Transmission of Monetary Policy

Introduction

Understanding monetary policy transmission is crucial because policy changes matter only if they reach the real economy.

What Is Monetary Policy Transmission?

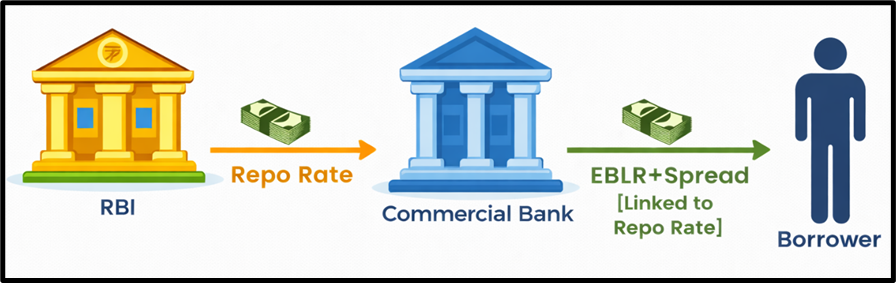

Monetary policy transmission refers to the process through which RBI’s policy actions (like repo rate changes) → affect bank lending rates → Which then influence consumption, investment, and growth

In simple terms:

Policy rate → Bank lending rate → Borrowing & spending decisions

Ideal Transmission Mechanism

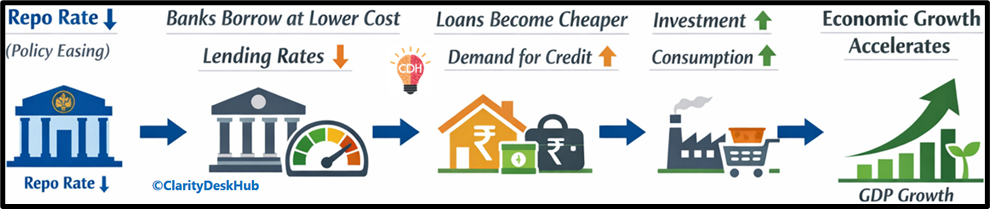

When RBI reduces the repo rate → Banks borrow at a lower cost → Banks reduce lending rates → Loans become cheaper → Demand for credit rises → Investment and consumption increase → Economic growth accelerates

Why Transmission Often Falls Short in India

In reality, banks may → Delay rate cuts or, Pass on only partial reductions

Key Reasons

- High Non-Performing Assets (NPAs)

→ Banks remain cautious about lending - Liquidity constraints

- Risk aversion during downturns

- Legacy loan portfolios at higher interest rates

📌 Result: Weak or incomplete transmission.

RBI Reforms to Ensure Better Monetary Policy Transmission

Over time, the Reserve Bank of India has reformed the way banks set lending rates, so that changes in the policy repo rate are passed on faster, more transparently, and more fairly to borrowers.

How Do Banks Decide Interest Rates?

Banks do not lend at the repo rate directly. Instead, they follow an RBI-prescribed benchmark system, to which they add a spread.

Over the years, India has moved through four major systems, each aimed at improving transmission.

Evolution of Lending Rate Systems in India

1. Prime Lending Rate (PLR) – Before 2010

- What it was: A benchmark rate for the best customers

- Problem:

- Banks had excessive discretion

- Same loan, different rates for different borrowers

- Outcome: Poor transparency, weak transmission

📌 Status: Discontinued in 2010

2. Base Rate System – 2010 to 2016

- What changed:

Banks could not lend below a minimum Base Rate - Objective: Bring fairness and a floor to lending rates

- Problem:

- RBI cut repo rates, but banks delayed passing benefits

- Transmission remained slow

📌 Status: Replaced by MCLR in 2016

3. MCLR (Marginal Cost of Funds Based Lending Rate) – 2016 onwards

How MCLR Works

- Lending rates linked to:

- Cost of deposits

- Cost of market borrowings

- Marginal cost of funds

- If RBI cuts repo rate → banks should lower MCLR

Why MCLR Fell Short

- Banks adjusted MCLR slowly

- Different banks had different MCLR structures

- Reset periods diluted immediate transmission

📌 Current Status:

- Still applies to legacy loans

- If you took a loan between 2016–2019, it is likely MCLR-linked

4. External Benchmark-Based Lending Rate (EBLR) – 2019 to Present

This is the most important reform from a UPSC and real-world perspective.

How EBLR Works

Instead of internal benchmarks, banks now link lending rates to external benchmarks, such as:

- RBI Repo Rate

- Treasury Bill yields

- Other market-based rates

👉 If RBI cuts the repo rate, banks must pass on the benefit almost immediately.

Analysis of EBLR

Why EBLR Is Superior

- ✅ High transparency – Same benchmark for all banks

- ✅ Faster transmission – No internal delays

- ✅ Reduced discretion – RBI policy reaches borrowers directly

📌 Status (Very Important):

- Implemented from October 2019

- All new floating-rate retail loans (home, auto, personal) must be linked to EBLR

Which System Applies to Your Loan?

| Loan Taken In | Applicable System |

| Before 2010 | PLR |

| 2010 – 2016 | Base Rate |

| 2016 – 2019 | MCLR |

| After Oct 2019 | EBLR |

Key Points:

- Old loans may still be under MCLR/Base Rate

- Borrowers can switch from MCLR to EBLR (fees may apply)

- Fixed-rate loans do not respond to RBI rate changes

MCLR vs EBLR (Prelims Favourite)

| Feature | MCLR | EBLR |

|---|---|---|

| Linked to | Internal cost of funds | External benchmark |

| RBI Rate Pass-Through | Slow | Immediate |

| Transparency | Lower | High |

| Bank Discretion | High | Limited |

How Final Loan Interest Rate Is Determined

Even under EBLR, the repo rate is not your final loan rate.

Formula

Loan Interest Rate = Benchmark Rate (EBLR) + Spread

What Is the Spread?

The spread is the bank’s markup over the benchmark. It varies by borrower and loan type.

Factors Determining the Spread

- Credit Risk of Borrower

- Higher risk → higher spread

- Lower risk → lower spread

- Operational Costs

- Staff, branches, technology, administration

- Profit Margin

- Bank’s business strategy and competition

- Loan Type & Tenure

- Personal loans > Home loans (higher risk)

- Longer tenure → higher uncertainty

- Liquidity & Capital Adequacy

- Banks under stress charge higher spreads

Simple Illustration

- EBLR (linked to repo rate) = 6%

- Bank’s spread = 3%

👉 Final loan rate = 9%

The spread compensates the bank for risk, costs, and profit, while EBLR ensures policy rate changes are transmitted cleanly.

To explore all Indian Economy topics in a structured manner, visit the complete Indian Economy UPSC Notes page.