India’s securities market infrastructure

Imagine the securities market as a large, organized ecosystem where companies raise money and investors invest their savings. For such a system to function smoothly, it needs institutions, platforms, and mechanisms that regulate, facilitate, and settle transactions.

India has built a well-structured financial market infrastructure, consisting of regulatory bodies, trading platforms, custodial institutions, and settlement systems. Let us understand each component.

Securities and Exchange Board of India (SEBI)

At the top of the securities market structure stands the Securities and Exchange Board of India (SEBI).

Role of SEBI

SEBI acts as the primary regulator of India’s securities market. Its fundamental responsibility is to ensure that the market functions in a fair, transparent, and efficient manner.

Why SEBI is Necessary

Financial markets involve large flows of money. Without regulation, problems like insider trading, market manipulation, fraud and investor exploitation could easily occur.

Therefore, SEBI performs three core functions:

1️⃣ Regulation

SEBI formulates rules, guidelines, and regulations for stock exchanges, listed companies, brokers, mutual funds and investment advisors

2️⃣ Investor Protection

SEBI ensures that investors receive:

- proper disclosure of company information

- fair treatment in the market

- protection against fraudulent practices

3️⃣ Market Development

SEBI continuously works to modernize the market, introducing reforms such as electronic trading, dematerialisation of shares and improved settlement systems

In short, SEBI is the guardian of India’s capital market.

Stock Exchanges

The next important component is the stock exchange, which acts as a marketplace for trading securities.

A stock exchange is a platform where companies list their securities and the investors buy and sell those securities

In India, the two most important stock exchanges are:

- National Stock Exchange of India (NSE)

- Bombay Stock Exchange (BSE)

These exchanges allow trading in → equities (shares), derivatives, debt securities and exchange traded funds (ETFs)

Essentially, they connect buyers and sellers of financial assets.

Now let us briefly compare BSE and NSE, the two pillars of India’s equity market.

| Basis | BSE | NSE |

|---|---|---|

| Brief Introduction | Oldest stock exchange in Asia | Largest stock exchange in India |

| Founded | 1875 | 1992 |

| Benchmark Index | Sensex (30 companies) | Nifty 50 (50 companies) |

| Listed Companies | Around 7400 | Around 1790 |

| Market Capitalisation | ~ ₹266 trillion | ~ ₹199 trillion |

| Trading Mechanism | Combination of traditional and electronic | Fully electronic |

| Liquidity | Lower | Higher (clear leader) |

Key Insight

Although BSE has more listed companies, NSE dominates trading volume and liquidity.

Higher liquidity means:

- easier buying and selling

- tighter bid-ask spreads

- better price discovery

That is why most derivatives trading in India occurs on the NSE.

Depositories

Earlier, shares existed in physical paper certificates. This system created several problems → risk of loss or theft, delays in transfer, forgery and duplication and cumbersome paperwork

To solve this, India introduced dematerialisation (Demat).

Depositories act as electronic vaults where securities are stored digitally.

India has two depositories:

- National Securities Depository Limited (NSDL)

- Central Depository Services Limited (CDSL)

How It Works

Investors open a Demat Account with a Depository Participant (DP) such as a bank or brokerage firm.

Then:

- shares are stored electronically

- transfer of ownership happens instantly

- settlement becomes faster and safer

Thus, depositories eliminate the need for physical share certificates.

Clearing Corporations

Once a trade happens on a stock exchange, the transaction must be settled.

This means:

- the buyer must receive securities

- the seller must receive money

This process is handled by clearing corporations.

The major clearing corporations in India are:

- National Securities Clearing Corporation Limited (NSCCL) — for NSE

- Indian Clearing Corporation Limited (ICCL) — for BSE

Key Function

Clearing corporations act as a central counterparty (CCP) between buyers and sellers.

This means:

- they guarantee the settlement of trades

- even if one party defaults, the transaction still completes.

Thus, they reduce counterparty risk and maintain confidence in the market.

Electronic Trading Platforms

In earlier times, stock trading occurred through open outcry systems on trading floors. However, modern markets operate through electronic trading platforms.

Both NSE and BSE now provide fully automated order matching systems.

How Electronic Trading Works

- Investors place orders through brokerage platforms such as → Zerodha, Groww etc.

- Orders are transmitted electronically to the exchange.

