers, Seeds and Agricultural equipment

Example:

- Sonamarg View Primary Agricultural Cooperative Credit Society Ltd.

PACS are extremely important for financial inclusion in rural India.

Long-Term Rural Cooperative Structure

Long-term agricultural investment requires larger loans with longer repayment periods.

To support this, India has a two-tier cooperative structure.

Structure

State Cooperative Agriculture and Rural Development Banks (SCARDBs)

↓

Primary Cooperative Agriculture and Rural Development Banks (PCARDBs)

1. SCARDBs

These operate at the state level and provide long-term agricultural finance.

Their loans support → Irrigation projects, Farm mechanization, Land development, Rural infrastructure

Example:

- Tripura Cooperative Agriculture & Rural Development Bank Ltd.

2. PCARDBs

These banks operate at the local level and directly provide long-term credit to Farmers and Rural entrepreneurs

Example:

- Puttukottai PCARD Bank

Duality of Control in Cooperative Banks

One of the most distinctive issues in cooperative banking is the Dual Control System.

This arises because:

- Banking is a Central subject

- Cooperative societies are a State subject

Therefore, cooperative banks fall under two authorities simultaneously.

RBI Controls

RBI regulates banking functions, such as → Interest rates, Loan policies, Banking licenses, Financial supervision and audits

Registrar of Cooperative Societies (State Government)

State authorities regulate cooperative aspects, including:

- Registration of cooperative societies

- Elections to managing committees

- Protection of members’ rights

This dual regulation often leads to administrative complexity.

Challenges Faced by Cooperative Banks

Despite their importance, cooperative banks face several structural challenges.

1. Regulatory Complexity

Dual control between RBI and State authorities sometimes creates regulatory confusion.

2. Governance Issues

Many cooperative banks suffer from → Political interference, Weak management structures, Lack of professional expertise

3. Capital Adequacy Problems

Cooperative banks often struggle to maintain adequate capital buffers, which → Limits lending capacity and weakens financial stability

4. Technological Backwardness

Compared to commercial banks, many cooperative banks lag in → Digital banking, Core banking systems and Online financial services

5. Poor Asset Quality

Many cooperative banks face high Non-Performing Assets (NPAs) due to → weak credit appraisal, local economic stress and lenient lending practices

Government Steps to Strengthen Cooperative Banks

Recognizing these issues, the government has taken several reform measures.

1. Amendment to the Banking Regulation Act (2020)

A major reform occurred in 2020, when the Banking Regulation Act was amended.

This amendment brought cooperative banks under stronger RBI supervision, similar to commercial banks.

The aim was to improve transparency, accountability and financial stability

2. Capital Infusion

The government has provided financial assistance to weak cooperative banks to improve their capital base.

3. Training and Capacity Building

Programs have been launched to improve skills in areas such as governance, risk management and regulatory compliance

4. Consolidation and Mergers

The government encourages mergers of small cooperative banks to create larger, stronger and more stable institutions

5. Enhanced Monitoring by RBI

The RBI now conducts stronger surveillance and supervision to detect early signs of financial stress. This helps prevent bank failures and depositors’ losses.