Reserve Ratios

Cash Reserve Ratio (CRR)

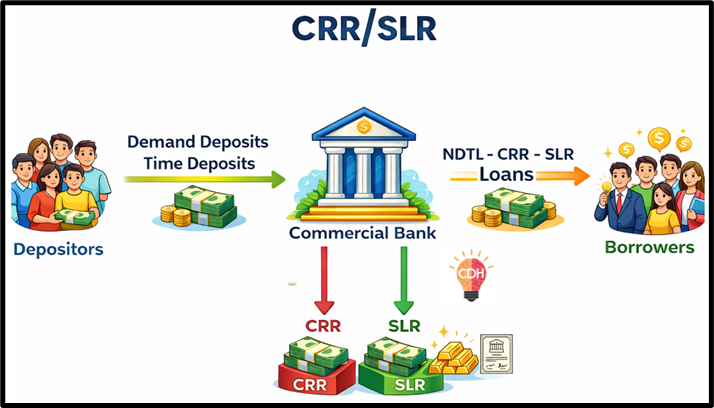

The Cash Reserve Ratio (CRR) is the percentage of a bank’s total deposits that must be kept → As cash in its vaults, or With the RBI

Banks cannot use this portion for lending or investment.

Example

Suppose → Total bank deposits = ₹1,000 crore; CRR = 4%

Then → ₹40 crore must be kept as CRR. Only the remaining amount can be used for lending

Purpose of CRR

CRR serves two critical functions:

- Ensures bank solvency and depositor safety

→ Banks can meet withdrawal demands and prevent bank runs. - Controls money supply in the economy

CRR as a Policy Tool

- CRR ↓ (Reduced) → Banks can lend more → Money supply ↑ → Growth stimulus

- CRR ↑ (Increased) → Lending capacity reduces → Money supply ↓ → Inflation control

📌 UPSC Insight:

CRR is a powerful but blunt tool, as it directly locks funds without earning any return for banks.

Statutory Liquidity Ratio (SLR)

The Statutory Liquidity Ratio (SLR) is the percentage of deposits that banks must maintain in → Cash, Gold, Government securities

Unlike CRR, SLR assets are held by banks themselves, not with the RBI.

Example (CRR + SLR Together)

Assume → Total deposits = ₹1,000 crore, CRR = 4%, SLR = 18%

Then → CRR = ₹40 crore, SLR = ₹180 crore, Total locked = ₹220 crore

👉 Funds available for lending = ₹780 crore

(Note: SLR assets can earn returns, especially government securities.)

Purpose of SLR

- Ensures liquidity and financial discipline

- Promotes investment in government securities

- Strengthens confidence in the banking system

SLR as a Policy Tool

- SLR ↑ → Lending capacity ↓ → Liquidity tightens

- SLR ↓ → Lending capacity ↑ → Credit expansion → Growth support

Impact of CRR and SLR on Banking Liquidity

Both CRR and SLR:

- Reduce lendable resources

- Help RBI manage excess liquidity or inflation

- Act as safeguards against financial instability

However, they operate in different ways, which is crucial for exam answers.

CRR vs SLR: Key Differences

| Basis | CRR | SLR |

|---|---|---|

| Meaning | % of deposits kept as cash reserve | % of deposits kept in liquid assets |

| Maintained with | RBI or bank vaults | Bank itself |

| Form | Only cash | Cash, gold, government securities |

| Return earned | No interest | Interest/returns earned |

| Purpose | Liquidity control + safety | Liquidity + financial discipline |

| Impact on lending | Directly reduces lendable funds | Reduces lendable funds but earns returns |