Market Based Monetary Instruments

Bank Rate

The Bank Rate is the rate at which the RBI → Lends money to commercial banks → Without collateral

It is also called the discount rate.

Historical Role of Bank Rate

Earlier:

- Bank Rate was the primary policy rate

- Changes in Bank Rate influenced → Lending rates, Deposit rates, Overall credit conditions

However, with the introduction of → LAF, Repo rate, MSF → The Bank Rate lost its day-to-day operational role.

Current Role of Bank Rate

Today, the Bank Rate functions mainly as a → Penalty and Signalling Rate

It is used to calculate penal interest when banks fail to maintain → CRR/ SLR

Penal Structure

Penalties are imposed as → Bank Rate + 3%, or Bank Rate + 5%

Example

- Bank Rate = 4%

- Penalty = Bank Rate + 3%

- Penal interest = 7%

If a bank falls short of SLR:

- It must pay 7% interest on the shortfall

- This enforces regulatory discipline

Alignment with MSF

- The Bank Rate is aligned with the MSF rate

- Therefore → Whenever MSF changes, Bank Rate changes automatically

📌 UPSC Insight:

Bank Rate is now a reference rate, not a liquidity management tool.

One-Glance Comparison of Policy Rates

| Feature | Repo Rate | Reverse Repo | MSF Rate | SDF Rate | Bank Rate |

|---|---|---|---|---|---|

| Basic Function | RBI lends to banks | RBI borrows from banks | Emergency lending | Absorbs excess funds | Penal/reference rate |

| Collateral | Yes | Yes | Yes (SLR allowed) | No | No |

| Role in LAF | Centre | Discretionary | Ceiling | Floor | Outside LAF |

| Relation to Repo | Base rate | Below repo | Repo + 25 bps | Repo − 25 bps | = MSF |

| Main Use Today | Core policy signal | Secondary | Safety valve | Liquidity floor | Penalty computation |

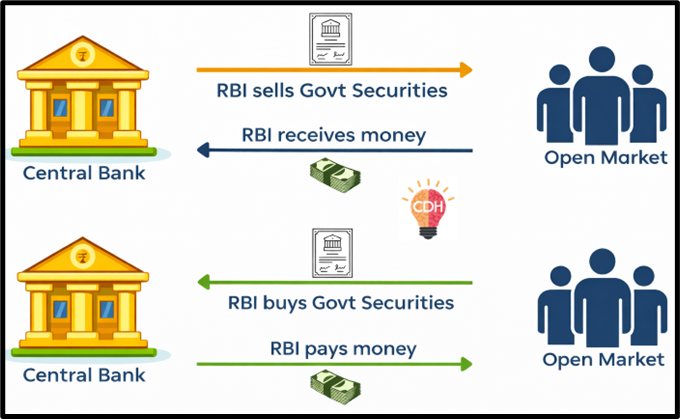

Open Market Operations

Open Market Operations (OMOs) refer to the buying and selling of government securities by RBI in the open market to regulate liquidity.

Unlike LAF:

- OMOs are outright transactions

- They have a longer-lasting impact on liquidity

OMO for Liquidity Injection

When RBI wants to increase money supply:

- It buys government securities from banks and PDs (Primary Dealers)

- Pays by crediting banks’ accounts

- Bank reserves increase

- Lending capacity expands

📌 Impact

More credit → higher investment & consumption → economic growth

OMO for Liquidity Absorption

When RBI wants to control inflation:

- It sells government securities

- Money flows from banks to RBI

- Bank reserves fall

- Lending capacity reduces

📌 Impact

Lower borrowing & spending → inflation cools down

OMOs vs LAF (Conceptual Distinction)

- LAF → Short-term, reversible liquidity management

- OMOs → Longer-term, durable liquidity impact

👉 UPSC often tests this difference.

Forex Swaps (Foreign Exchange Swaps)

What is a Forex Swap?

A forex swap is a two-leg transaction:

- One transaction happens today

- The reverse transaction happens on a pre-decided future date

- Exchange rate for both legs is pre-agreed

Forex swaps are conducted through RBI-announced auctions, in which commercial banks participate.

👉 Key idea: Temporary exchange of currencies to manage liquidity without permanently changing forex reserves.

Types of Forex Swaps

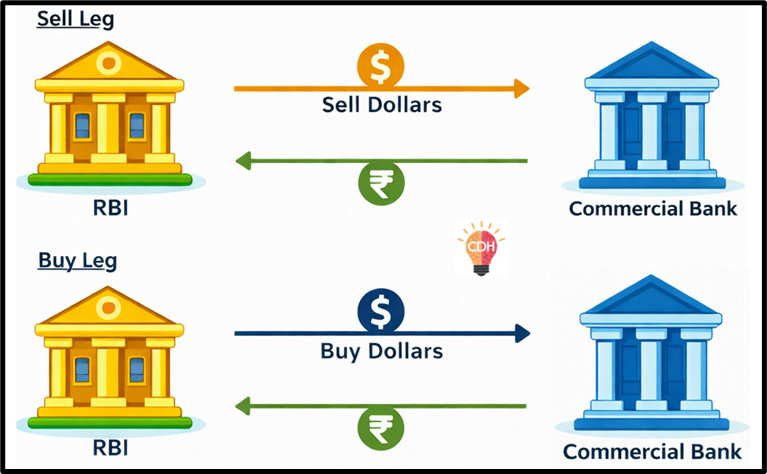

1. Sell/Buy Forex Swap

(Liquidity Absorption Tool)

Structure

- Sell leg (now): RBI sells foreign currency (e.g., USD) to banks

- Buy leg (future): RBI agrees to buy back the same foreign currency later

Purpose

- Absorb rupee liquidity

- Prevent rupee depreciation

- Manage inflationary pressure caused by excess liquidity

Example

- RBI sells USD 100 million at ₹80/USD

- Absorbs ₹8 billion from the banking system

- After one year, RBI buys back USD at ₹81/USD

- Re-injects ₹8.1 billion

📌 Insight: Liquidity absorption is temporary, unlike permanent sterilization.