- The system automatically matches buy and sell orders.

- Trades are executed in milliseconds.

Advantages

Electronic trading provides faster execution, higher transparency, reduced human errors and better market access for retail investors

This modernization is one of the major reasons why India’s securities market is among the most technologically advanced in the world.

Payment and Settlement Systems

After the trade is executed and cleared, the final step is settlement of funds.

In India, banking payment systems facilitate this transfer of money.

The major systems used are:

- Real Time Gross Settlement (RTGS)

- National Electronic Funds Transfer (NEFT)

These systems ensure that → funds move securely, transactions are recorded, payments are completed efficiently

In the securities market, settlement cycles have improved dramatically and now operate on T+1 settlement, meaning the transaction is settled one working day after the trade.

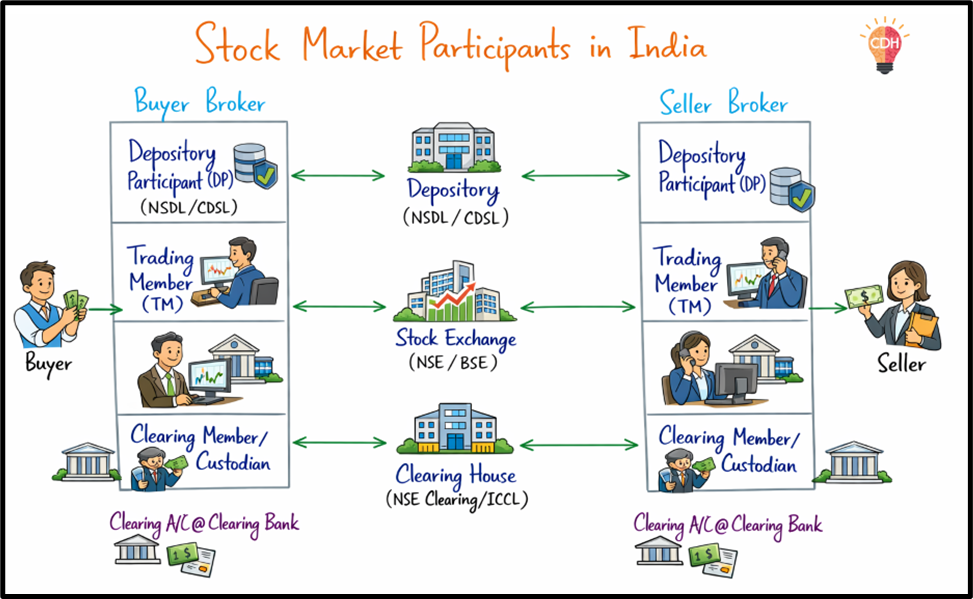

Life Cycle of a Stock Market Trade in India

The functioning of India’s securities market can be best understood by looking at how a typical stock market transaction takes place.

When an investor decides to buy shares, the order is placed through an online brokerage platform such as Zerodha or Groww using a trading account linked to a Demat account. This order is then transmitted to a stock exchange such as the National Stock Exchange of India or the Bombay Stock Exchange, where an automated electronic trading system matches the buyer’s order with a corresponding seller’s order. Once the prices match, the trade is executed within milliseconds, ensuring efficiency, transparency, and accurate price discovery in the market.

After the trade is executed, the responsibility shifts to clearing corporations such as National Securities Clearing Corporation Limited or Indian Clearing Corporation Limited. These institutions act as central counterparties that guarantee the completion of transactions between buyers and sellers, thereby reducing the risk of default.

At the same time, the transfer of securities takes place through depositories like National Securities Depository Limited and Central Depository Services Limited, where shares are held in electronic (dematerialized) form. The shares move from the seller’s Demat account to the buyer’s Demat account without any physical certificates, making the process faster and more secure.

Finally, the payment for the securities is settled through banking systems such as Real Time Gross Settlement and National Electronic Funds Transfer, ensuring the transfer of funds from the buyer to the seller. India currently follows a T+1 settlement cycle, meaning that the final settlement of funds and securities takes place one working day after the trade.

This integrated system of brokers, stock exchanges, clearing corporations, depositories, and payment systems—under the regulatory oversight of Securities and Exchange Board of India—ensures that India’s securities market operates in a transparent, efficient, and secure manner.