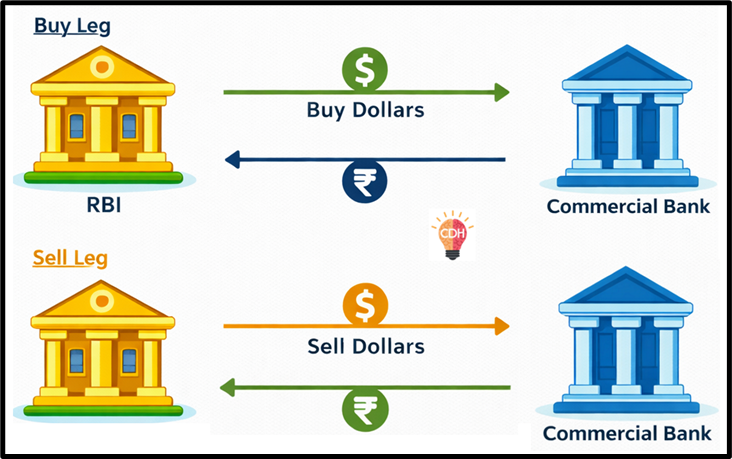

2. Buy/Sell Forex Swap

(Liquidity Injection Tool)

Structure

- Buy leg (now): RBI buys foreign currency from banks

- Sell leg (future): RBI sells the same amount back later

Purpose

- Inject rupee liquidity

- Tackle liquidity crunch

- Smooth volatility in forex markets

Example

- RBI anticipates liquidity stress due to tax outflows

- Buys USD 100 million at ₹80/USD

- Injects ₹8 billion into the system

- After one year, RBI sells back USD at ₹79/USD

- Absorbs ₹7.9 billion

Why Forex Swaps Are Powerful

- Liquidity impact is time-bound

- Do not permanently alter RBI’s forex reserves

- Useful during:

- Capital flow volatility

- External shocks

- Global monetary tightening/loosening cycles

📌 Note:

Forex swaps allow RBI to manage liquidity and exchange rate simultaneously without changing the policy rate.

Market Stabilization Scheme (MSS)

What is MSS?

The Market Stabilization Scheme (MSS) is a liquidity absorption tool used by RBI to sterilize excess liquidity, especially arising from large foreign exchange inflows.

- Introduced in 2004

- Used when forex inflows create → Excess rupee liquidity, Inflationary pressure, Undue appreciation of the rupee

Why MSS Was Needed

When RBI buys foreign currency to prevent rupee appreciation → It injects rupees into the banking system → This can fuel inflation

👉 MSS was designed to neutralize (sterilize) this excess liquidity.

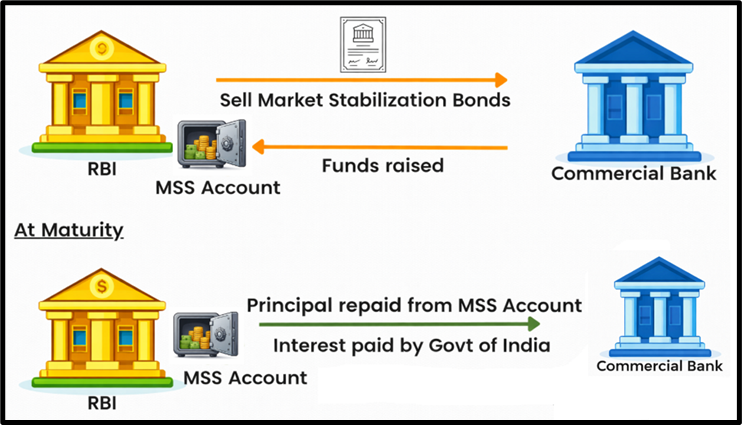

How MSS Works

- RBI issues Market Stabilization Bonds (MSBs)

- These are government-backed securities

- Sold via auction to banks and financial institutions

- Money raised:

- Not used for government spending

- Parked in a separate MSS account

Important Features

- Interest cost borne by Government of India

- Principal repaid from the MSS account

- Usually short-term securities

- Purely a liquidity management tool

Indian Context Examples

Early 2000s

- Large capital inflows → Rupee appreciation pressure → MSS used extensively to absorb liquidity

Demonetisation (2016)

- Sudden surge in bank deposits → Massive excess liquidity → MSS deployed to mop up surplus funds

📌 UPSC Value Addition:

MSS is an exceptional tool, activated only during extraordinary liquidity situations.

MSS vs Open Market Operations (OMOs)

| Aspect | OMOs | MSS |

|---|---|---|

| Nature | Buying/selling G-secs | Issuance of special bonds |

| Usage | Regular monetary tool | Exceptional, situation-specific |

| Liquidity Impact | Injection or absorption | Mainly absorption |

| Securities | Normal G-Secs, T-Bills | Market Stabilization Bonds |

| Fiscal Impact | Normal budget process | Interest borne by government, funds parked |